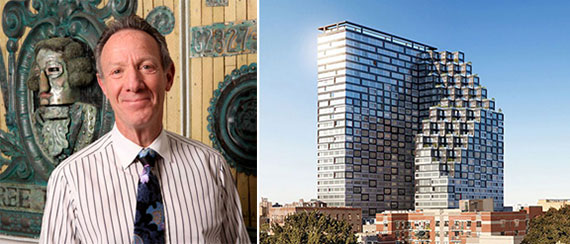

In December, Kevin Maloney and Kamran Hakim gave up on a development site in Long Island City they’d spent nearly three years assembling. The partners wanted to build a $750 million, 914-foot-tall rental and condominium skyscraper on the site, but couldn’t go the distance.

The stakes were high. They’d taken on more than nearly $140 million in acquisition and predevelopment loans from Acres Capital that were coming due in a matter of days, and lenders weren’t willing to give them a construction loan unless the sponsors pumped in more equity into the deal. Their choices: sell, or face the prospect of foreclosure, sources said.

“It was too big for us,” Hakim said.

In Maloney and Hakim’s woes, the Durst Organization [TRDataCustom] saw opportunity. The cash-rich developer, which controls more than 13 million square feet of Manhattan office space, acquired the site at 29-37 41st Avenue for between $167 million and $175 million (the number varies depending on whether you ask the buyer or sellers). Durst’s low basis will allow it to develop the project as a rental.

“We cannot compete with condo builders on cost when acquiring land conventionally,” the firm’s CEO Douglas Durst told The Real Deal. “Acquiring distressed sites allows us to build rental and make the kinds of long-term investments that have served us well for more than 100 years.”

Renderings of Queens Plaza Park in Long Island City and Douglas Durst

For Durst and others looking to benefit from sponsors in a tight spot, now seems the time to pounce. Many are earmarking funds specifically to swoop in when the original sponsors of a project find themselves running out of cash or unable to score a construction loan. This may involve taking control of the site, as in the case of the Clock Tower, or simply a fresh equity injection that makes the project’s loan-to-value ratios more palatable to traditional banks.

“One thousand percent, I see capital being set aside for this, whether it be predatory or not,” said Nicholas Mastroianni, CEO of the U.S. Immigration Fund, which helps developers raise funds through the EB-5 program.

Some investors aren’t shy about their white-knight intentions, and expect to get rewarded handsomely.

“We’re certainly looking at this space,” said Christopher Sameth of Kuafu Properties, a New York-based investment firm that is backed by Chinese private equity. “We’re getting ourselves organized to help be a solution to the problems we expect to present themselves in 2017. There should be ample opportunities for new capital to go into deals at a basis they’re comfortable with and get paid well for doing it.”

Craig Solomon, a managing principal at real estate investment firm Square Mile Capital, said his company is “looking at a number of these deals as we speak.”

“Without being penal,” he added, “the capital that is solving some of these problems will enjoy very favorable risk-adjusted returns.” In most cases, “you’d be talking about equity-type returns being enjoyed at more senior parts of the capital structure than typical common equity.”

Year of reckoning

For developers who bought parcels at ambitious prices during the exuberance of 2014 and 2015, 2017 may be the year when those deals come home to roost.

“Some deals were put together in very heady times and with a belief that the market was going to remain as lofty as it was at the time,” said Michael Lefkowitz, a real estate attorney at Rosenberg & Estis.

From January 2014 through June 2016, New York City saw about $28 billion in land trades, $18 billion of that in Manhattan, according to data collected by Kuafu. Most of those deals were financed through short-term land acquisition loans. The take-out for those loans are typically construction loans, but with high-end condo sales slowing and banks facing heavier regulation, traditional lenders aren’t stepping up to provide them.

“I don’t think anyone anticipated the pullback in the construction market when they were buying development sites during this period,” Sameth said.

Developers’ profit margins were already tight because of high land costs. Now, they’re being forced to fork out for the associated carrying costs as they scramble to secure construction financing for their sites. And since land and acquisition loans typically expire within 24 to 36 months, these sponsors could be left stranded.

“You’re going to see 25 or 30 percent of these loans coming due this year,” Mastroianni said. “Some people are going to lose their sites. Some are just going to require restructuring.”

Loans coming due this year “are definitely going to be at a lower proceed level than would have been underwritten in 2014 and 2015,” Sameth said. “Projects will need additional equity, either from the existing partnership or from an outside investor, to fill the gap.”

Dustin Stolly, a financing broker at JLL, said lenders are typically looking for sponsors to provide 35 to 40 percent more equity before they’ll even consider them for financing.

“If you’re not a tier-1 developer or a household name, you’re running into a lot of issues,” he said.

But even developers with pedigree are hurting. Gary Barnett’s Extell Development, for example, hoped to have scored a construction loan for its Central Park Tower project at 217 West 57th Street before its $235 million land loan came due. But in December, Extell had to refinance the land loan.

Plenty of other developers are on the hunt for construction financing to take out their land loans.

They include the likes of Michael Shvo, Bizzi + Partners and New Valley, who are still trying to finalize a $500 million-plus construction loan with United Overseas Bank for their Financial District condo skyscraper at 125 Greenwich Street, and Victor Group and Lendlease, which are in talks for a loan for their Rafael Viñoly-designed tower at 281 Fifth Avenue. The acquisitions loans on both projects come due this year, sources said.

Some of their well-capitalized counterparts, such as Kushner Companies, Fisher Brothers and RXR Realty, are looking to take advantage of the construction lending drought by providing debt.

Shang Dai

Kushner Companies, for instance, recently provided a $33 million loan to Toby Moskovits’ Heritage Equity Partners for a new mixed-use office-and-retail project at 215 Moore Street, replacing a prior senior mortgage from Richmond Hill Investment Company. The firm is also a mezzanine lender on JDS Development Group’s and Chetrit Group’s supertall mixed-use tower in Downtown Brooklyn.

“Right now, come in to lend money,” Kuafu’s CEO Shang Dai said in November. “You will either become the hero,” or become the owner at a discount if the project goes south. “Either way, you will sleep well at night.”

The fallout

The market has already seen some notable casualties this cycle. In 2013, Continuum Company’s Bruce Eichner paid Vornado Realty Trust about $65 million for a site at 1800 Park Avenue. Buying the site with high-interest debt from Garrison Investment Group, Eichner announced a bold plan to build Upper Manhattan’s tallest towers, a pair of 32-story mixed-use buildings with 682 rental apartments. But even as he scrambled to secure financing, the Durst Organization made its move: It purchased about $100 million in distressed debt on the property from Garrison, and moved to seize the site, eventually cutting a deal with Eichner and taking control of it in May for $91 million.

From left: Ian Bruce Eichner and a rendering of 1800 Park Avenue in Harlem (credit: ODA)

And in December, Joseph Beninati lost a development site at 3 Sutton Place site to his lender, N. Richard Kalikow’s Gamma Real Estate. Sources blamed Beninati’s failure on his scanty track record in Manhattan, which made banks nervous and unwilling to finance him, and on his high-interest debt fueled plan to add even more luxury condos to what observers feel is a saturated market. Beninati’s dream, sources said, would have been out of reach even in the best of times.

But the vultures aren’t just eyeing train wrecks.

“For every 3 Sutton situation,” Solomon said, “there are going to be dozens of situations that are more conservatively capitalized but still require recapitalization.”