You wouldn’t be surprised to meet Jeremy Morton in the Hamptons.

Tall and ruddy, Morton rented an apartment in the West Village and owned a 12,800-square-foot home in East Hampton with an infinity pool, pool house and at-home gym on 2 acres.

He married his wife, Brooke, at a black-tie wedding at the Metropolitan Club. She would post about the couple’s lifestyle to her travel blog and Instagram account, both called the Glowtrotter, with pictures detailing their dozens of trips to places like Burning Man, Greece and St. Tropez.

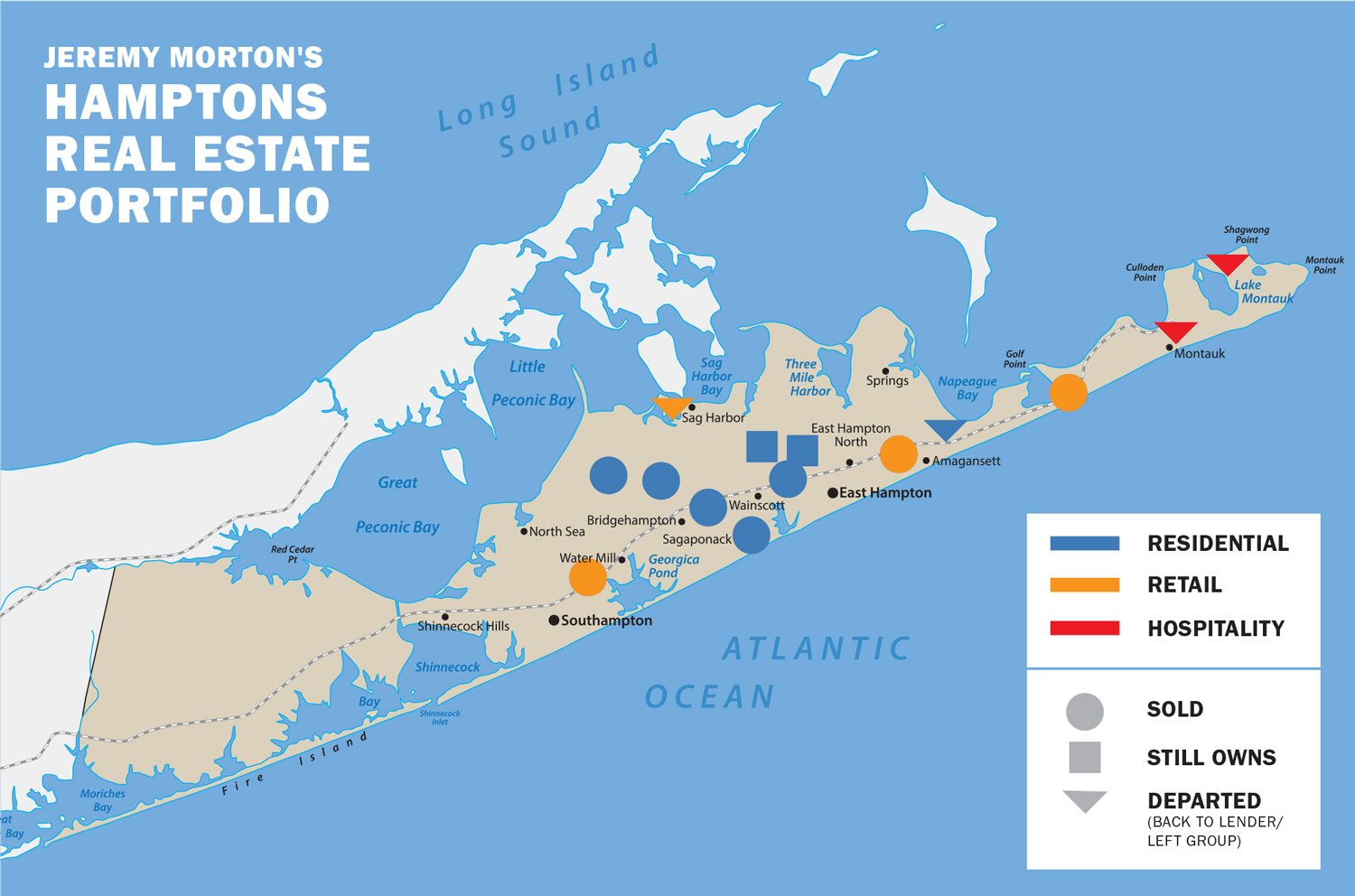

Undergirding the conspicuous consumption was a growing Hamptons real estate portfolio. The properties themselves mirrored the lifestyle: custom homes, the late-night hotspot Ruschmeyer’s, popular faux-humble eateries Cyril’s Fish House and Rick’s Crabby Cowboy Cafe, retail in Water Mill and Southampton, and eventually a prize piece of Sag Harbor, the roughly 22,000-square-foot corner at 2 Main Street and 22 Long Island Avenue, at the traffic circle where Bay and Main streets meet by the wharf. Morton paid $30 million for it in 2025, at the time the most ever paid for Hamptons retail.

