Sales price for market-wide Brooklyn apartments (source: the Corcoran Group)

The Brooklyn residential market may have made inroads in its recovery thanks to a surge in new development transactions, but sales are still down in Queens as the borough continues to feel the impact of the expiration of the homebuyer tax credit, according to separate second-quarter residential sales market reports for the two boroughs released today by Prudential Douglas Elliman and the Corcoran Group.

Overall, prices saw moderate quarterly increases in Brooklyn, with sales remaining at about the same level as last year, the Elliman report, prepared by Miller Samuel, shows.

The overall median sales price increased 3.7 percent to $480,000 from $463,000 in the second quarter of 2010.

Luxury sales, the upper 10 percent of all sales, mostly in new developments, propelled overall sales volume with the lower limit of the top 10 percent of all sales reaching $969,000. The median sales price for a luxury property was $1.3 million, up 14 percent since the second quarter of 2010.

Brooklyn condominium unit sales jumped 11.4 percent in the second quarter, with the median sales price hitting $525,000, up 8.2 percent from the same three months in 2010. Co-op sales increased by 8.7 percent to 351 units and sold for a median price of $260,000, down 3.7 percent from the prior year quarter. Only one- to three-family property sales declined in the borough, 9.9 percent to 846 units, from 939 units in 2010.

“Stable, I think is the theme,” said Jonathan Miller, president of Miller Samuel. “We’re a year out of the tax credit, which wreaked havoc on sales statistics. On the whole, overall prices trended mostly upwards while resales remained flat.”

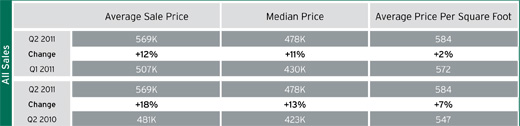

Corcoran’s second-quarter Brooklyn report shows a similar story in terms of new developments. The company attributes an overall 13 percent Brooklyn market-wide median price increase to heightened new development activity as well as a shift into larger three-plus bedroom residences.

The report shows an average per square foot median price increase of 7 percent compared to the second quarter of 2010.

In terms of market share, Williamsburg and Greenpoint accounted for 19 percent of overall sales in the second quarter due to sales at the Edge, Two Northside Piers and 80 Metropolitan, up from 14 percent at the same time a year earlier, the Corcoran report shows. Brooklyn Heights also increased its market share to 19 percent from 14 percent, thanks to closings at several submarket developments, including be@Schermerhorn.

“It’s a very strong picture,” said Leigh Godwin, senior managing director at Corcoran’s Williamsburg office, “and I think we’re going to see more of the same.”

Godwin pointed to other recently-opened Corcoran-marketed developments such as 75 Clinton Street in Brooklyn Heights and 46 South 2nd Street and 29 South 3rd Street, both in Williamsburg, that were still selling strongly moving into the third quarter. “We’ll see those sell out in the coming quarter,” she said of the latter two properties.

The Elliman report paints a bleaker picture for Queens, with overall sales down 40.6 percent, to 2,631 from 3,972 in the second quarter of 2010.

Miller attributes the Queens sales drop to two factors. “In Queens,” he said, “the relationship of new development to the overall market is much smaller [than in Brooklyn]. New developments make up only 8.9 percent of total sales activity,” compared with 24.6 percent in Brooklyn. “The overall price point is also somewhat lower [and] the lower the price point, the greater the impact felt by the tax credit.”

However, both Miller and Michael Guerra, Elliman’s executive vice president and director of sales in Brooklyn, warn that the Queens figures are somewhat skewed as a result of artificially inflated prices in the prior year quarter thanks to people buying before the expiration of the tax credit in mid-2010.

“Queens was significantly impacted by the expired tax credit,” Guerra said. “If there were a way to filter out the tax incentive, what we’d see would be far more in line with what we’re seeing in Brooklyn. The hallmark of this report is that across the board you’re seeing stability. You’re seeing incremental ups and downs once you filter out the tax credit and surges.”

While sales were down, prices don’t seem to have suffered too much. Borough-wide price indicators show modest quarterly increases; the median overall sales price for a Queens home increased 2.1 percent, to $342,000 from $335,000 in the second quarter of 2011. Listing inventory fell slightly below the prior year level, and the new development condo market share reached a three-year high.

The median sales price for a condo was $278,222, up 36 percent from the second quarter of 2010, but the volume of condo sales dropped 61 percent to 359 units. Co-op sales also fell by 16 percent to 676 units, with the median price for a Queens co-op dropping to $190,000, down 1.6 percent from the previous year. The median sales price for a one- to three-family home was also down by 2.3 percent, to $428,500, with sales falling by 41 percent.