Sales of Manhattan development sites slowed significantly in the first months of 2016, adding to broader concerns over the health of the New York real estate market.

A mere $90 million worth of development deals were recorded in the borough in January and none in February, according to data from Real Capital Analytics. Brokers blame a drop in demand on tighter financing markets, weakening luxury condo sales and the expiration of the 421a tax abatement program.

“Seller expectations are higher than buyers are willing to pay,” said Shimon Shkury, president of brokerage Ariel Property Advisors. “We will see throughout the year a dramatic decline in transaction volume – not just in Manhattan, but pretty much everywhere.”

Bob Knakal, who heads New York investment sales at Cushman & Wakefield, argues that the average market value of development sites has fallen by 25 to 30 percent over the past few months. That price drop isn’t reflected in sales data because most sellers have yet to accept the new market reality and adjust their expectations downward, he explained. Until they do, he said, few sites will trade.

Diverging expectations between buyers and sellers are a telltale sign of a turning point in the market. Many sellers, buoyed by some $1,000-per-buildable-square-foot land deals in 2015, are still gunning for a big payout. According to Ariel Property Advisors, development sites below 96th Street currently ask $800 per buildable square foot on average (the average sales price in 2015 was $610).

“The challenge,” said Jim Costello, senior vice president at Real Capital Analytics, “is that existing owners of potential development sites probably have a price in their heads related to the prices that the previous transactions achieved,”

But buyers now balk at those prices. A key culprit: weakness in the high-end condo market, which accounted for a large share of Manhattan’s new development activity over the past three years. “When you can buy and sell out a building as condos you can afford to pay more for the land and that kind of got into everybody’s mind,” said Bob Faith, CEO of real estate fund manager Greystar. “Now you’re starting to see a pause.”

As luxury condos begin to flail – average days on the market increased precipitously in late 2015 – lenders have tightened financing conditions on the new development market. In turn, “Developers who have multiple projects have said ‘you know what, let me make me sure I can finance what I have as opposed to buying new sites,’” said HFF’s Eric Anton. He believes the development slowdown is “directly linked to the uncertainty in the capital markets.”

The expiration of the 421a tax abatement program at the beginning of the year has had a far bigger impact in Queens and in Brooklyn. Brokerage TerraCRG expects new development deal volume in Brooklyn to plummet from $2 billion in 2015 to around $700 million in 2016.

This hasn’t stopped a number of sizable development sites in the outer boroughs from hitting the market in recent months, particularly in Queens, where a trio of five-acre-plus sites are listing for north of $100 million.

Overall, rentals using the 421a abatement account for the majority of development activity in both boroughs. In contrast, condos and mixed-use towers dominate development in Manhattan. But the program’s expiration adds to uncertainty and makes it harder to substitute rental development for condos as the latter become less profitable.

Under pressure from a weak condo market, tight financing and 421a expiration, development-site sales volume has been on a downward slope since October after a strong showing in the first half of 2015, according to RCA data.

The dip in land sales comes as the broader New York real estate market shows signs of a slowdown amid turmoil in global capital markets. Manhattan investment sales volume across all asset types fell to $6.6 billion in the first two months of 2016 – down 40 percent from the $11.2 billion in sales during this period last year.

New development sites tend to perform worse than core assets in turbulent times because of the risks associated with new construction. “Manhattan is probably feeling the slowdown the most,” said Hodges Ward Elliott’s Daniel Parker, “because land has been priced for condo construction for so long.”

That’s not to say no sites are trading, or that everyone is pessimistic. For example, Lloyd Goldman’s BLDG Management recently bought an assemblage on East 38th Street for $36.7 million and China Oceanwide Holdings just closed on its August contract to buy 80 South Street for a staggering $390 million. Tishman Speyer also closed on the acquisition of a development site across from the Jacob Javits Center for $185 million, where a 1.3 million-square-foot office tower is planned (this deal wasn’t included in the RCA figures because of its unconfirmed purchase price).

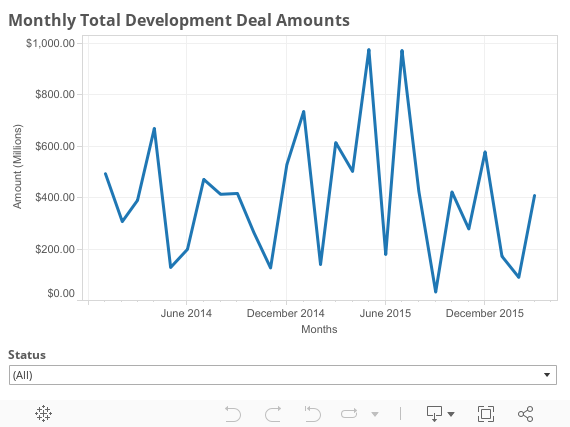

RCA’s data for Manhattan development sites only counts vacant buildings and empty lots, but new development often starts with the purchase of an income-producing asset. When you include sales of income-producing buildings likely to become new development, the drop is less dramatic (see chart above, also based on RCA data) and volume recovered somewhat in March. But unless a flurry of deals takes place between now and April 1, the year-to-date volume of $670.4 million is still significantly less than the $1.49 billion in deals recorded in the first three months of 2015 or the $1.19 billion recorded in the first three months of 2014.

“I am not seeing development stop dead in its track,” said Adelaide Polsinelli, a broker at Eastern Consolidated, who recently arranged the sale of a development site at 216 Bowery for $13 million. While demand for development sites is still strong, investors are “looking at deals differently now,” she said. Buying existing buildings with air rights and developing office properties are in, she claimed, while vacant lots and condo development are out. RCA’s Costello also cautioned that it’s too early to call weakness in the new development market. “A couple more low quarters and one could say that it is off peak,” he said.

Others are more pessimistic. Robert Knakal expects deal volume to stay depressed until mid-2017 before prices adjust down. “Generally, as we saw in the last cycle, it takes 18 months to two years (for the sellers) to get used to new normal,” he said.

Greystar’s Bob Faith agreed. “Most landowners don’t have to sell,” he said. “So capitulation typically takes a while.”