The Sag Harbor purchase elevated Morton. Still, he appeared grumpy about being in the spotlight. (There are not even publicly available photos of him.) “People are buying properties in the Hamptons every day,” he told local news site 27East when a reporter asked about his Sag Harbor purchase. “Is there some kind of obligation for the media to write about it?”

Perhaps he had reason to be. According to multiple partners, buyers and investors, as well as lawsuits and liens against his properties, Morton sometimes skimped on paying contractors, was loose about project budgets and quietly stepped away from struggling projects on his way to building his portfolio. His precise outcomes are hard to track because he sometimes invested alongside partners, often cross-collateralizing projects. But a review of lawsuits shows he allegedly defaulted on millions in loans to three different lenders.

“He swings for the fences, is a great talker and is really good at presenting himself,” one former partner said.

“My businesses operate in contentious industries involving substantial commercial transactions,” Morton wrote in a statement to The Real Deal. “Litigation is an unfortunate but common feature of that environment. Many of the matters referenced involve disputed allegations that remain unresolved, and in several instances the claims lack merit or are already dismissed or settled. Because these cases are pending, I cannot fairly litigate them through the media, but I remain confident the court process will resolve them appropriately.”

Hamptons real estate can emit a siren song that’s hard to ignore for those who’d make it rich. But it’s not as easy as it looks to reap a fortune on the old potato fields. Home buyers are especially fickle about location and finish style, their budgets tied to the stock market and bonus pool. Retail is seasonal, and plenty of landlords cut deals to stay full through the winter; restaurants churn through operators and owners. Because profit isn’t a given, ownership of commercial, hospitality and retail can be a status symbol of its own, with major players RFR’s Aby Rosen, Apollo’s Marc Rowan and Mindy Gray, wife of Blackstone’s Jon Gray, recently picking up a Southampton movie theater, the Montauk lobster shack Duryea’s and Sagaponack general store, respectively, places they might manifest ideal summers, though locals often bristle at the sprucing up of quainter establishments.

This power move has trickled down. “I meet these new dads who are here, who say, ‘We should get a fund together,’” Compass’ Matt Breitenbach said. Breitenbach, who focuses on residential and was born in the Hamptons, said casual playground conversations can now turn into ad hoc fund pitches. “It’s a bit nuts. There’s a lot of money in that space,” he said.

“There was one bathroom that had, I want to say 13 pieces of hardware that each had different finishes.”

Morton topped out at about $100 million in Hamptons real estate, according to a review of property records. One source familiar with the finances of Excelsior, Morton’s development firm, said the business had been bringing in more than $10 million in revenue annually until the end of 2025.

Some of Morton’s partners say they’re happy with the results. “His performance as the GP was generally positive, and I was paid at or above the underwritten returns on the projects where I exited,” one recurring investor said.

Successes include a row of East Hampton properties at 15, 17 and 18 2nd Avenue — he built 15 and 17 from the ground up — that he sold in 2022 for more than $8 million, roughly triple what he paid in 2020. He also sold the Water Mill retail center for $13 million to Robert Zecher’s Vault Development Partners after buying it for $8.7 million two years prior.

But Morton’s current projects have mechanic’s liens filed from subcontractors for over $300,000. (“All of my liabilities have either been paid, negotiated, or are in the process of a positive resolution,” he wrote in an email.) Another former partner counted himself lucky: “I guess I came under that apron of monies that were needed to be paid to certain people.”

Last year, the people not getting paid started to swell. His portfolio rapidly dwindled, as foreclosures and liens have piled up on cross-collateralized properties, many of which have debts on them that he’s also personally guaranteed. He appears to have sold other properties after incurring sizable debts, or stepped away from ownership, according to sources familiar with his holdings. Revenue in his development company fell to near zero in recent months, a source familiar with the firm’s finances said. Morton did not respond to a question about his firm’s revenue.

