New YorkApr 1, 2024Why New York’s condo market is a delicate balancing actNew condos remain in demand in New York City, but economic forces and pensive developers could dry up the inventory pipeline soon

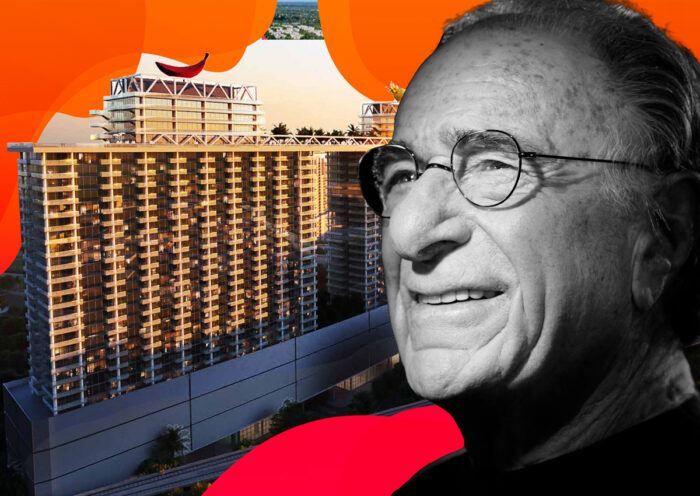

South FloridaMar 12, 2024Harry Macklowe wants to sell Miami development site near Dadeland MallMacklowe paid $32M for the property, financed the deal with a $39M loan

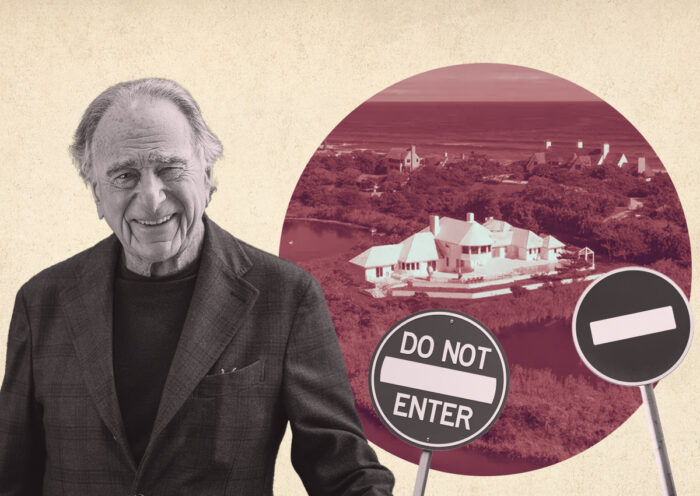

Tri-StateMar 5, 2024Harry Macklowe’s Hamptons home not legally habitable Developer asking $38M for estate mired in fight with East Hampton