New York’s real estate industry is keeping a close eye on Capitol Hill – and not just because the U.S. Senate is debating the future of the EB-5 visa program. In March, the House financial services committee quietly passed a bill that could have a big impact on commercial real estate lending.

Dubbed the Preserving Access to CRE Capital Act of 2016, the bill would soften restrictions on CMBS issuance that are set to take effect in December. It still faces a vote in the House of Representatives – which may be a tall order in an election year. But if the bill passes, it would make a lot of real estate lenders — and borrowers — very happy.

A bit of background: In December 2016, new risk retention rules for CMBS issuers under the Dodd-Frank Wall Street Reform and Consumer Protection Act will take effect. The new rules require CMBS issuers to keep five percent of a loan’s value on their books – as opposed to selling all of it in the form of bonds. Issuers can pass this share on to B-piece bondholders, but only if the bondholders agree to not sell the CMBS for at least five years.

Arkansas Congressman French Hill

These risk-retention rules are a cornerstone of post-2008 financial reform. By forcing CMBS issuers to hold on to some of the bonds they issue, the rules are designed to discourage risky lending of the kind that proliferated during the housing bubble. But by forcing issuers to spend more of their own capital on bonds, the rules are also bound to drive down their profit margins and restrict the volume of loans they can issue, likely making credit more expensive.

“It’s definitely a big topic. Even as early as December of 2015 people started to express their concerns over it,” Sean Barrie of CMBS research company Trepp told The Real Deal. “It will make CMBS lending a more tricky outlet.” He added that smaller issuers are likely to be hit hardest by the new rules.

Enter the Preserving Access to CRE Capital Act, introduced by Arkansas Representative French Hill. The bill would exempt single-asset or single-borrower CMBS from the risk retention rule. It would also make it far easier for CMBS pooled together from different borrowers to get an exemption, for example by scrapping term requirements.

Numerous trade groups, including the Appraisal Institute, the National Association of Realtors, the International Council of Shopping Centers and the U.S. Chamber of Commerce are lobbying legislators to support the CRE Capital Act of 2016. “Barring some form of relief, borrowers [in] many smaller commercial markets across the country may not be able to finance projects that could spur development and create jobs in the areas that need it most,” the trade groups wrote in a joint letter sent to the House of Representatives on March 2.

Data: Morningstar Credit Ratings

There’s a reason virtually all major real estate trade groups support the bill: the industry has become accustomed to cheap CMBS financing over the past couple of years and fears a painful withdrawal. Even in Manhattan, where CMBS lenders tend to play second fiddle to balance-sheet lenders like banks and insurance companies, $26.7 billion in CMBS loans were issued between January 2014 and February 2016, according to Trepp. Costlier debt typically translates to lower real estate prices, which could exacerbate a market slowdown.

In February, turmoil in global bond markets and the prospect of risk retention rules combined to drive mid-sized CMBS lender Redwood out of business and led to broader concerns over the health of the CMBS market. “We have concluded that the challenging market conditions our CMBS conduit has faced over the past few quarters are worsening and are not likely to improve for the foreseeable future,” the firm’s CEO Marty Hughes said in a statement on Feb. 9.

Bond markets have since calmed. The spread between 10-year Treasury swaps and most types of CMBS bonds fell between February and April, according to Trepp.

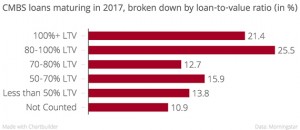

But the onset of risk retention could drive spreads up again at the worst possible time. A staggering $99.47 billion in U.S. CMBS loans are set to mature in 2017 – up from $52.42 billion this year – according to a recent report by Morningstar Credit Ratings. 46.9 percent of those loans have a loan-to-value ratio of 80 percent or more (see chart above), and Morningstar reckons “successfully refinancing many of these loans will be very difficult without sharp improvement in cash flow through 2017.”

From the industry’s perspective, this flood of high-risk loans maturing is a good argument in favor of keeping credit cheap and available. But lawmakers could equally interpret it as another reason to tighten standards to avoid this kind of instability in the future.

In a 39-18 vote in the House financial service committee on March 2, Democrats and Republicans supported the Preserving Access to CRE Capital Act. For CMBS lenders and the industry they service, this could be a good omen.