Then, in May, Morton turned over the prime Sag Harbor retail corner to lender Mavik Capital. The comedown wasn’t just the end of a short-lived era as local mover and shaker but also sparked a bigger question: how he managed to level up from struggling on a couple small-time residential developments to scooping up several headline properties in the elite enclave.

“That man has a gift for getting money from people,” a source who worked with Morton on several projects, including his short-lived Morty’s Oyster Stand, told TRD.

Still, in April — the same month Morton was hit with the latest lawsuit this year, putting his alleged unpaid debts up to nearly $10 million, according to suits and liens — Morton and Brooke took a family vacation to a coastal resort town in El Salvador.

“Estoy bien,” Brooke’s Instagram caption said.

An expanding portfolio

Morton is from Minnesota, and his path to the Hamptons is fuzzy. Multiple people who knew or worked with Morton say he ran a construction-related business in Texas before moving to New York, where he met Brooke, who began bringing Morton out to a friend’s family’s place in Amagansett.

Jeremy does not seem to have come from the kind of money or status that would have given them access to the multimillion-dollar lifestyle they later enjoyed. Morton’s mom works as an account executive for a multi-level-marketing company, Energetix, which offers both holistic wellness products and jewelry, while his dad owns a now-defunct electrician shop, according to LinkedIn.

In 2016, Morton established his first Hamptons development outfit, Morton Custom Homes.

The following year, he closed on the company’s first three properties, vacant plots where he planned to build spec homes using his own money. Two were in wooded areas between East Hampton and Sag Harbor, and the third on Bittersweet Lane in Amagansett. The frames went up quickly on the East Hampton homes, but Morton struggled to finish them once the third project was underway, a source familiar with the projects said. By the end of 2017, he had lost all to the lender, according to the lender, Alfonso Kimche of North Hill Capital Management.

By 2019, he was back. For $1.3 million, he picked up Cyril’s Fish House, once known for its post-beach frozen cocktail, the BBC (Banana Bailey Colada). After losing its liquor license and falling afoul of the zoning code, Cyril’s had shuttered in 2016.

In 2020, he bought another trio of residential lots for $2.5 million in the same wooded area as his earlier residential projects.

He spent the next six years buying and selling. Morton added at least six more residential properties, paying about $11 million.

His splashiest deals were the restaurant and commercial purchases. In 2021, he paid $11 million for hotel and club-staurant Ruschmeyer’s, where A-list celebrities like Vanessa Hudgens and Naomi Watts gathered. He bought Rick’s Crabby Cowboy Cafe for $14 million, intending to turn it into a 14-key hotel, though the plan fell flat in front of the local planning board. He also scored the Water Mill retail space, home to the Soul Cycle and grocery store Provisions, for almost $9 million. He owned Provisions too.

The local real estate guys didn’t know Morton. “It’s a small circle, and he’s not really in it,” one active developer said. “Especially not anymore.”

Instead, Morton seemed to rely on wealthy friends. Documents show that he invested with Western Beef CEO Peter Castellana III, and sources say that his investors also included Hamptons regulars like Chirp Golf president Charlie Grace. Adam Whittingham and Michael Musante’s The MW Group, a small Connecticut-based firm, went in on the Sag Harbor project. Contacted for comment, the investors declined to comment.

Morton and Brooke’s social profile rose alongside Morton’s portfolio.

Months after closing on Cyril’s Fish House, Morton launched the stand as Morty’s Oyster House and hired celebrity chef Sam Talbot away from Surf Lodge. The restaurant made it onto nearly every major Hamptons summer preview list, from Eater to the New York Times. Laura Donnelly from the East Hampton Star admired how the spot — unlike some other redone mainstays — seemed true to its roots.

“I don’t usually get into the background of new owners, partners, investors, etc.,” she wrote, “but it is worth noting that these three fellas, Jeremy Morton, Jack Luber, and Charles Seich have the hospitality (and design and construction) chops to make this place a success. It’s not just another “Duryea-ization” of a beloved old rundown shanty.”

For July 4th of 2019, Morton attended a Studio 54-themed beach party with stars of “Real Housewives,” Ramona Singer and Kelly Dodd. The next day, he hosted his own birthday party at Morty’s. The following week, Morty’s did the catering for Gucci at an event in Montauk. In 2021, he threw his 40th, again at Morty’s, then brought in Diplo to DJ at Ruschmeyer’s for a daytime dance party that felt like the height of a post-Covid cultural and social comeback.

