Cushman & Wakefield stands alone among the city’s big commercial brokerages.

Not only is the 100-year-old firm the last of its peers to go public, its Sixth Avenue headquarters makes it an outlier as well. Cushman’s main competitors — CBRE, JLL and Newmark Knight Frank — are all located several avenues over, near Grand Central Terminal.

So when Cushman sought to consolidate several offices it inherited amid a wave of mergers and acquisitions a few years ago, it looked as though the company might finally join the others in the heart of Midtown.

But the search stalled and then slipped into inertia as top decision-makers simply couldn’t agree on a course of action. It was a case, company insiders said, of too many cooks in the kitchen, and a presage of disarray within the firm. Cushman finally gave up the effort late last year when it decided to stay put and expand at 1290 Sixth Avenue for at least another seven years.

The inability to pull the trigger was certainly surprising for a company that specializes in finding office space for clients. But the ordeal is indicative of something bigger: the growing pains Cushman has been going through as it prepares for its Wall Street debut.

Now the company finds itself at a pivotal moment. Cushman and its CEO, Brett White, are banking on a successful initial public offering to pay down some of the hefty $3 billion in debt that private equity giant TPG Capital loaded onto the firm after the series of mergers.

And Newmark’s underwhelming IPO in December raises concerns about the public market’s appetite for another commercial brokerage offering.

“It’s much more about debt than anything,” said Josh Barber, a research analyst at Diamond Hill Capital Management, an Ohio-based investment adviser and JLL shareholder. “The IPO would mark a natural exit for its private equity backer, and it’s important that Cushman engage in a process to extinguish a lot of that debt.”

Meanwhile, insiders say Cushman’s top brass has been single-mindedly focused on preparing for the IPO — and the long runup has led to immense internal disorder and confusion.

Wall Street analyst Jason Weaver said executives are under the gun to make the company appear to be a lean commercial real estate machine.

“If you don’t exceed expectations out the gate in the first couple quarters, that looks bad on management,” said Weaver, who was at the Los Angeles-based financial services firm Wedbush Securities until last month.

The mega-brokerage entered a new era in June, when it finally filed its preliminary paperwork for an IPO with the Securities and Exchange Commission.

Since 2015, when Texas-based TPG acquired the firm for $2 billion and merged it with Chicago-based DTZ — following recent acquisitions at both brokerages — Cushman has been on a roller coaster of highs (bringing on the top-grossing investment sales team in the city) and lows (company infighting that’s spilled out into the public eye).

After the DTZ merger, the firm’s leadership decamped to Chicago from Midtown Manhattan, leaving many in New York feeling like they’d been cut out of the loop.

It has also laid off some support staff, according to multiple sources familiar with the situation. And more recently, top dealmakers have been leaving the firm at an accelerating — and some say alarming — rate. Bob Knakal, who held the title of chair of New York investment sales, was the latest in a string of top players to depart last month. The brokerage told this publication that it “terminated” its relationship with Knakal just days before his contract ended. And sources say that decision came after the firm’s top brass caught wind of the fact that he was plotting his exit.

Now many are questioning whether the firm will bleed even more talent once it goes public.

“Cushman is not reinvesting in its people,” said one person with knowledge of the brokerage who, like many others, spoke to The Real Deal on the condition of anonymity. “When Cushman goes public, a lot of top people who hold stock in the company will likely cash out — and that’s not conducive to growth.”

In addition, the IPO prospectus revealed that the firm has been operating at a substantial loss since the 2015 deal.

Attorney Richard Morris, a partner at law firm Herrick Feinstein who focuses on corporate finance, noted, however, that disruptions like this are not out of the norm for companies getting ready for the brutal reality of the public markets.

“Preparing for an IPO is all results-driven,” he said. “That usually means it’s time to make significant changes.”

Too many cooks

Last October, several of New York’s most iconic office towers — including the Empire State Building and One World Trade Center — were lit red in honor of Cushman’s 100-year anniversary.

But at the commercial brokerage, that celebration was mixed with anxiety over the looming IPO.

Though the company had not yet filed its prospectus at that point, its debut on Wall Street was simply a matter of time. The industry has been marching toward the kind of growth that comes with being public, and Cushman will be the last of the big New York City commercial firms to get its own stock-market ticker.

And there’s been a looming sense of uncertainty at the brokerage — which is in an SEC-mandated quiet period and declined to comment — as it gears up for its rollout, according to several people familiar with the matter.

“It’s a shitshow,” said one source close to the company.

