Just before Manhattan rents started soaring at the start of the year, Blackstone Group agreed to buy a Frank Gehry-designed apartment tower in the Financial District for $930 million.

Across the East River, KKR has spent more than $1 billion in the past two years to become one of the biggest owners of newer tax-exempt apartment buildings in Brooklyn. And Carlyle Group has quietly amassed a portfolio of small, mom-and-pop-style buildings in the borough worth at least half a billion dollars. Meanwhile, Apollo Global Management, an active commercial lender, is starting to take a more direct role in projects.

Private equity, historically focused on leveraged buyouts, has in recent years branched into everything from fast fashion to life sciences, taking on a role akin to, as the New York Times put it, “supermarkets of the financial industry.”

As private equity firms evolve, their appetite for big-ticket prime real estate plays has grown, and they’ve emerged as one of the biggest forces in the city’s post-pandemic recovery as multifamily investment reaches levels not seen since seven years ago, at the peak of the last cycle.

Though all are big names on Wall Street, each appears to have its own idiosyncratic strategies, largely avoiding going after the same types of properties as the others.

“One size does not fit all,” said MSCI Real Estate’s Jim Costello.

Private equity’s hunger for New York apartments is not new. Blackstone has owned the 11,000-unit Stuyvesant Town complex on Manhattan’s East Side since 2015 — when it partnered with Ivanhoé Cambridge to buy it for $5.45 billion — and acquired the Parker Towers complex in Queens for $500 million in 2018. Before its Brooklyn shopping spree, Carlyle already owned the rental tower 1 QPS in Long Island City and the 43-story Ritz Plaza north of Times Square.

KKR, which has spent the past decade building up its real estate business, is relatively new to the New York City market, and a wave of private equity-backed real estate investment trusts represents another emerging pool of money.

Today’s big multifamily buys, however, look different from the high-juice deals of yesterday. Instead of buying older properties with heavy rent-stabilized components and banking on the fix-and-flip model, private equity appears focused on free-market buildings with cash flow.

Free-market frenzy

KKR’s Henry Kravis (Getty images)

Blackstone’s purchase of the roughly 900-unit Gehry tower at 8 Spruce Street is the city’s biggest multifamily deal so far this year, and it helped push the market close to a record high.

Manhattan multifamily sales totaled $4.4 billion in the first half of the year, according to Ariel Property Advisors. The last time it hit that mark was in the second half of 2015 — the peak of the post-Great Recession recovery.

It’s no surprise that rentals are so hot. Post-pandemic demand has led to bidding wars, social media posts of apartment hunters lined up around the block to view units and renters willing to cut side checks to secure a lease. Manhattan rents have broken records each month since February, with the median net effective rent reaching an all-time high of $4,100 in July, according to a report from Douglas Elliman.

From an investor perspective, multfamily properties are also attractive as an inflation hedge .

Free-market multifamily assets accounted for 75 percent of total sales in the first half of the year, according to Ariel’s figures.

That’s largely the result of the state’s 2019 Housing Stability and Tenant Protection Act, which severely limited landlords’ ability to raise rents on regulated apartments.

The act “changed that business plan,” said Ariel’s president, Shimon Shkury. “The value-add optionality is not relevant anymore.”

Private equity played a role in bringing about that shift.

In the years leading up to the overhaul, the firms had become villainized by tenant advocates and politicians as “predatory equity,” blamed for backing landlords who sought to make money by harassing people out of their rent-stabilized homes, then upgrading the units so they could raise the rent.

Fairly or not, New York investors like Joel Wiener’s Pinnacle Group became shorthand for profit-driven, eviction-happy landlords in the early aughts, drawing scrutiny from the City Council, the Manhattan district attorney and the state attorney general.

But although private equity is now targeting free-market properties, that doesn’t mean it’s avoiding the contentious politics of housing. One need only look at institutional investors’ aggressive push into single-family rentals — the subject of a June hearing by the U.S. House of Representatives’ Financial Services Committee — to see how their presence in the housing market can stir up controversy.

Carlyle came under fire this year when one of the companies it partnered with to buy Brooklyn walk-ups, Greg Fournier’s Greenbrook Partners, refused to renew leases for free-market renters during the pandemic.

Tenants pushed back and got local leaders, including state Sen. Jabari Brisport, to condemn the move.

