New YorkJul 27, 2023Reuben Brothers in on Extell’s $500M debt deal at Central Park TowerSupertall snagged support from British billionaires on real estate expansion tear

NationalMar 25, 2023Nine days in hell: Inside the lending crisis that rocked multifamilyInstitutions collapsed, deals froze and fear took over. A look back at banking’s crucible

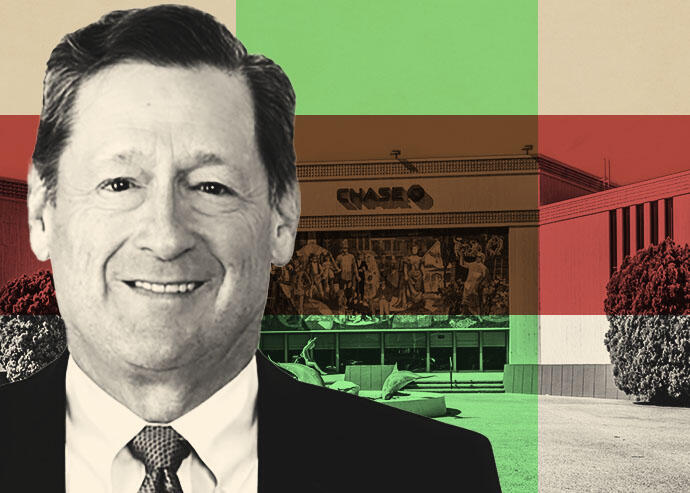

Los AngelesJan 19, 2023J.P. Morgan Chase buys retail portfolio in CaliforniaBank paid $138M for 22 sites it previously leased from MetLife