Several brokers who spoke to TRD expressed frustration over an increasing inability to grow within the organization, as well as a lack of communication among leadership in the firm’s various offices. And they described morale inside the New York office as being at a low point.

The delays connected to Cushman’s IPO plans have not helped matters, either.

During this latest stretch, the company was said to be eyeing 2017’s third quarter for the IPO, but as the calendar rolled into 2018 there was radio silence on when — or even if — it would happen.

When Cushman’s preliminary prospectus finally hit last month, it offered a first-ever public glimpse into the brokerage’s operations, including the fact that it’s been operating at a net loss of more than $1.2 billion since the DTZ deal. And because of TPG saddling the firm with debt, Cushman has $2.6 billion coming due in 2021 and another $470 million coming due the following year, per its SEC filing.

The company is looking to raise about $1 billion in the IPO and at a valuation north of $5 billion, the Wall Street Journal reported. It would then use the proceeds from the IPO to pay down the debt, according to the prospectus.

Ross Carmel, a founding partner at the law firm Carmel, Milazzo & DiChiara, made a similar point: “That’s their liquidity event,” he said, describing TPG’s playbook for Cushman. “That’s how they get out.”

A successful offering would give Cushman the financial firepower to further compete on a global scale and acquire smaller companies worldwide — a trend that is only accelerating.

However, insiders question what shape the company will be in after the IPO — a shell of itself with low morale and a skeleton leadership team or a leaner outfit with more dry powder.

“They want to solidify their presence,” Barber said. “Going public doesn’t give Cushman a massive advantage, but it puts them on more even footing with their public peers.”

‘Preening up the doll’

In some ways, Cushman’s books have already started improving.

In its first year under TPG, Cushman posted a net loss of $473.7 million on revenues of $4.2 billion. But by last year, the company — which employs 48,000 people across 70 countries — cut that loss to $220.5 million and upped its revenues to $6.9 billion, according to its SEC filings.

And some say they expect things to continue improving.

Retail broker Joanne Podell, who was named Cushman’s top producer worldwide in 2016, said she believes the IPO will help the firm build out its infrastructure when it comes to technology and other areas.

“I hope and I believe that [we will have] the opportunity to continue to grow our platform,” Podell said during a panel hosted by TRD in May.

But it’s become increasingly clear that some of the company’s resources have been sacrificed to get to this point.

In recent months, the brokerage has laid off a number of support staffers, including some who prepare marketing and presentation materials for brokers. The firm also implemented a new policy restricting the reimbursement of travel expenses for brokers — a move that has not been good for agent morale. And sources inside the company say there are more layers of approval than ever to collect reimbursements for business expenses.

Internally, the practice of cutting staff and dressing up financial statements has been referred to as “preening up the doll,” said one Cushman broker.

“Expense reductions do suck, especially for the brokers,” said a high-level source who formerly worked at the firm. “But it’s not uncommon to primp and dress up the earnings to do something like that. The cuts are not sustainable in the long term. The thinking is, ‘Let’s be sure our finances and metrics are in line with our competitors.’”

Some market experts, however, are skeptical of too much cutting.

“A lot of housecleaning, in my opinion, doesn’t jibe with an IPO,” Barber said.

While shaving zeros off the expense ledger might make the company’s financial statement look more attractive to outside investors, it’s causing friction — and turnover — at Cushman’s Midtown office.

Late last year, Tod Lickerman stepped down as CEO of the Americas and went to a Chicago-based private equity investor. But Lickerman told TRD he thinks the company is moving in the right direction. “Cushman was built to get to and perform at this level,” he said. “Whatever the board decides to do, the company is in good shape and should continue to grow.”

Then, in March, Executive Vice Chairman Peter Hennessy was fired after lashing out at Lickerman’s replacement, Shawn Mobley, over the firm’s new expense policy.

Others have left in recent months of their own accord.

In April, office leasing veteran Gus Field, who spent 30 years at Cushman, jumped to mega-developer Tishman Speyer, where he was tapped as leasing director. And last month, Gene Spiegelman — who previously managed the company’s retail arm — defected to Ripco Real Estate, where he’ll be one of three principals.

Meanwhile, the leadership team from Massey Knakal Realty Services, which Cushman acquired in late 2014 for $100 million, is all but gone.

Power broker James Nelson decamped in January for Avison Young, where he’s now building up a 30-person team that will likely compete against Cushman in the midmarket investment sales space. And Paul Massey — who co-founded his namesake firm with Knakal — left in April to start his own firm focusing on debt and investment sales. He’s now aiming to be in as many as 10 cities.

One broker who left called it a “sin” that the firm couldn’t find a place for Massey — a highly regarded business mind and manager in the industry. Although Massey’s contract bars him from recruiting from Cushman, sources said he is already courting Cushman’s Massey Knakal alumni.

According to several sources, Knakal is actively talking to JLL, Colliers International and other brokerages and also considering either teaming up with Massey again or starting his own shop. Both Massey and Knakal declined to comment.

Some of Cushman’s remaining Massey Knakal alumni, meanwhile, are said to be waiting to see what the duo hatches before renewing their own contracts. If — or when — those brokers hightail it out of the firm, they could alter the playing field in the midmarket space, particularly in the outer boroughs.

Sources said that while the IPO restructuring and loss of additional Massey Knakal brokers could mean a reduced presence in the outer boroughs, they noted that Cushman is not likely to abandon the boroughs altogether.

Still, Shimon Shkury, president of the multifamily-centric brokerage Ariel Property Advisors, said Cushman’s IPO is good news for smaller firms like his. He said that as the industry continues to consolidate and bigger firms go public, smaller private firms that focus on the outer boroughs, or specific asset types, will have those areas to themselves.

“As a privately held company, we’re happy to see Cushman go public,” Shkury said.

The IPO shepherd

It’s not the first public rodeo for Cushman’s CEO.

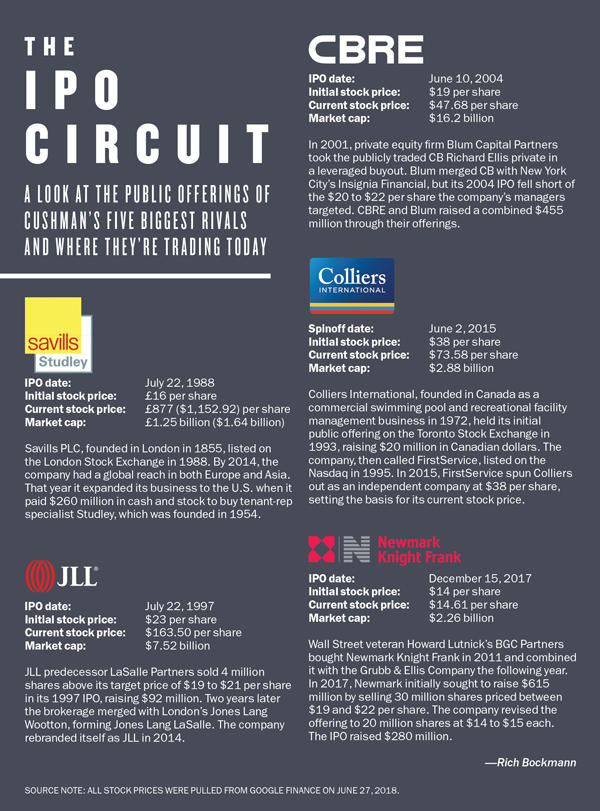

White — who joined the firm just weeks before the DTZ deal — was president of CBRE when it debuted on Wall Street back in 2004. And while there are several others who are leading the IPO charge with him, he’s the face of the company’s public debut.

And that is no accident.

“Brett White is still pretty known in the capital markets space,” Diamond Hill’s Barber said.

“A good amount of people want to hear from him, because he put the whole company together in its latest iteration,” he added, referring to the DTZ merger.

Still, sources say that the company’s board of directors weighs in on all major decisions.

And while it was contemplating its IPO, several other real estate firms have pulled the trigger, including Newmark, which went public in December.

Cushman reportedly got serious in 2017 when it held informal meetings with banks about planning an IPO. It ultimately hired Goldman Sachs, Morgan Stanley, JPMorgan Chase and UBS as underwriters.

As with its biggest rivals, Cushman’s status as a public company will open it up to more scrutiny. Not only will it be required to make quarterly financial disclosures to investors, it will also face heightened pressure to generate revenue.

And the process is not for the faint of heart.

Newmark suffered a disappointing public rollout. The New York-based firm initially planned to sell 30 million shares for $19 to $22, but instead only unloaded 20 million for $14 each. In late January, its stock price hit a high of $16.66, but as of June 27 it was trading at $14.61.

Barber said he’s “mystified” by the fact that Newmark’s stock hasn’t done well, given “thus-far solid results, a solid capital markets backdrop and strong performance by competitors.”

