Arlene Reed is still reeling from a deal that took months to go into contract.

Arlene Reed is still reeling from a deal that took months to go into contract.

By the end of February, the Warburg Realty broker was helping guide a buyer through an accepted offer on a $3.9 million apartment in a new construction condo project on the Upper East Side. But before the parties inked the contract, New York woke up to the threat of coronavirus.

The stock market had taken a nosedive, businesses were shuttering left and right, and her buyer wanted a bargain.

“Generally, a seller would say, ‘get lost,’” Reed noted. “No one’s waiting two months for you.”

But these aren’t ordinary times. Instead, she wrangled a $100,000 credit for a renovation and a financing contingency that allowed the buyer to walk away unscathed if its lender didn’t fund the deal, and the sponsor agreed to pay the mansion tax. (They had also already agreed to pay common charges for a few years.)

Selling a high-end home in Manhattan can be trying even in the best of times, especially in a soft market with a glut of new development condos. Going into 2020, there was $5.7 billion in existing condo inventory on the market and another $33 billion worth of inventory in the shadows, according to a report by Halstead Development Marketing. Add a pandemic to the mix and you might as well give up trying — and that’s what some top brokers have done, decamping to second homes to wait out the disease from the comfort of the suburbs.

For those still trying to do deals, Covid-19 has not only upended the entire market, but also fundamentally changed the way they do business. While brokers were once traversing the city, going from one showing to the next, they’re now holding daily meetings over Zoom, navigating virtual tours and strategizing ways to stay competitive in a recession.

“I never thought that I’d be doing virtual tours from my childhood bedroom in Massachusetts,” Halstead Development Marketing agent Craig Dancewicz joked before showing off a 46-unit condo he’s handling in Astoria, Queens. The building, dubbed the Rowan, launched sales just six weeks before the pandemic shuttered its sales office.

And for luxury developers, the pandemic has only intensified the challenge of moving unsold inventory in a soft market — even more of a challenge now that buyers can’t see their potential homes in person.

At the end of April, Extell Development announced that it was offering discounts of up to 20 percent on all remaining units at its 815-unit One Manhattan Square condo in response to the pandemic — the first major developer to publicize such a move.

“While we have adapted to selling our residences through a virtual sales experience, we recognize that it is also important to incentivize our buyers with this program,” Gary Barnett, Extell’s founder and chair, said in a statement provided to The Real Deal.

Others are offering unheard-of contingencies that allow buyers to get back their deposits if the deal should hit a snag.

Others are offering unheard-of contingencies that allow buyers to get back their deposits if the deal should hit a snag.

At the 46-unit Astoria condo, developer RockFarmer Properties is offering buyers who sign a contract during the shutdown the ability to walk away from the deal with a full refund of their deposit after they see the unit. Buyers will have a five-day window whenever the sales gallery reopens to come in person.

“It’s a no-lose situation,” said John Petras, a co-founder and managing principal of RockFarmer. His company is also offering a scaled 10 percent deposit at the Rowan, with 5 percent due upon contract signing and the rest due on Oct. 1.

The great pause

When it comes to who’s actually buying in the city’s sales market, the answer is murky.

Some are even questioning the veracity of data, particularly after listing portals removed their “days on market” calculation at the urging of trade organizations advocating on behalf of real estate agents.

One metric nearly everyone can agree on — in addition to the market being down — is that the number of properties up for sale has fallen as a result of the pandemic.

Even as early as March, when awareness of the coronavirus remained low, the volume of new home listings was notably less than a year earlier, according to an analysis by Jonathan Miller of appraisal firm Miller Samuel. The number of condos and co-ops listed in Manhattan in March typically grows by about 7 percent compared to the end of February, heralding the start of spring selling season.

This year, however, listings grew by only 2.2 percent in the first nine days of the month, Miller found.

By the end of the month, spooked sellers had pulled hundreds of homes off the market, according to data firm UrbanDigs.

Douglas Elliman Chair Howard Lorber said his 7,000 agents are discouraging clients from listing homes now, while they’re unable to show the properties in person. “We don’t think it really makes sense [to list],” Lorber said on an earnings call for Elliman’s parent company, Vector Group, in early May.

When it comes to closed sales, Lorber said Elliman saw a “severe decline” in mid-March, as Gov. Andrew Cuomo’s ban on home showings went into effect, though it was later amended to allow virtual showings.

In response, Elliman and many other brokerage firms made hefty cuts in payroll costs and salaries in anticipation of plunging sales volume.

The Corcoran Group’s parent, Realogy, reported a 30 percent drop in New York City deals, while contract activity fell by 50 percent at its company-owned brokerages.

The Corcoran Group’s parent, Realogy, reported a 30 percent drop in New York City deals, while contract activity fell by 50 percent at its company-owned brokerages.

Though some brokers claim there are still buyers ready to lay down their money sight unseen, such deals are rare, and the majority that do close or go into contract began in earnest weeks, if not months, before lockdown.

Wendy Maitland, founder of the boutique brokerage Atelier WM, brokered one of only a handful of luxury contracts signed in Manhattan at the end of April.