City Comptroller Brad Lander, who helped organize tenants at other Greenbrook buildings as a City Council member last year, said he hasn’t heard of any new complaints about tenants being forced out of Carlyle-owned buildings. But he expressed his distrust of private-equity investors, which “focus on short-term profit-making at the expense of long-term tenants … accelerating the crisis of housing affordability and stability across our city” and repeated his support for “good cause eviction” legislation, which would expand tenant protections and limit rent increases, including for nonstabilized units.

Rise of the REITs

One factor driving demand for cash-flowing apartments is the rise of private-equity REITs. Blackstone, KKR and Apollo have their own nontraded REITs, which allow individual investors to buy into large portfolios.

Blackstone recently raised $24 billion for its latest real estate fund — its largest ever, focused on opportunistic investments — but when the company bought 8 Spruce Street, it put the building into Blackstone Real Estate Income Trust (BREIT). Since its launch in 2017, BREIT has built a portfolio of mostly multifamily and industrial properties valued at nearly $120 billion.

“These are income-generating, stabilized properties, but over a longer period of time we still think there’s additional opportunities to improve and invest in these communities,” said Jacob Werner, Blackstone’s co-head of acquisitions for the Americas.

Similarly, KKR has been putting recent New York City investments into KKR Real Estate Select Trust (KREST), which it launched last year.

The REIT’s assets include the 365-unit tower at 80 DeKalb Avenue in Downtown Brooklyn, which it bought in July for $190 million. It also owns a piece of the $675 million mortgage secured by Josh Gotlib’s Black Spruce Management in March for its $837 million purchase of the 760-unit American Copper Buildings in Murray Hill.

Carlyle’s David Rubenstein (Getty images)

“Those deals are about accessing high-quality properties that we wanted to own long-term,” said Danny Rudin, who heads up investments in the Northeast for KKR. “We like the dependable cash flow in submarkets with strong fundamentals.”

Hopping on the bandwagon, Apollo filed paperwork in April to form its Apollo Realty Income Solutions REIT.

On the company’s May earnings call, Apollo Co-President Scott Kleinman said the REIT is one product “across the risk-reward spectrum that is purposely designed for this market.”

Apollo is also developing a 51-story apartment tower in Downtown Brooklyn through its mortgage REIT, Apollo Commercial Real Estate Finance.

The REIT had provided a loan on the development site at 565 Fulton Street to RedSky Management’s Benjamin Bernstein and Benjamin Stokes, a pair of brash young developers who imploded in 2019.

When RedSky went under, Apollo took over the site and tapped Steve Witkoff to develop a 561-unit building known as the Brook. Apollo and Witkoff received a $388 million construction loan from Bank of America in August.

Stuart Rothstein, president of Apollo Commercial Real Estate Finance (also known as ARI), said on the REIT’s October earnings call that there is some risk with taking on the development project, but he likes the company’s chances of recovering its investment on the loan.

“I think there is — given the strength of Brooklyn, given the strength of the New York multifamily market recently — I think there is potential for real upside to ARI economically if we execute correctly,” he said, noting that the project will take two to three years to construct and lease up.

Supply crunch

New York’s rental market is only going to get tighter.

The city needs to build 560,000 housing units by 2030 to keep up with expected population and job growth, according to figures from the Real Estate Board of New York.

As an unintended consequence of the 2019 rent law, city landlords have warehoused some 20,000 vacant but uninhabitable units, claiming that fixing them up and renting them out would be a money-losing proposition. And the June expiration of 421a, a popular property tax break for multifamily developers, is expected to drastically slow the delivery of new units for the foreseeable future.

New York is also, relatively speaking, a bargain for investors.

Cap rates for New York multifamily properties are now 5.2 percent, much higher than the national average of 3 percent for the best locations, which essentially means other markets have become overheated and New York has become a less expensive alternative.

Investors who pulled money out of the city in recent years in favor of high-growth areas like the Sun Belt are now moving in reverse: selling out of secondary markets and buying in the Big Apple.

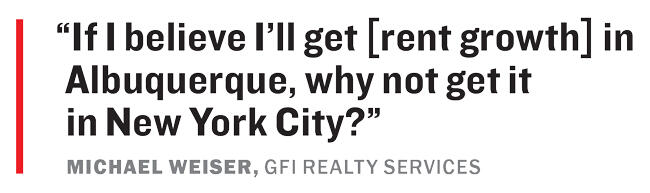

“Every landlord’s seeing that,” said GFI Realty Services President Michael Weiser. “If I believe I’ll get [rent growth] in Albuquerque, why not get it in New York City?”

The last time the multifamily market was this hot was in 2015, when Stuyvesant Town sold for more than $5 billion.

The buyer leading the market back then was, of course, Blackstone.