Updated May Property owners seem to be willing to get a bit unconventional these days to keep rent payments rolling in amid the ongoing waves of store closures.

Indoor amusement parks, doctors’ offices, movie theaters, gyms and even discount stores — once considered undesirably downmarket — are plugging holes in vacancy-riddled shopping centers and storefronts as rents decline, leases shorten and concessions spike, brokers and owners say.

The Real Deal’s ranking of the top leasing deals and brokerages in major markets in the U.S. reveals that, despite efforts by national firms to boost their retail teams in recent years, the marketing of stores is still largely a local game outside of Los Angeles and New York City. “We’re all trying to do the best we can,” said Marty Shelton, an L.A.-based broker with NAI Capital, the second most active retail leasing brokerage in L.A. County, with 718,825 square feet rented over the past 12 months, according to TRD’s analysis.

To rank the top brokerages in leasing for Chicago, Miami, L.A. and New York, TRD examined data provided by commercial real estate services firm Lee & Associates NYC on new retail leases and renewals in those markets from April 2017 to March 2018. Brokerage leasing totals and deals were shared with the firms, which were given the option to submit additional information.

Josh Strauss

New York

The country’s most populous city, which is also a major draw for tourists on shopping sprees, has not been insulated from the retail collapse. Once-vibrant shopping districts in Manhattan — like Fifth Avenue, Madison Avenue, Soho and Bleecker Street — continue to be pocked with empty storefronts.

As in other U.S. markets, the list of top New York leases over the past year includes many tenants in the business of offering “experiences,” a heavy-in-rotation retail buzzword.

To wit: The largest deal of the last 12 months was Equinox Fitness’ renewal of its nearly 66,000-square-foot, two-level space at Midtown’s One Park Avenue, a 22-story, full-block office building at East 32nd Street majority-owned by Vornado Realty Trust. The deal, which was handled in-house by Vornado, closed last spring.

Similarly, Chelsea Piers, the vast Manhattan sports complex, leased a 52,000-square-foot, two-level space at 33 Bond Street, a new 25-story rental in Brooklyn from developer TF Cornerstone. A 25-yard pool, yoga studios and a cafe will be included the property, which earned a fourth-place finish. In the transaction, the landlord was represented by Winick Realty Group, the fourth most active retail brokerage in New York, with 547,000 square feet under its belt.

Even though New York sees tens of millions of visitors a year, retail in tourism-rich districts like Times Square — including restaurant concepts that are performing well in other markets — has also struggled, brokers say.

(Click to enlarge)

At 11 Times Square, an office tower developed by SJP Properties on West 42nd Street, two high-profile restaurants collapsed after about only a year: an offering from Señor Frog’s, a national restaurant chain; and Urbo, a farm-to-table eatery.

“Times Square is actually under-restaurant-ed,” said Joshua Strauss, an executive vice president with RKF, which markets the tower. “But if you don’t have an offering that’s compelling, no one is going to come.”

Now 11 Times Square will serve up a 48,000-square-foot, three-level virtual-reality-themed indoor amusement park from the film studio Lionsgate. The first of many planned across the country, the attraction will draw on movies and TV shows like “The Hunger Games” and “Mad Men.”

The asking rent on the 20-year lease, which includes options to renew, was $8 million a year, “and we got close to it,” Strauss said.

SJP is offering an unspecified amount of free rent while Lionsgate and its operator, Parques Reunidos Group, extensively renovate the location, which will open in 2019. “Experience is driving retail,” Strauss added. “It’s not just a fad. It’s the wave of the future.”

In terms of the present, RKF is New York’s busiest retail brokerage, with more than 1 million square feet leased in the last 12 months, according to TRD’s analysis of data, which was provided by Henry Abramov from Lee & Associates NYC. RKF seems to be that rare national firm with regional dominance, even though the 20-year-old company’s roots are in Manhattan.

