Home-flippers are busier than ever. They had better be, because their profit margins have been plunging for three years.

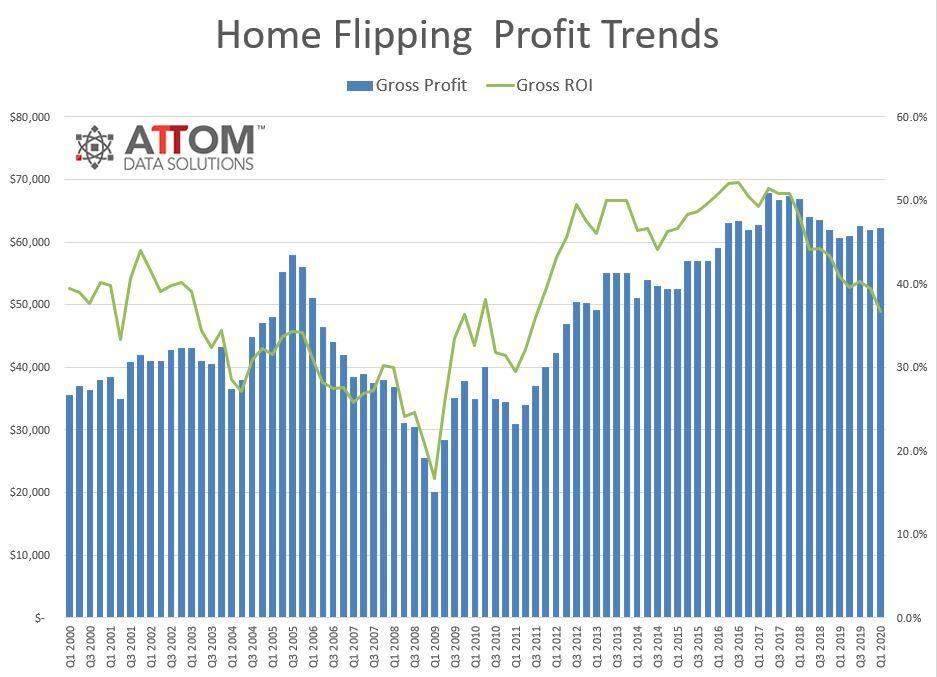

The first quarter of the year saw home-flipping activity keep rising but return on investment continue a three-year slide to fall to its lowest level since 2011, according to a report from real estate data provider Attom Data Solutions.

Attom found that 53,705 single-family homes and condominiums in the United States were flipped in the first quarter, accounting for about 7.5 percent of all home sales. That was the highest level since the second quarter of 2006.

Yet as home prices rose, increasing acquisition costs, flippers’ returns dropped back to where they were soon after the Great Recession.

The median gross profit on a home-flip increased to $63,200 from $62,000 the previous quarter, but that was just 36.7 percent of the median purchase price, down from 39.5 percent in the fourth quarter of 2019 and 40.9 percent a year earlier.

“Home flipping has gradually taken up a larger portion of the housing market over the last couple of years,” said Attom’s chief product officer Todd Teta in a statement. “But profits are down and are lower than they’ve been since the dark days following the Great Recession, which is a sign that investors aren’t keeping up with price increases in the broader market.”

Perhaps offsetting the narrowing of margins, flippers are financing their purchases less often. The report found that the share of investors taking out loans to flip homes dropped to 40.5 percent from 44 percent in the last quarter of 2019 and from 46.4 percent last year.

The trend in all-cash deals for investment properties might continue as major mortgage providers tighten lending standards in response to the market shocks of the coronavirus pandemic.

Tight credit also probably led more buyers of flipped homes to seek cheap credit backed by the Federal Housing Administration, which insures low-interest, low-down-payment mortgages. More than 15 percent of homes purchased in the quarter used loans backed by the agency, up from 14.6 percent in the fourth quarter and 13.5 percent in the first quarter of 2019.

Teta added that the coming months will be important for the home-flipping market. If home prices fall, flippers will get hit hard. So far, homeowners are in a better financial position than they were before the last recession and can ride out the pandemic without dropping prices and moving en masse.

Source: Attom Data Solutions