Tri-StateApr 19, 2024East Hampton eyes density for affordable senior housing Change could add dozens of units to three eligible properties

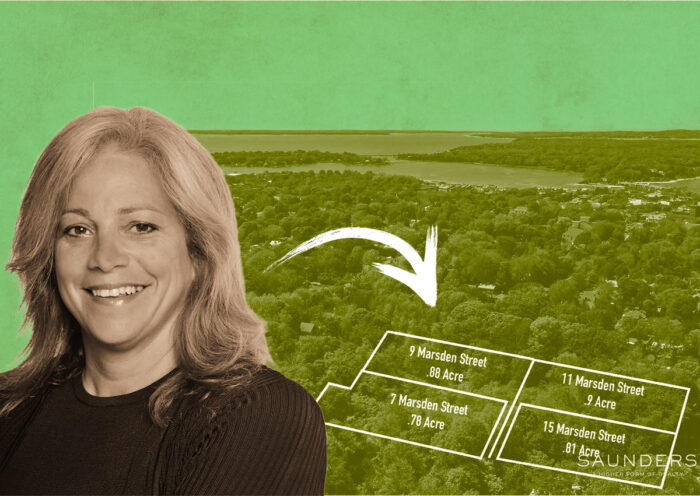

Tri-StateMar 27, 2024Sag Harbor lots sold after failed purchase by school district Marsden Street parcels likely to become housing

Tri-StateMar 19, 2024Church of Scientology buys Long Island office buildingRegional chapter pays $15M for Melville property