During a recent earnings call, Starwood Property Trust CEO Barry Sternlicht broached a touchy topic in the real estate world: the possibility of a recession.

The head of the $56 billion real estate investment trust told investors and analysts that “the only thing we have to worry about is a calamitous recession,” warning of a slowing economy largely thanks to the national political environment.

Specifically, Sternlicht said Starwood needs to be “über-careful” in the hotel sector because of a potential oversupply.

Developers have, in fact, been churning out hotels at a blistering pace. And New York is one of several U.S. cities (along with Miami) that have seen a boom in hotel construction.

As of May, there were more than 18,700 hotel rooms across 112 new developments under construction or being planned in the five boroughs, according to NYC & Company, the city’s tourism arm. That includes a 128-key Hotel Indigo in the Financial District and a 137-key Six Senses resort and spa at HFZ Capital Group’s “the XI” development in Chelsea.

Meanwhile, Marriott and hotelier Ian Schrager opened their roughly 450-room Edition hotel in Times Square this year, and just last month the same chain opened a 285-room Moxy in the East Village.

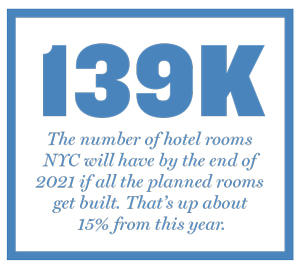

Those properties are just a few of the newbies. If all of the planned rooms are built, there will be nearly 139,000 rooms citywide by the end of 2021 — a 15.5 increase over the middle of this year, NYC & Company’s data shows.

A second-quarter report from the financial firm PwC painted a less-than-rosy picture for the Manhattan hotel market.

A second-quarter report from the financial firm PwC painted a less-than-rosy picture for the Manhattan hotel market.

“Continued increases in supply, coupled with pressures on demand stemming from continued trade tensions and slowing economic growth, are having a profound impact on Manhattan hotels,” PwC’s Warren Marr said in the report. “In addition, inbound leisure travel from China was also impacted due to the devaluation of the yuan.”

Others — including Jim Butler, who chairs the global hospitality group at L.A.-based law firm Jeffer Mangels Butler & Mitchell — said pricing for properties in top U.S. markets like New York has generally peaked, making it a good time to sell.

“It’s still a good market and they’re getting good prices,” he said, noting that there is good reason to invest in “irreplaceable locations and buildings.”

But, he said: “It’s great to diversify risks and good to be taking chips off the table.”

How many chips to take off the table is the big question.

The hospitality industry has historically been a canary in the coal mine — one of the first segments in real estate to get hit when the market starts turning. That’s because it’s low-hanging fruit for both consumers and businesses to cut back on hotel stays.

In the wake of the 2008 financial crisis, the key metric for gauging hotel performance — revenue per available room, or RevPAR — plummeted nationally. And New York was hit harder than most, with RevPAR free-falling by 27 percent between October 2008 and 2009.

There are already red flags this time around.

In August, hotel research firm STR downgraded its projected 2020 RevPAR growth nationally to 1.1 percent from the 1.9 percent it had projected in June. And New York is the only major market in the country where STR projects a decline in RevPAR — albeit of just 0.8 percent — in 2020. Year-to-date RevPAR was down 3.6 percent in the city from the same period last year.

While economists have been chattering about a downturn for a while, all signs now suggest that it’s imminent. Most economists expect the recession to really hit in 2020, which is expected to be a particularly hard year for the hotel industry.

HFZ’s XI, which will include a Six Senses resort and spa

The Federal Reserve Bank of New York’s recession probability indicator — which gauges the likelihood of a recession within the coming 12 months — skyrocketed from around 10 percent at the beginning of 2019 to 37.9 percent in August.

Oversupply is a key concern for hotel owners in a recession, said attorney Joshua Bernstein, co-chair of the hospitality sector team at the law firm Akerman. Established hotels and brands are better positioned to weather a downturn, he said.

“New supply is generally a greater risk for [owners of less-established properties] because they have no existing reputation in the market and no cash flow to rely on, so they’re at risk of some large debt liabilities,” he said.

Exposure and opportunities

In New York, smaller boutique hotels, particularly those in the outer boroughs, are more vulnerable to a downturn than their larger Manhattan counterparts, sources say.

Boutique hotel development has exploded since the last recession, with nearly 40 percent of hotels planned since 2013 including fewer than 70 rooms, according to a July TRD analysis.

Smaller developers often build boutique hotels outside of the city’s core. But those properties are at risk in a down market, said Douglas Hercher, principal and managing partners of hospitality investment banking firm RobertDouglas.

“In a recession, the market pulls back into Manhattan,” said Hercher. “Those assets that aren’t as conveniently located can suffer — Secaucus, Brooklyn, Harlem.”

In New York, developers and lenders have yet to show much concern about a potential turn in the market.

