Trending

New venture Staley Point Capital plans self-storage facility in LA Opportunity Zone

This the first project for the Century City-based firm was formed by Kevin Staley, co-founder of Magellan Group; and his son, who recently left Blackstone

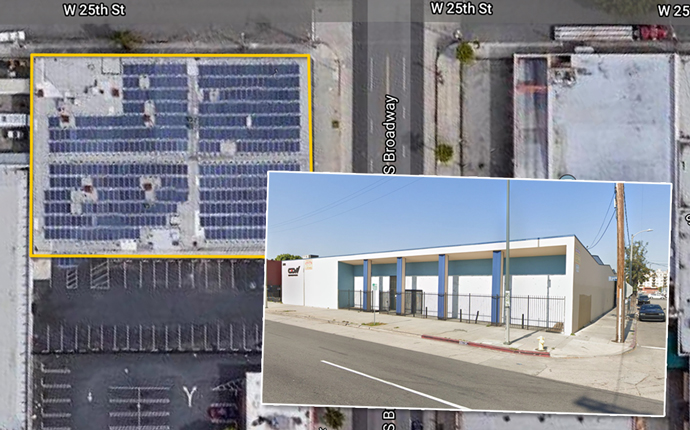

UPDATED, Jan. 17, 8:06 a.m.: For its first project, Staley Point Capital wants to demolish a 21,000-square-foot South Los Angeles light manufacturing complex it acquired last month and replace it with a sprawling “state of the art” self-storage facility, according to records filed with the Los Angeles City Planning Department.

Century City-based Staley Point is a new venture formed by Kevin Staley — who co-founded the Magellan Group — and his son, Eric, who recently left Blackstone Group, Eric Staley said.

In December, the investment firm paid $7.35 million for the site located at West 25th Street and Broadway. It plans to replace the existing structures with a 109,000-square-foot storage facility featuring 24-hour digital surveillance and controlled access.

This site is located in a federal Opportunity Zone. Over 8,700 such zones have been created across the country. Developers who undertake projects in them can realize significant tax benefits by investing their capital gains in the designated census tracts.

The zones have not been without controversy, and a group of Democratic lawmakers, including New Jersey Sen. Cory Booker, have requested that the Treasury Department’s internal watchdog investigate allegations that a site in Nevada was designated an opportunity zone because a Trump supporter planned a project there. According to data gathered by the accounting firm Novogradac, at least $7 billion has been invested in Opportunity Zones since the program went into effect.

Kevin Staley was also a former partner at Trammell Crow, where he oversaw the highly successful development of the Citadel, a former rubber manufacturing site, in the City of Commerce.

Overall, demand for industrial properties has been strong in L.A., in particular the Inland Empire, which has been at the center of much of the expansion. The appetite for distribution and last-mile centers helped push the local industrial market to the lowest vacancy rate of any major market in the U.S., according to a third quarter report from Cushman & Wakefield. Even with the addition of new industrial construction in L.A., vacancy isn’t expected to rise beyond 4 percent, according to the report.

Correction: A previous version of this article incorrectly stated that Magellan Group — which Kevin Staley also co-founded — was planning to build the self-storage property.