With new rental projects becoming harder and harder for developers to pencil out in Manhattan as the price of land and construction rises, it would make sense to assume that rental inventory would be shrinking. In reality, new rental inventory is expected to grow over the next two years, but the trend is not forecast to last much beyond that time frame.

The rental market in Manhattan south of 96th Street is projected to expand through 2016 as the pipeline of projects developed over the past several years comes to market.

The prime area of the city is projected to see a roughly 25 percent uptick in new rental apartments this year to 4,152 units (up from last year’s number of 3,313) and then more than double in 2016 to almost 8,800 units, according to the brokerage Citi Habitats.

For developers and landlords the near-term onrush could give way to concerns of a glut, but Jim Hedden, chief development officer for Rose Associates, said he thinks demand is strong enough to offset the additions on the supply side.

“Is it staggering? I look at some studies and it doesn’t scare me,” said, Hedden, who is bringing one of Manhattan’s largest rental developments to market this year, 70 Pine Street.

“As a rental guy, I think [in 2015 and 2016] you’re going to see the pipeline deals from ’13 and ’14 and it’s going to fall off after that. There’s just no land available and everything is priced for condos.”

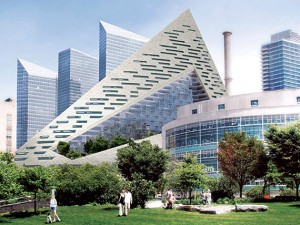

The Durst “pyramid” building on West 57th Street will include 709 rentals.

In fact, new inventory is expected to reverse course in 2017 and decline 14 percent to 7,540 apartments, according to the brokerage’s projections. And the culprit, industry pros say, is the sky-high prices development sites are fetching these days that almost necessitate condos as opposed to rentals.

In the short term, the increase this year is largely the result of a couple of mega-projects, most notably the Moinian Group’s 1,174-unit 605 West 42nd Street, the Durst Organization’s 709-unit “pyramid” on West 57th Street and Rose Associates’ aforementioned 70 Pine Street, which will deliver 644 units.

Projects like these work either because the developer has owned the sites for many years or was able to lock them in at attractive bases, industry watchers say. But in today’s market, those rental-appropriate development sites are becoming harder and harder to find.

By way of comparison as to how these projects began on paper, Moinian paid an average of roughly $205 per buildable square foot in 2005 and 2007 when it purchased the two Far West Side parcels that made up the development site for its 60-story-tall rental tower.

By last fall, the average price for a buildable square foot in Manhattan had climbed to $548, up 23 percent from the year before, according to commercial brokerage Massey Knakal Realty Services.

Oskar Brecher, Moinian’s executive vice president and director of development, said that shortly after the recession, the developer considered the project as a condo in the face of a potential condo inventory crunch.

“But as the [overall real estate] market improved, we concluded the financing could work as a rental and we moved the building over to a much simpler scope,” he said.

Nowadays, considering the price of land and the underwriting challenges for rentals, Brecher said developers will have to get more creative when putting together projects that pencil out soundly.

“It’s much more difficult to make the numbers come together,” he said.

Rose got involved with 70 Pine in 2012, when it bought out the stake held by the partnership of Ronnie Bruckner and Nathan Berman’s Metro Loft Management, which for a short time had planned to do a condo conversion at the former headquarters of American International Group.

Rose’s Hedden said the two teams’ divergent approaches came down to “philosophical differences,” and that the decision to steer the project to a rental was “never much of a discussion.”

One result of the higher prices developers are paying for property these days, he said, is that it pushes minimum rents up to the areas of $75 and $80 per square foot.

“What we found in the market is that the people who pay those types of prices expect certain finishes and a certain lifestyle,” he said. “It’s driving the product to a higher level of finish than what was put out five or six years ago.”

“So what you’re seeing then is the life cycle of finishes used to be 10 to 15 years. Now it’s five years. It gets updated a lot quicker and adds to the acceleration of the rent,” he said, adding that the demand for the latest finishes and amenities creates “room for growth in those rents.”

Andrew Heiberger, the CEO of Town Residential, said that because of “rising costs of land and exorbitant construction budgets, we will see few ground-up rental projects in Manhattan.”