In March, Bank Leumi USA issued a $45 million construction loan for Maddd Equities and Joy Construction’s 203-room project on West 48th Street in Hell’s Kitchen. That same month, Lightstone Group refinanced its recently opened 349-key Moxy Chelsea with a $155 million loan from LoanCore Capital and KSL Capital Partners.

Goldman Sachs is also betting on the sector. It refinanced the debt on at least two hotels this year — $115 million for the Sapir Organization’s 264-room NoMo and $88 million for CBSK Ironstate’s 249-key Pod Hotel in Brooklyn.

While CMBS hotel debt is still available in major markets, including New York, it’s not coming as easily as it is for office properties and other assets, said Manus Clancy, a senior managing director at Trepp, which tracks securitized mortgages. Overbuilding — and a handful of delinquent loans — have led to closer scrutiny from lenders.

“People want to see stronger financials, less leverage, a longer track record [from borrowers],” Clancy said. “People are cautious, but its still available.”

Still, Clancy said, many owners may be insulated this time around by long-term financing that will carry them through a recession.

To some extent, he added, the narrative of a looming recession “has got ahead of the reality.” But, he said, there’s a consensus that the unprecedented 10-year economic expansion is nearing its end.

“There’s one perspective that we’re in the eighth inning of the rally,” Clancy said. “But some people think we’re in the first inning of a recession where the first pitch really hasn’t been thrown yet.”

As of early September, 7.7 percent of the $3.9 billion CMBS loans for hospitality properties in New York were in some stage of delinquency, according to Trepp. By comparison, only around 2.6 percent of the $3.9 billion in hotel-backed CMBS loans in L.A. are in delinquency, and none of the $3.9 billion in South Florida are.

Strong tourism in New York has kept occupancy relatively high — it’s hovered above 85 percent since 2013. But for every month this year, those rates have been down over last year.

In May, the Miami-based Safe Harbor Equity launched a $100 million distressed debt fund and then doubled its target a month later after garnering strong interest during fundraising tours in Europe and Asia. Raphael Serrano, the firm’s managing director, said the fund — which will target all commercial assets, including hospitality and retail properties — is focusing on South Florida but will also look to other major markets, including New York, Texas and California.

The Edition in Times Square

Safe Harbor’s goal is “to be well-positioned for the oncoming economic headwinds that are being forecasted,” Serrano said in May.

A recession may not even be the most worrying challenge ahead for hotel builders in New York.

Construction and labor costs are already contributing to struggles for developers in the Big Apple, Miami, California and elsewhere.

In New York, rising costs are baked in balance sheets for the next seven years. That’s because in 2015, the Hotel Association of New York City — which represents hotel owners — extended a 2012 deal to increase wages for bar and restaurant workers through 2026.

HANYC President and CEO Vijay Dandapani said that while labor costs are a concern, an even bigger issue in New York is property taxes.

“Real property taxes are a real bite,” Dandapani said. “On a macro level, we’ve been working on this for years with the Department of Finance.”

High costs become that much more problematic when RevPAR takes a hit.

“I think the scariest thing is that costs right now are for the first time in years going up faster than RevPAR, particularly for labor,” said Butler, speaking about the national landscape but also noting that it’s a concern in New York.

He said it’s crucial for hotel investors to be capitalized going into a downturn. “The best thing you can do to prepare for a downturn is make sure you have ample equity and funding,” Butler said. “The hotel industry is cyclical — they’re going to be back, but if you can’t get through the downturn, you could lose your property.”

He noted that when consumer and corporate clients start to cut back on expenses, the luxury hotel industry tends to cut room rates. That, he said, creates a “suicidal” downward spiral. Hotel owners would be wise to hold steady on pricing in the event of a slowdown, he said.

Larry Wolfe — vice chairman and co-head of the Lodging Capital Markets group at Newmark Knight Frank — also noted that owners usually cut their room rates if occupancy dips.

“In New York there seems to be infinite demand for cheap rooms, so occupancy stays up but rates don’t hold and [owners] tend to cave,” Wolfe said. “So if declines in the bottom line accelerate, inevitably there will be more situations that become somewhat distressed.”

Black swans

The hotel market has been underperforming for a while now.

In 2017 and 2018, national RevPAR growth was the weakest it’s been since the recession — at around 2.9 percent annually, according to STR.

RobertDouglas’ Hercher cautioned that the recent declines in fundamentals are more a function of “oversupply” and “post-peak pricing” than a recession.

“What we haven’t seen in a way that I would be willing to say demonstrates — or is evidence of — a recession,” said Hercher, who represented KHP Capital Partners in its $67.6 million sale of the 205-key hotel at 70 Park Avenue in 2016. “Declines in [room rates] and occupancy that appear to be a function of a drop in demand instead of new supply or unwillingness to pay a higher [rate].”

The prevailing view seems to be that when the next recession hits, it will be less severe than the last one. But Butler noted that there are always unknowns.

“I am not pessimistic, I am optimistic,” he said. “But over the years, I’ve been through some cycles where there is an event that isn’t quite as big as a black swan, and we never see it no matter how hard we look. We never see it.”