“What a summer,” Brooke captioned an Instagram story on Labor Day weekend, after another party at Ruschmeyer’s.

They couldn’t hang on. The Morty’s website still reads: “Thank you for a great 2022 Summer Season! See you in 2023!” but it never reopened. He sold Morty’s to David Miller for $2.4 million in late 2023, but despite the price increase did not make a profit after accounting for renovations.

Morton told TRD he exited Rick’s Crabby and Ruschmeyer’s in 2021. Neither reached their former level of local cachet. Rick’s burned down in 2023 and the ownership group for Ruschmeyer’s has gone through several attempted rebrands in the past few years.

Yet Morton continued buying, adding Southampton’s largest retail corner at 1-15 Hill Street and 1-17 Windmill Lane for $8.4 million in 2024. Last year, he bought the Sag Harbor corner at 2 Main Street and 22 Long Island Avenue, proposing to more than double the square footage of the retail spaces. Currently he appears to own a residential project at 126 Long Lane he bought for $2 million in 2023, another at 15 Fieldview Lane and his personal residence — all in East Hampton, according to property records.

Snags on spec

Morton’s earliest projects showed characteristics that defined his decade as a developer in the Hamptons.

About the time that Morton was doing his first projects in 2016, builders were testing the idea that buyers would consider high-end spec homes away from the well-trafficked coastal areas south of the highway.

Two of his first three lots were on Whooping Hollow Road, in the woodsy area between East Hampton and Sag Harbor. He paid $745,000, evidence of the iffy location, and planned two spec homes.

“He was really the first one to start building more expensive houses on Whooping Hollow,” said a source familiar with the projects.

In this, Morton was prescient: Sales for luxury homes north of Route 27 have crept up in recent years, but the lots in East Hampton on Whooping Hollow were relatively virgin when Morton started working on them.

He got an $850,000 construction loan from Kimche’s North Hill Capital Management, broke ground and got the frames up.

In the design, he seemed less savvy. “There was one bathroom that had, I want to say 13 pieces of hardware that each had different finishes,” a source familiar with the project said.

Morton went back to his lender for a second loan — around double the size of the first — to buy a third plot of land at 15 Bittersweet Lane, near Napeague Bay, where Amagansett starts to narrow toward Montauk. Kimche acquiesced, and Morton bought the new property for $1.8 million.

Less than a year into starting development, he handed back the keys on all three homes. “He bit off more than he could chew,” Kimche said. “He started just running out of capital and underestimating his expenses. It became clear he was not going to be able to complete them all.” Kimche oversaw the completion of the homes, eventually selling them for almost $8 million combined.

“Jeremy was dancing. He was excited.”

At a 2022 project at 73 Wainscott Stone Road in East Hampton, he got further, buying the property for $3.4 million and building a resort-style estate with a heated gunite pool, spa, gym, a private theater, sauna, steam shower and three-car garage, according to Zillow.

But he kept needing more money to finish. By April 2024, he had taken out a loan for $12.4 million, which refinanced a previous $5 million on the house. The new loan was collateralized by another home and matured in just six months.

The Wainscott Stone house sold this year for over $12 million, property records show.

Loan documents between Morton and U.S. Strategic Capital show that Morton took out $3.8 million from the lender to buy an investor on the project, developer Roy Stillman, out of two ownership entities, one of which was tied to 73 Wainscott Stone Road. Stillman said he was paid back “100 cents on the dollar,” while Morton took back nothing.” “The proceeds I received from U.S. Strategic Capital were used for exactly what they were drawn for. Investors were paid exactly how they were supposed to be and in full,” Morton wrote.

Morton “had a lot of transactions going on at once,” Stillman said at the time. “Which was likely a mistake.”

One of those other deals was an ambitious build at 825 Old Sag Harbor Road in Water Mill, on a property Morton had bought in 2022 for $1.6 million. He planned a sprawling 12,000-square-foot, shingled home with nine bedrooms and 12 bathrooms. Melvin Rodriguez, whose wife Monique founded and sold Mielle Organics to P&G in 2023 for $600 million, agreed to pay $10.4 million in February 2025, according to documents in a lawsuit filed by a cash advance company in January.

“Jeremy was dancing,” a source familiar with the deal said. “He was excited.”