Other national players with similar clout in New York include Cushman & Wakefield (No. 5 with 523,000 square feet) and Newmark Knight Frank (No. 6 with 431,000 square feet).

But local firms have also finished strong, like Winick, as well as Ripco Real Estate (No. 2 with about 872,700 square feet).

Ripco had a hand in the city’s second-largest retail deal, the lease of about 57,000 square feet in the Hub section of the Bronx by Burlington Coat Factory, now known as just Burlington after an early-2017 rebranding. Located in a bustling shopping district, the store is owned by A&H Acquisitions, a retail-focused developer helmed by longtime retail investor Alex Adjmi. Ripco repped A&H; CNS Real Estate was the agent for Burlington.

“It’s in a terrific transportation hub, close to the subway and buses,” Cliff Simon of CNS told TRD last summer about the deal. “It’s an old historic shopping street with great density.”

Burlington, a rapidly expanding discount apparel chain with about 640 stores in 45 states, also took 55,000 square feet in Kings Plaza Shopping Center, a mall in Mill Basin, Brooklyn, owned by Macerich. Other tenants at the mall, which opened in 1970, include Old Navy and H&M. The Brooklyn Burlington lease, which is for 10 years and has three options for extensions, was the third-biggest transaction last year.

Los Angeles

Los Angeles

L.A. County is tightly focused on making sure the bottom doesn’t fall out of the retail leasing market.

To accomplish this, the sprawling metropolis is thinking small. Tenants continue to experiment with pop-up stores, flocking to small spaces of less than 10,000 square feet that come with leases of just a few months. These short-term deals are trending at the same time that there’s an increase in calls to brokers from tenants asking how they might lower their rents, though those efforts are usually unsuccessful, brokers said.

Large-scale retailers are also shrinking footprints to appeal to the tastes of millennials — who reportedly dislike cavernous stores — and to save on real estate costs, which are of particular concern in booming L.A.

As large retailers see upticks in their e-tailing businesses, vast brick-and-mortar locations are less important anyway, said Shelton of NAI Capital, citing the example of Target, which usually occupies 150,000-square-foot stores and as of press time was still looking for a 22,000-square-foot berth in the Hollywood neighborhood.

As large retailers see upticks in their e-tailing businesses, vast brick-and-mortar locations are less important anyway, said Shelton of NAI Capital, citing the example of Target, which usually occupies 150,000-square-foot stores and as of press time was still looking for a 22,000-square-foot berth in the Hollywood neighborhood.

Similarly, Kohl’s, a department store chain, closed several locations across L.A. in the last two years, in part, according to news reports, to save on expensive leases.

One of Kohl’s closed locations in San Gabriel will welcome what appears to be the first California outpost of the British grocery chain Asda in what was the fourth-largest lease in the county over the last 12 months. Asda entered into an 80,000-square-foot sublease deal brokered by Colliers International, the fourth most active L.A. County retail leasing brokerage, according to TRD’s ranking, with nearly 345,000 square feet rented.

(Click to enlarge)

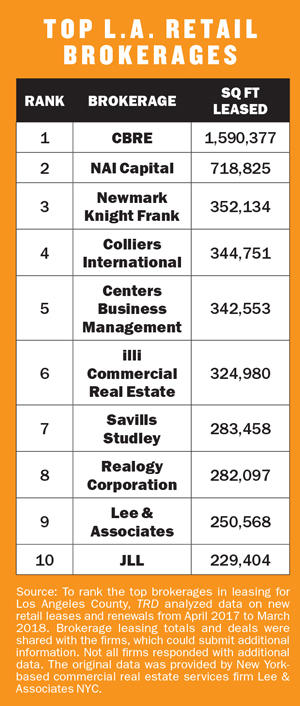

Like Colliers, CBRE — which is No. 1 in L.A. with nearly 1.6 million square feet leased — is a national firm. But West Coast agencies are also active, like NAI Capital, in second place, and Centers Business Management, which is focused on shopping centers and took fifth place with 343,000 square feet.

