New York

Manhattan office leasing jumps as availability and rents drop

Manhattan office leasing jumps as availability and rents drop

LoanCore Capital sued joint ownership venture for alleged $193M default

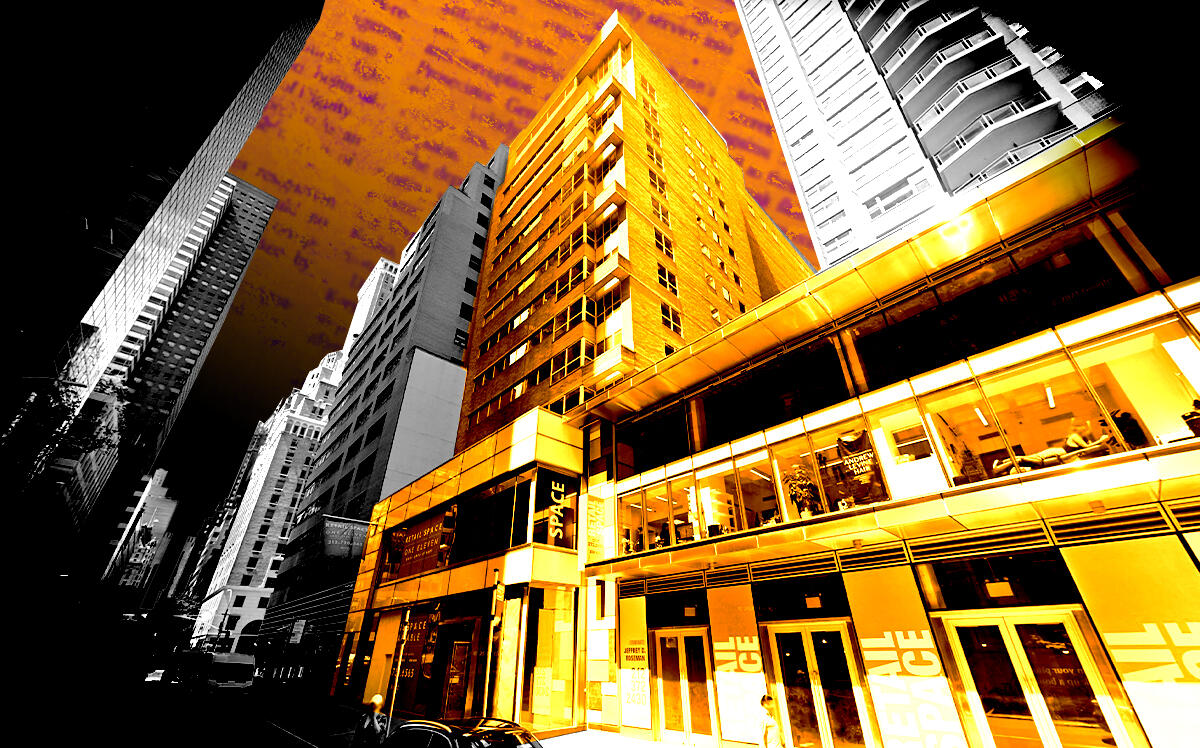

The owners of a Plaza District building could soon be persona non grata at the office and retail property.

LoanCore Capital filed a lawsuit this week against the joint venture at 111 East 59th Street, which also includes Dune Real Estate Partners, the Commercial Observer reported. The lender alleged the owners defaulted on $193.4 million in loans and is calling for the forced sale of the retail and office property.

Proceeds from a forced sale would go towards the alleged debt, along with legal bills, late fees and interest. None of the companies involved in the lawsuit responded to the outlet’s request for comment.

Partners Princeton International Properties, Dune Real Estate Partners and Empire Capital Holdings agreed in 2015 to buy the 15-story building from blindness advocacy nonprofit Lighthouse International for $170 million. The joint venture planned to convert the lower floors of the 200,000-square-foot building for a big-box retail tenant.

Princeton and Empire Capital exited ownership of the property in 2018.

In 2017, LoanCore Capital — an affiliate of Jefferies LoanCore — provided a $195 million financing package at the building. On top of a previous $103 million loan, the financing included a $50 million mortgage, an $8.6 million loan consolidated with a previous $16.8 million loan and a $7 million loan consolidated with a previous $9.4 million loan.

At the time of the loan, the developers were in the midst of a $20 million capital improvement project. Instead of trying to lure a big-box tenant, however, the venture was converting the bulk of the building into a medical facility while setting aside commercial space on the first two floors.

The lender alleges in the lawsuit the owners of the building defaulted in September 2020 after failing to pay off interest on the loans. Additionally, the building’s plumber’s insurance expired in June, leading to a partial stop-work order. Three months prior, the temporary certificate of occupancy for the first six floors expired.

The building is leased to Premier Medical Group and a cashier-free Starbucks.

Correction: A previous version of this article referenced Princeton International Properties as current owners of 111 East 59th Street, based on the Commercial Observer’s reporting on the suit. The firm exited the property in 2018, and the details from the suit have been updated.

— Holden Walter-Warner