Source: Federal Deposit Insurance Corp.

Potentially shaky real estate loans held by Miami community banks more than doubled in the last year, according to the Federal Deposit Insurance Corporation, the agency responsible for maintaining stability in the nation’s banks.

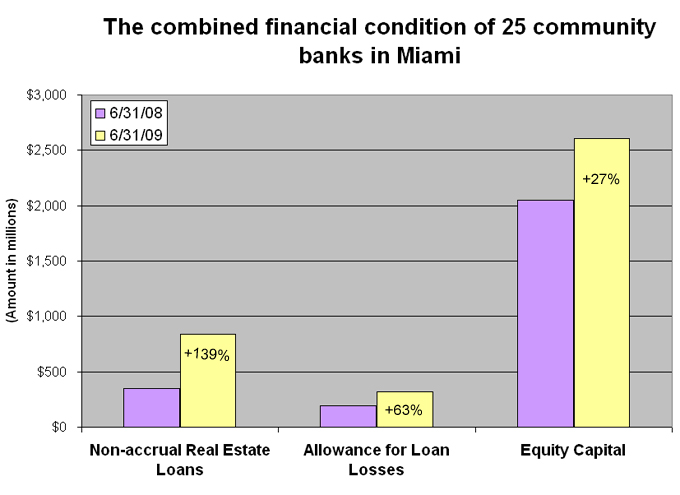

A review of financial statements for 25 community banks in Miami shows that they had $841 million of real estate loans that are classified as non-accrual, or unprofitable, as of June 30. That’s 139 percent more than a year earlier.

Some Miami banks have reported much faster growth in their non-accrual real estate loans. At U.S. Century Bank in Miami, for example, non-accruing real estate loans ballooned to $82 million on June 30 from $14 million a year earlier, a 585 percent increase.

“I don’t think anybody can be comfortable with what’s going on there,” said Octavio Hernandez, president of U.S. Century Bank in Miami. But “we are strong enough and capitalized enough that we can weather the storm.”

The figures show that real estate loan problems are mounting at small banks in Miami, not just at big ones. Most of the 25 banks reviewed have less than $1 billion in deposits.

“A lot of times, community banks will say, ‘We didn’t cause this [financial] crisis. It was caused by the big banks, not the small community banks,’” said Ken Thomas, an independent bank analyst based in Miami. “That’s not really correct, because all the banks got caught up in this.”

Financial statements filed with the Federal Deposit Insurance Corporation also show that many community banks in Miami failed to increase reserves for possible loan losses as fast as their non-accrual real estate loans have increased. The 25 banks increased their combined reserves for possible loan losses in the 12 months ended June 30 to $316 million from $198 million a year earlier, up 63 percent.

The average U.S. commercial bank has a loan-loss reserve equal to between 60 percent and 65 percent of its non-accrual loans. But this so-called reserve ratio is much lower at most FDIC-insured banks in Miami-Dade, Broward and Palm Beach counties, Thomas said.

“In South Florida, banks are way under-reserved,” he said. “Many banks are below 25 percent. There are some below 10 percent.”

Thomas said some banks are reluctant to add to loan loss reserves because each addition reduces their profits or increases their losses.

“When you have a problem loan that has not yet been charged off, you have to reserve against it. The problem is that lots of the banks are very low on their reserves,” he said. “Some banks are delaying the day of reckoning by taking low loan-loss provisions. They are avoiding reporting big losses, because if you have to increase your allowance for loan losses, you lower your earnings.”

Many banks are trying to raise additional capital to increase their reserves for loan losses and for other purposes. At least two community banks in Miami, U.S. Century Bank and Biscayne Bank, have obtained equity investments through the U.S. Treasury Department’s Troubled Asset Relief Program, or TARP.

The Treasury Department has approved TARP loans of $6.4 million to Biscayne Bank and $50 million to U.S. Century Bank. The banks can count the loan money as equity capital until they repay it.

But “there are no sources of capital for many of these small community banks,” said Bowman Brown, a Miami attorney who works with financial institutions. “Those that are distressed don’t have access to TARP funds, and their shareholders generally are not in a position to, or not willing to, further capitalize the banks.”

Though some loan problems at Miami community banks are self-inflicted, “for the most part, it’s the downturn in the real estate market,” Brown said. “There was no way to manage out of that if you did business in Florida because so much of the banking business in Florida is real estate related.”