Meanwhile, rising employment numbers and tight credit restrictions for first-time homebuyers have been pushing Manhattan rents up for nearly a year.

The median price for a Manhattan rental climbed to $3,250 in December, capping 10 consecutive months of year-over-year gains, according to the most recent market report for Douglas Elliman released by appraisal firm Miller Samuel. That’s a 4.8 percent bump on the year. And with the dearth of new rental construction on the horizon, prices are expected to continuing rising.

The lack of construction “coupled with the increasing trend of existing rental projects converting to condo, will cause a ripple effect in the rental market with monthly rents rising as high as 5-10 percent in 2015,” Heiberger told The Real Deal last month.

MNS CEO Andrew Barrocas also said prices will continue to climb, “I’m not saying, ‘Hey, I think it’s going to increase.’ I know it’s going to increase,” Barrocas said.

Moving out of Manhattan

Manhattan is not the only borough in New York City that will see more rental units coming online this year. In fact, the number of units coming to market in Brooklyn is expected to jump 120 percent to 6,527 units from just shy of 3,000 in 2014, according to Citi Habitats.

World Wide Group is building 41-50 24th Street, a Long Island City rental.

In Queens, Long Island City is forecast to add 1,800 new rentals this year, a bump of 87 percent over last year.

And the swell of units in those places, sources say, is a direct result of the changing face of the rental landscape in the city.

“It’s no longer a stepsister to Manhattan, but to many people it’s more desirable than Manhattan,” Scott Avram, senior vice president at Lightstone Group, said of Brooklyn, echoing a common refrain.

The firm is working on a pair of large rental buildings in Gowanus, at 363-365 Bond Street. National home builder Toll Brothers originally planned to do a 450-unit condo building at the site, but when they got bogged down in a rezoning process, Lightstone picked the project up for $33.15 million in 2013 and decided to reposition the two buildings as 700 rental apartments.

“It’s one of those niche neighborhoods where the rents, from the developer side, are so strong that we could not look away,” Avram added.

Town’s Heiberger noted that Brooklyn, along with areas such as Jersey City, Hoboken, Astoria and Long Island City, are all benefitting from “Manhattan’s white-hot sale and rental markets.”

Rents in Queens were up 5.9 percent on the year in December, with a median price of $2,839, according to Miller Samuel. In Brooklyn, the median price of $2,900 was up 9 percent on the year.

David Maundrell, founder and president of the brokerage aptsandlofts.com, said the rental surge in Brooklyn is as strong as he’s ever seen it.

While land and construction costs are also on the rise in Brooklyn and Queens, they are still far lower than they are in Manhattan, making it easier for developers to pencil out the numbers and convince lenders to provide financing.

Maundrell said that back in 2006, when Brooklyn was in the midst of a condo boom, “there were no major rental projects here.” The rentals that did come online were the “shadow product,” projects envisioned as condos that switched course mid-stream because of financial struggles.

“The enormous amount of product on the rental side” today has different roots, he said, though he noted that renters are still discerning.

“The renters are there and they’re willing to pay top dollar, but the product has to be worth it,” he said.

Condos grow at faster clip

While developers are delivering more rental units in Manhattan this year, rentals in the borough are a decreasing percent of the new residential pie.

Lightstone Group picked up 363-365 Bond Street from Toll Brothers, and is building 700 rental units on the Gowanus property.

Last year, rental units in Manhattan accounted for 58 percent of the new residential product, according to Citi Habitats. This year, they will make up only 41 percent.

That is because condo production is projected to outpace growth on the rental side this year, expanding roughly 150 percent to 6,097 units.

The opposite is true in Brooklyn, where rental growth outpaces condos. New rentals are expected to make up more than 80 percent of the market in Brooklyn, as well as in Long Island City.

On the rental rate front, some analysts point out that the reason for increases in Manhattan is that there’s an inherent demand for rentals because the tight credit market still makes it difficult for many to buy.

“The reason rents have been rising, or at least have been at a high level for the last three or four years, is not unique to Manhattan. It’s a function of tight credit,” said Miller Samuel’s Jonathan Miller. “People are tipped back to the rental market and it creates a logjam. This is a national phenomenon.”