Every day, The Real Deal rounds up New York’s biggest real estate news. We update this page in real time, starting at 9 a.m. Please send any tips or deals to tips@therealdeal.com

This page was last updated at 6:19 p.m.

The controversial rezoning of Industry City is set to get a greenlight. Brooklyn Councilmember Carlos Menchaca has reportedly reached a deal with the complex’s landlord, which is a partnership between Jamestown, Belvedere Capital and Angelo Gordon. Menchaca previously said the rezoning would be “dead on arrival” if the developer didn’t delay its application. The owners agreed to set aside up to 900,000 square feet of the complex’s space for manufacturing. Other concessions include adding a vocational school and redoing the area’s streetscape. [Crain’s]

Brooklyn’s most expensive home is listed for $18 million. The mansion at 88 Remsen Street, which was built in the 19th century, has six bedrooms, two kitchens and a carriage house at the rear. It previously fetched the highest Brooklyn sale price in 2008 for $10.8 million. [Curbed]

Forever 21 is planning to file for bankruptcy as soon as Sunday. The retail chain could close as many as 700 stores in such an event, bringing an end to months of hemorrhaging money while it struggled to secure a loan. [WSJ]

WeWork CEO Adam Neumann (Credit: Getty Images)

Adam Neumann (technically) lost $10 billion. The WeWork founder’s 22 percent stake was reportedly pegged as high as $14 billion earlier this year. But after a rocky path to the company’s IPO, its valuation has plummeted, and Neumann’s stake is now worth closer to $3 billion. [Bloomberg]

A penthouse in one of New York’s most exclusive buildings is for sale at $65 million. The 5,902-square-foot duplex at 15 Central Park West, was purchased in 2008 for $30 million by Lindsay Rosenwald, a bio-pharma investor. Another unit was sold in the building last month for $57 million. [WSJ]

Harlem’s tallest new building is for sale. The 300-foot high tower at 233 West 125th Street, which is currently being constructed by hotel developer Lam Group, is being marketed for an investment or sale with an option to take advantage of tax benefits afforded by the Opportunity Zone program. The developers have so far poured $178 million into the project. [NYP]

Low rates are increasing loan enthusiasm. Mortgage applications jumped 2 percent last week, compared with the previous week, and remained 69 percent higher than the same week last year. Interest rates are also down slightly; the average contract interest rate for a 30-year fixed rate mortgage with conforming loan balances dropped to 3.82 percent from 3.87 percent over the week. [CNBC]

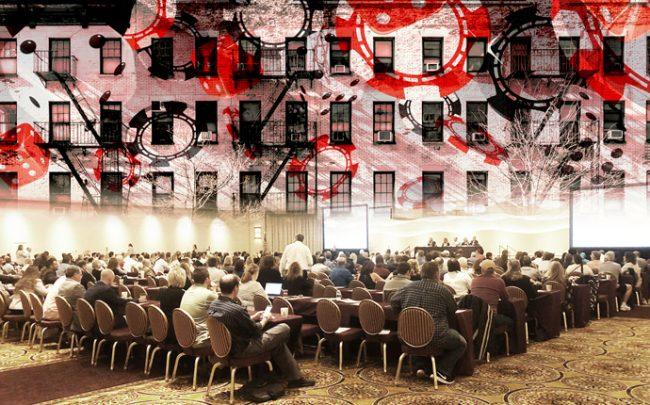

The massive meeting held in a suburban casino outside of Utica came at a time when the real estate industry is asking itself some tough questions. (Credit: iStock)

Meet the 400 landlords that are taking rent laws into their own hands. At an Upstate New York casino Tuesday, building owners gathered at an event to plan the industry’s path forward after decades of landlord friendly rent laws were rolled back over the summer. [TRD]

Softbank CEO Masayoshi Son and WeWork CEO Adam Neumann (Credit: iStock and Getty Images)

SoftBank has some leverage over WeWork’s IPO. While the Japanese conglomerate doesn’t have control of WeWork’s board to override an IPO, it does have significant levers to pressure WeWork. In addition to the billions of dollars it has invested, it also has control over WeWork’s Asia business and is yet to release a $1.5 billion commitment. [TRD]

A Fifth Avenue co-op sold at a $67 million discount. The 12,000-square-foot duplex at 834 Fifth Avenue previously owned by the John Gutfreund, the former CEO of Salomon Brothers investment bank, was purchased for $53 million by billionaire trader Stanley Druckenmiller. As recently as 2016, the property was listed for $120 million. [WSJ]

The city is planning to build flood-proof houses. Thirteen properties destroyed by Superstorm Sandy in 2012 have been earmarked by the Department of Housing Preservation and Development to purchase for $1.67 million in federal grants. The agency then plans to construct one- and two-family homes that are elevated 6 feet to protect against flooding. [The City]

Here’s the current state of commercial lending in New York. Low interest rates, a glut of debt and rent law reforms are just some of the issues forcing lenders to offer record-low prices to secure deals in New York’s lending market. [TRD]

Compiled by David Jeans

FROM THE CITY’S RECORDS:

Financing:

The Manocherian Brothers secured a $65 million refinancing loan from the Bank of New York Mellon for 400 East 71st Street, a 23-story building in Lenox Hill. [ACRIS]

Wells Fargo provided a $60 million building leasehold mortgage to Genting New York, the casino, for a vacant parcel at 110-10 Rockaway Boulevard in Queens. [ACRIS]

AAREAL Capital Corporation provided a $90 million refinancing loan for 101 Fifth Avenue. [ACRIS]

Compiled by Mary Diduch