Despite Newmark’s less than stellar stock market debut, the IPO still gave it the capital to make acquisitions. The company announced in late May that it had reached a deal to acquire retail powerhouse RKF. And Newmark recently poached a top hotel investment sales team led by Lawrence Wolfe from Eastdil Secured.

Weaver, the analyst, said Newmark’s lukewarm IPO was the biggest deterrent for Cushman to follow suit — even though the latter firm has “a more standard ownership model than Newmark,” where top brokers own a portion of the company.

“It has to be on their minds,” he added.

The expansion mission

In many ways, the current angst at Cushman’s New York headquarters is a 180 from where the firm was during its rapid-growth days.

The company was on an expansion tear — buying firms and poaching top-tier brokers. And those moves have positioned it to make steady gains in the investment sales, office leasing and debt brokerage arenas.

After its late-2014 purchase of Massey Knakal, Cushman became a dominant force in the outer borough investment sales market — which, while not as splashy as transacting trophy Manhattan tower sales, is a high-volume sector with billions of dollars on the line.

Then, the following May, TPG announced it would acquire Cushman from the Agnellis — the Italian family that made its fortune in the auto industry — and merged it with DTZ to create the third-largest brokerage on the planet.

The Agnellis — who were also part of a group that owned Rockefeller Center in the mid-1990s — had purchased a controlling stake in Cushman in 2007.

While Cushman has always been a major player on the brokerage scene because of its size, it ramped up in a big way after the DTZ merger. The combined brokerages instantly shot up the ranks of New York City’s commercial brokerage food chain — and started luring in top dealmakers.

Two years ago, it snagged office leasing veteran Mark Weiss from Newmark, and last year it poached CBRE’s Patrick Murphy.

Then, in October 2016, it achieved the unthinkable — at least on the New York poaching front: landing the city’s top investment sales duo, Doug Harmon and Adam Spies from Eastdil. The Harmon-Spies team put Cushman in direct competition with CBRE and its institutional group headed by Darcy Stacom and Bill Shanahan.

The move paid off. The firm closed $6.36 billion in deals and landed the top spot on TRD’s latest annual investment sales ranking, which came out this year but was a tally of 2017 deals. And the firm is already on a tear this year — with the Harmon-Spies team alone closing north of $7 billion in the first half of 2018, including Jamestown’s $2.4 billion sale of the Chelsea Market building to Google, according to an analysis of property records and news reports.

Sources say Harmon and Spies signed a multiyear contract with Cushman that likely runs for five years, meaning they’re probably locked in for another three years. It’s unclear whether Cushman is offering other brokers stock options or other financial incentives to stay put.

And while the firm may have to grapple with more cuts and departures, some believe the worst is already behind it.

“They don’t want to take you public and let you fall on your face,” one source said.

Contraction action

Cushman’s belt-tightening may be the epilogue to an era of privately held big brokerages.

And whatever happens with the IPO, the exercise of preparing for it is often very useful, sources said.

“The preparation for an IPO is worthwhile even if you never pull the trigger,” Herrick Feinstein’s Morris argued. “Assessing everyone’s role and responsibility in the company drives corporate change more than anything else.”

This is not the first time Cushman has taken a cold, hard look in the mirror.

In the wake of the financial crisis, the firm (and its main rivals) all diversified their business models to protect themselves, adding or beefing up annuity-based revenue streams like property management and project development services and moving away from the pure-play brokerage model.

Weaver said 60 to 67 percent of CBRE and JLL’s revenue comes from annuity revenue — which is not subject to the whims of the marketplace. Cushman, he said, already has more than 70 percent of its revenue coming from nonbrokerage sources — nearly double the amount it had post-downturn.

“This way, they’re less cyclically exposed,” Weaver said.

Both CBRE and JLL have been rewarded on the stock market, with valuations that have surged over the past decade and are now at their highest levels since the downturn. CBRE has a market capitalization of $16.2 billion, while JLL’s stands at $7.5 billion.

“Both JLL and CBRE stocks had very strong runs this cycle, but they’re not crazily valued,” Barber said. “Both did a good job of diversifying their product lines. But if we fell into a recession, they still have a cyclical element and would probably suffer.”

What happens to Cushman’s stock remains to be seen. But considering the significant amount of debt on the firm’s balance sheet — and concerns that the country’s economic expansion is nearing a cyclical end — it appears Cushman has a narrow window to strike.

“If there was a time for Cushman to go public, it would be now,” Weaver said.