Commercial difficulties

That Morton, who struggled on three small-time residential projects, was unable to manage a more mature portfolio that included food and beverage and commercial is perhaps not a surprise. Bureaucratic quagmires are part and parcel of developing in the Hamptons.

“The towns are not easy,” Breitenbach said.

Soon after the close, Ruschmeyer’s encountered issues, including the loss of its liquor license.

After Morton exited the project in 2021, the remaining ownership group, now led by Castellana, began shopping the site.

“During my involvement in 2021, Ruschmeyer’s performed very well and I am proud of the momentum created,” Morton said. “There were complications involving the transfer of liquor licenses from the prior ownership, so I exited my involvement at the time of the new liquor license application.”

Rick’s, which Morton also owned with Castellana, also had a snafu with its liquor license, which led its former owner, Richard Gibbs, and Morton to sue each other in summer 2021. “We were not going to achieve a short term profit by selling $10 hamburgers and salads after a $14,000,000.00 investment, but rather by continuing to sell alcohol and putting on events,” Morton wrote in a court filing the following year.

About the same time, in December 2021, the East Hampton Town Planning Board nixed Morton’s plans to expand the Rick’s property into a resort, with a single-family residence, 110-seat restaurant, bar, swimming pool and fitness center. “I just want to emphasize that this project is way too large,” one planning board member said at the time. “There are so many different problems with it.”

Morton’s most ambitious proposal, for the Sag Harbor retail property, involved doubling the square footage to increase the number of businesses to 27 from 15. The Sag Harbor Village Planning Board was skeptical about the disruption to the intersection.

“You’re going to have no business use [or] pedestrian use for multiple years,” board member Drew Harvey said, shocked, at a November meeting. “It’s a big ask. It’s a huge construction project. Is this what we’re sticking with?”

Yes, Morton told them.

Months later, when he turned the keys over to Mavik, he had changed his tune.

“The project required a number of approvals and entitlements, and unfortunately those approvals were not obtained within the timeframe required by our financing,” he said in a statement.

Money troubles

Morton’s troubles, though, seem to derive from more than difficult approval processes.

At his project at 825 Old Sag Harbor Road, Morton struggled to close the deal with Rodriguez. The Zillow listing shows that the property entered into the MLS as pending sale four separate times before being removed. Sources familiar with the project said work stalled after Morton didn’t pay contractors.

“Melvin was like ‘What the hell, why is this taking so long?’” the source said.

A source familiar with Morton’s Sag Harbor project said that the financial stress from residential projects not closing impacted his ability to fund pre-development costs in the retail investment. Morton said this was “not factual in any way” and that he nor other members of the investor group “were required to provide ongoing funding of this property in this way, all capital came from interest reserve and rental income.”

For the next year, Morton began the scramble of his life. He mortgaged his remaining properties and took out ultra-short term loans, according to lawsuits filed from several of his lenders.

Morton mortgaged his personal East Hampton home for $5 million in March 2025. Four months later, he took out nearly $4 million in bridge capital from U.S. Strategic Capital, collateralized by his own home and by one of the residential homes he still hasn’t sold, the one at 126 Long Lane. He also got $300,000 from Simply Funding, a cash advance firm which he quickly stopped making required payments on. Contractors at Long Lane are also owed $300,000, according to mechanic’s liens filed on the property in the last year.

In November, he allegedly defaulted on his loan from U.S.S.C. and the original $3.8 million construction loan from Temple View Capital he had taken out for Long Lane, according to lawsuits from both lenders. In December, he allegedly defaulted on the mortgage on his personal home, per another lawsuit filed by his lender, JPMorgan Chase. Morton says the defaults are in the process of being remedied.

Two months later, the MW Group, investors in the Sag Harbor retail corner, filed an $850,000 collateral mortgage on the same residence.

In May, a court ruled that Simply Funding had the right to Morton’s ownership interests in eight different entities. It’s not clear how valuable those are, as Morton’s creditors continue to battle over his portfolio’s scraps. “Simply Funding, as part of a collection strategy, took ownership of closed special purpose entity companies that are irrelevant to any day to day operations,” Morton stated in an email. “This collection activity has stopped as this loan is being paid as agreed.”

The sale of 825 Old Sag Harbor finally closed in February, according to property records.

Even before the closing, Morton began to fundraise for three new projects, according to investor documents shared with TRD.

In October, he closed on one, an East Hampton lot, for $3 million.

The documents project a 60 percent return.