It’s important to note that TRD’s brokerage ranking, which does not include numbers of deals, does not tell the full story when it comes to the most active players in the market. Some local firms are not focused on hitting mega-deal home runs, which can be hard to attain in the current economy. Instead, they opt for lots of base hits to get ahead.

For example, despite not landing any huge individual leases, NAI manages to be one of the city’s most active firms through multiple small-bore deals, like a recent one with a 7-Eleven convenience store at 6500 Hollywood Boulevard, Shelton said. Fast-casual restaurants, like Burger Lounge, a chain that specializes in grass-fed meat in 1,500-to 2,500-square-foot spaces, are also a strong subsector, he added.

As is the case across the country, discount stores offering items at deep discounts — around $1, in some cases, but also with less drastic cuts — are also a growth category.

As is the case across the country, discount stores offering items at deep discounts — around $1, in some cases, but also with less drastic cuts — are also a growth category.

A recent transaction in this category involves the discount-furnishings store Curacao, which in October renewed its lease for an over-100,000-square-foot space in a shopping center at 5980 Pacific Boulevard in the Huntington Park neighborhood. That was L.A.’s largest leasing deal in the last 12 months, according to TRD’s ranking..

When Curacao’s lease was up for renewal, Argent Retail Advisors — the 10-year-old brokerage representing the landlord, Il Young Kim — began marketing the 1984 building, said Terry Bortnick, Argent’s president. He said there was widespread interest from a “who’s who” of tenants, since large footprints are hard to come by in the area. But Pacific Properties might have had to renovate the space, a costly undertaking, and so instead stuck with Curacao in a 10-year deal, Bortnick said.

The asking rent was $25 a square foot annually, which is on a par with the $27 average asking rent for shopping centers countywide, according to Cushman & Wakefield.

“Deep discounters are one of the few categories that are still aggressively opening in today’s environment,” Bortnick said.

Meanwhile, landlords are being squeezed as they look for new tenants, including discount chains, to replace closing stores.

In addition to offering free rent to commercial tenants while they renovate their stores — a fairly typical concession — owners are now expected to offer credits to help pay for things like expensive electrical work, according to brokers.

South Florida

South Florida

With low vacancy rates and a whirlwind of retail leasing, the Miami metro area continues to buck the national trend.

In fact, the average asking rent in the first quarter of 2018 was about $40 a square foot, according to Colliers International. That’s a sharp jump from the $35-per-square-foot asking rent in the year-earlier quarter.

But dark clouds may be forming, brokers said. Toys “R” Us, the bankrupt toy chain that announced in March it would close all of its U.S. stores, has 23 locations in South Florida, meaning a mass of big-box space is poised to flood the market.

(Click to enlarge)

In a similar vein, Miami is awash in new retail construction, like the mixed-use megaproject Miami Worldcenter, which has 360,000 square feet of stores being built or planned for downtown.

As is the case in other markets, a major bright spot appears to be discount retailers. These chains are often publicly traded and have deep pockets, which helps explain their appeal as tenants.

Many of the top leasing deals of the last year involved companies emphasizing below-market-rate merchandise, according to TRD’s ranking. Costco, the discount giant, took more than 51,000 square feet by the Miami airport, and Burlington was responsible for a pair of leases, one in Lake Park in Palm Beach (ranked fifth) and one in Hollywood, which was 35,178 square feet.

As in other markets, national chains are picking up some of the slack. Hobby Lobby, the arts-and-crafts store, took three major berths last year, all at 55,000 square feet — a size the brand strictly adheres to — making the chain responsible for three of the top five South Florida leases.

A variety of landlords are benefiting from the store’s moves. In Dania Beach, near Fort Lauderdale, Hobby Lobby will take space at Kimco Realty Corporation’s Dania Pointe, an under-construction one million-square-foot retail complex that is charging forward despite the gloomy forecast.

