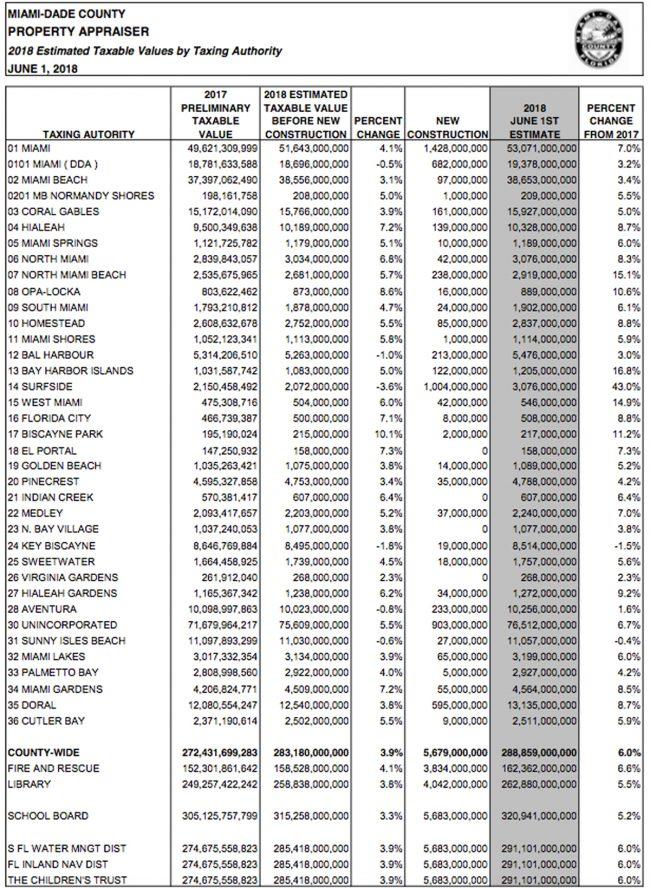

Miami-Dade County’s taxable property values rose 6 percent to $288.86 billion in 2017, despite the condo market slowdown.

The county’s property appraiser, Pedro J. Garcia, released the June 1 estimates, showing that property values are growing at a slower pace than in previous years. Garcia said in a release that the oversupply of condos put downward pressure on condo values, but that the short supply of mid-range single-family homes increased property values.

The largest project to be completed last year was the Four Seasons Residences at The Surf Club in Surfside with an assessed value of about $1 billion. The luxury condo development caused values to jump 43 percent — the highest increase countywide — in the town of Surfside to more than $3 billion.

Next door, in Bay Harbor Islands, taxable property values rose by 16.8 percent to $1.2 billion.

Garcia’s estimates show that values fell in Key Biscayne, by 1.5 percent to $8.5 billion; and in Sunny Isles Beach, by 0.4 percent to $11 billion, compared to the previous year.

Overall, the county saw more than $5 billion in new construction last year. More than $1.4 billion of new development was completed in the city of Miami, which includes 1010 Brickell, a 389-unit, 50-story condo tower with a projected sellout of more than $262 million. Cities like Doral, Aventura, North Miami Beach and Bal Harbour also saw a significant amount of new construction.

From 2014 to 2015, Miami-Dade property values jumped 9.4 percent to $230.4 billion, and from 2015 to 2016, they were up 9.1 percent to $251.3 billion. From 2016 to 2017, they rose 8.2 percent to $272 billion.

Garcia will release the 2017 assessment roll on July 1. Here’s a full list of the estimates: