Source: Prudential Douglas Elliman

The East End residential real estate market completely collapsed in the first

quarter of 2011, according to a Prudential Douglas Elliman market report released

today, but the report’s preparer said the numbers were an anomaly created by

fear surrounding the possible expiration of the so-called “Bush tax cuts” this past

December. (President Barack Obama eventually extended the cuts for two years in late December.)

Jonathan Miller, president and CEO of Miller Samuel and the compiler of the report,

said that buyers who feared Bush tax cuts would expire in 2010

moved early on their East End purchases, thereby inflating last quarter’s sales

numbers and depressing statistics for the first three months of this year.

The combination set the first-quarter report up for drastic declines.

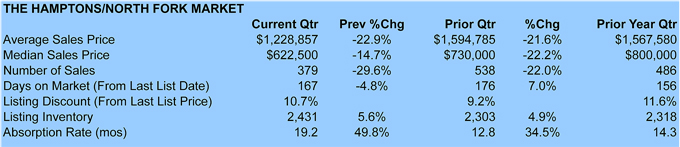

In the first three months of 2011, the number of sales in the Hamptons and North Fork plummeted to 379, down 22 percent from the same period a year ago and 29.6 percent compared with fourth-quarter 2010. The

median sales price declined to $622,500, down 22.2 percent from the first quarter

of last year and 14.7 percent from last quarter.

“On the surface it looked like the market collapsed,” Miller said, “but concern over

the tax cuts expiring pushed people to close by Dec. 31 — especially on the high-

end.” He noted that home sales greater than $1 million, which typically comprise

one-quarter to one-third of the East End market, were at 36.1 percent of the total number of sales in the last three months of 2010, but just 19.8 percent

this quarter. That’s the lowest figure since the fourth quarter of 2008 when Lehman

Brothers declared bankruptcy.

More proof of the abnormal

market circumstances comes from the fact that despite the weaker market, listing

discounts actually shrank year-over-year to 10.7 percent from 11.6 percent,

although that’s still greater than the 9.2 percent achieved last quarter as buyers

were desperate to close by year’s end.

The East End market is typically most active in the first half of the calendar year, but

the number of sales jumped 52 percent in the last quarter of 2010, which acted more like a typical first quarter. That explains the similarities between the quarter-over-quarter and year-over-year declines, Miller said.

No part of the market was safe from the declines. The number of sales in the

Hamptons and in North Fork each tumbled about 22 percent from a year ago;

condominium sales and luxury home sales fell by 50 and 24.5 percent, respectively;

and the median sales price dropped across all price ranges.

Miller said he expects the market is on pace to return to near normal levels over

the next three months, which, compared to the depressed first quarter, will give the

appearance of a spike in the market. “But really,” he said, “the East End is a relatively

stable residential market.” He didn’t think the single-quarter results would

negatively impact consumer habits between now and the end of the second quarter.