While malls are suffering as shoppers gravitate toward other experiences, Kimco, a Long Island-based developer, is betting there will be demand for its brand of shopping complex, which is more open-air than typical mall properties.

The $800 million, 102-acre Dania Pointe project, on the site of a former roller coaster, the Hurricane, includes tenants like T.J. Maxx and Outback Steakhouse among its 10 storefronts.

Hobby Lobby also picked up space in a building owned by Verde Realty, a real-estate investment trust, in Pembroke Pines. In addition, the chain will cut a ribbon in part of a former Kmart store at the Plaza at Lake Park, a shopping center owned by the Sterling Organization, a Florida-based private-equity firm.

On the tenant side, all three Hobby Lobby deals were handled by Katz & Associates, South Florida’s third most active brokerage with 326,000 square feet leased last year, according to the ranking. A 22-year-old firm that mostly represents tenants along the East Coast, Katz did not return a call for comment.

Chicago

Chicago

As the retail economy has suffered, so too have companies generally considered bullet-proof, like Wal-Mart. Earlier this year, it announced it was closing dozens of its Sam’s Club spin-offs, for instance.

But some stores – namely, chains that can offer even deeper discounts than mass-market retailers – are inching in. A location that Sam’s Club was on the verge of leasing, at the in the Deerbrook Shopping Center in Deerfield, Ill., is instead now home to the latest outpost of the Dump Luxe Furniture Outlet, an 11-location chain specializing in discounted couches and tables, with an unusual twist. It’s open only on weekends to keep labor costs low. With about 136,000 square feet, the deal was Chicago’s largest in the past 12 months, according to TRD’s data.

Arcore Real Estate Group worked on behalf of Dump Luxe. The landlord, Mid-America Real Estate Corporation, repped itself at the property, which is a handy symbol of the decimated retail sector.

Tenants such as Best Buy, Office Max and the Great Indoors, a home decor retail chain owned by the struggling Sears, have vanished in recent years. But in an effort to salvage the property, Mid-America has renovated the one-time enclosed 1970s shopping mall into open-air shopping center; that Great Indoors store became a parking lot.

(Click to enlarge)

Other major leasing activity in Cook County seems to mirror national trends. Medical facilities, eager to branch into neighborhoods as the health care industry grows, are snapping up storefronts. The Chicago Center for Sports Medicine & Orthopedic Surgery signed a lease for an 80,000-square-foot store in a shopping center anchored by a Ross Dress for Less in North Kenwood, near Lake Michigan.

Other major leasing activity in Cook County seems to mirror national trends. Medical facilities, eager to branch into neighborhoods as the health care industry grows, are snapping up storefronts. The Chicago Center for Sports Medicine & Orthopedic Surgery signed a lease for an 80,000-square-foot store in a shopping center anchored by a Ross Dress for Less in North Kenwood, near Lake Michigan.

Likewise, Advocate Health Care will take about 50,000 square feet in Wrigleyville, in a former Sports Authority store. Services offered there will include X-rays and cardiac testing, according to a press release from Next Realty, the landlord. CBRE handled the transaction. “Finding 50,000 square feet of free-standing retail space with parking in Lakeview is like finding a unicorn. It just doesn’t exist,” said Marc Blum, Next’s president.

At the same time, Chicago’s retail vacancy rate seems relatively high. Quantum Real Estate Advisors put it at nearly 7 percent in 2017.

But market segments like grocery stores, too, seem robust. Indeed, Living Fresh Market signed up for a 70,000-square-foot store in Forest Park, in a deal it brokered with an in-house team. NAI Hiffman represented landlord Living World Christian Center in the deal.

This article has been amended to describe Dump Luxe Furniture Outlet’s lease in Deerfield, Ill with landlord Mid-America. A previous version of this story described a lease for Dump Luxe with Mid-America at another location. The article has also been amended to reflect that CBRE, with 720,071 square feet of retail space leased, sits atop the ranking of commercial leasing firms in South Florida.