The seller had initially accepted an offer in late February, but the buyer pulled out after the stock market plunged, she recounted in Olshan Realty’s luxury market report. A second buyer also backed out. Running out of options, Maitland later went back to the first buyer, this time offering a fresh round of concessions, and managed to cut a deal.

Such stories are rare: In the seven weeks after New York’s stay-home order came into effect, just 20 luxury contracts were signed, according to the latest market report, a stunning fall from the 158 during the same period last year.

An UrbanDigs analysis of property records and the Real Estate Board of New York’s Residential Listing Service shows the number of closed deals between March 23 and the end of April in Manhattan was down 71 percent year-over-year. Signed contracts dropped 76 percent.

The preliminary analysis of weekly reports by Olshan and UrbanDigs is only part of the picture, however.

Parsing what transactions are true products of the age of coronavirus (viewed, negotiated and closed amid the pandemic) is nearly impossible. It’s also debatable whether data recorded during the lockdown in New York City’s property records and industry databases is truly accurate.

“Even if there is a data point, nine times out of 10, its genesis was pre-Covid,” said Miller.

“On top of it, we’re expecting unusual delays in the difference between the closing date and the reporting date, just because government employees are working from home, too,” he added. “So there’s all these hurdles to get over to get current, fresh, of-the-moment information.”

Reality checks

While it may take another month to get a clearer sense of April sales, existing contract data offers valuable insight into what it takes to keep deals alive in a pandemic — often grueling tests of resilience and perseverance.

Donna Olshan, who writes her firm’s weekly report about luxury contract signings in Manhattan, said that after the city went into lockdown, she was forced to throw out her numbers-driven formula because new contracts were in such short supply.

Instead, Olshan said, she’s taken to hitting the phones each week to get the backstories from brokers about their deals. Many describe multimillion-dollar contracts hanging on by a thread — buyers nervous about the market, demanding price cuts, and round after round of renegotiations.

Beyond the here and now is the urgent question of when everyone can go back to work. While some firms are making tentative plans, the uncertain timeline makes it more difficult to prepare for life after the most severe restrictions are lifted.

The city’s shutdown is slated to end in June, but it remains to be seen if the governor will extend it, and no one knows what a return to normalcy will look like, given new concerns about social distancing, sanitizing and density in office buildings.

There are also questions about how buying patterns will change and whether our collective concern about density will spell doom for Manhattan’s crowded condo buildings.

At HFZ Capital’s XI condo, the Douglas Elliman sales team had discussed the possibility of a bulk offering — a trend gaining traction in the pandemic as developers and investors hunt for opportunity.

For these kinds of deals to materialize, though, developers will likely have to entertain deep discounts.

“I have a list of people that want to buy in bulk, it’s just that I’m not seeing anybody that really is interested in selling in bulk at a price that investors would be interested in,” said Andrew Gerringer, who runs new business development at the Marketing Directors.

Art Hooper, president of development firm Ceruzzi Properties, said he was open to bulk opportunities at his Upper East Side condo, the Hayworth. “There are bulk buyers out there,” he said.” They’re in the market; they’re calling all the condo owners, not just us.”

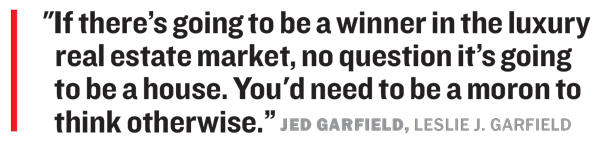

In the townhouse market, some brokers are feeling confident that the pandemic will give their product the edge over condos.

“If there’s going to be a winner in the luxury real estate market, no question it’s going to be a house,” said Jed Garfield, a townhouse specialist with Leslie J. Garfield.

“You’d need to be a moron to think otherwise.”

Time for some action

It’s hard to find a group more optimistic than New York City brokers.

Celebrity broker Ryan Serhant of Nest Seekers International said that after an initial slump, he saw his business begin to pick up again one month into lockdown.

“For the first four weeks of quarantine, the market was very quiet … Everybody was in a wait-and-see mode,” he said. “[Now] we’re going into this strange new normal.”

New listings in Manhattan began to creep online at the end of April, including pop singer The Weeknd’s former Tribeca rental that appeared on the market asking $27.5 million in early May.

(Listings and contract signings, however, remained down.)

There have also been some preliminary signs that New York state’s housing market could be spluttering back to life.

In the first two weeks of May, the number of mortgage applications to buy homes in New York increased by 9 and 14 percent from the previous weeks, despite the number of applications still lagging a significant 51 and 43 percent, respectively, compared to the same periods a year earlier, the Mortgage Bankers Association reported.

And while it remains an open question if and when buyers may be comfortable touring apartments again, most believe that New York’s buyer’s market will continue unabated for the foreseeable future.

“I’m sure developers are scared to death,” said Reed of Warburg. “[But] when you’re working with your buyers? Run. Run, go get something.”

“If you’re working with buyers,” she added. “this is your moment.”