Everyone loves a dynasty. But few fields are as dominated by hereditary empires as real estate. If the business is built on relationships, as industry players like to say, why not tap into your folks’?

For those on the inside, inheriting or working for family business is a source of pride, a step toward creating a legacy. Outsiders, though, have invented a new term.

“Nepo babies” — a short and not-so-sweet nickname used to describe the offspring of the rich and famous who have professionally benefited from their family line — often fight the label. The term has captured media attention across the country, making its way into the zeitgeist in everything from Hollywood and politics to Formula One and tennis.

And there is no legacy shortage across commercial real estate.

From former President Donald Trump and Jared Kushner to Rob Speyer and Billy Macklowe, the industry is full of second-, third- and fourth-generation real estate executives who have taken the reins from their predecessors. They embody the stories we love to see on television — from the Roy children squabbling over their father’s business in “Succession” to John Dutton just trying to keep enough of his children alive to inherit his beloved Montana ranch in “Yellowstone.”

This month, The Real Deal took stock of some of the legacy kids — counting them all would take hundreds of pages — who have set up shop and built and sold towers across New York, Los Angeles and Miami.

The blue bloods

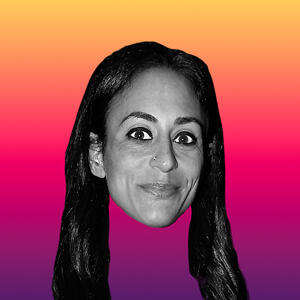

Jared Kushner and Nicole Kushner Meyer

Jared Kushner and Nicole Kushner Meyer

Jared Kushner needs no introduction. The son of real estate developer Charles Kushner, he took over the family business during his father’s incarceration in the mid-2000s. But running Kushner Companies, which today owns more than 26,000 apartments, was not his last brush with nepotism.

In 2017, Jared Kushner was named a senior White House adviser, serving at the pleasure of his father-in-law, then-President — and nepo baby himself — Donald Trump. Kushner stepped down as CEO of the family investment firm and passed the reins to his sister, Nicole Kushner Meyer.

Nicole Kushner Meyer (who lately seems to go by Nicole Meyer more often than not) was appointed as president in 2021, but not CEO. The top job went for the first time to someone outside of the family, Frenchman Laurent Morali.

As the scion of a storied real estate family — her grandfather, Joseph Kushner, was among the New Jersey developers known as the “Holocaust Builders” — Nicole gets the generational aspect of the real estate game.

“Every opportunity we look at, we look at it in that long-term lens and we look at it to hold forever,” she said at a TRD event in 2021.

Stefan Soloviev

Sometimes, children of famous parents will try to distance themselves from the weighty family name. Take Stefan Soloviev, son of one of New York’s most prominent developers, the late billionaire Sheldon Solow.

Soloviev, who adopted the Russian version of his last name, inherited his father’s $4.4 billion real estate fortune, including perhaps New York’s most prestigious office building, 9 West 57th Street, which sits on the edge of Central Park.

But Soloviev has focused his efforts — and deep pockets — less on expanding his father’s Manhattan empire and more on buying large tracts of land throughout the West. As of last year, Soloviev owned over 400,000 acres of farmland across Colorado, Kansas, New Mexico and Texas, as well as New York, making him the country’s 26th largest private landowner, according to the Land Report.

Still, he is taking after his father in some ways. He wants to build a casino on an East Side parcel near the United Nations that Solow long sought to develop, and he’s tapped his son Christian — one of his at least 20 children (reports vary) — to head up about 1,100 acres of farmland on the North Fork of Long Island.

Rob Speyer

When Rob Speyer was named the sole CEO of Tishman Speyer in 2015, it felt inevitable. The son of company co-founder Jerry Speyer, Rob had been sharing the title of co-CEO with his father since 2008. The duo in their 2015 announcement called the move a “natural progression.”

After working as a reporter for the New York Daily News, Rob joined the family business in 1995, when he was in his mid-20s. Ten years later, he was driving the firm’s $5.4 billion acquisition of Stuyvesant Town and Peter Cooper Village in Manhattan — a deal that blew up after Tishman Speyer and its partner BlackRock defaulted on $4.4 billion worth of debt.

After working as a reporter for the New York Daily News, Rob joined the family business in 1995, when he was in his mid-20s. Ten years later, he was driving the firm’s $5.4 billion acquisition of Stuyvesant Town and Peter Cooper Village in Manhattan — a deal that blew up after Tishman Speyer and its partner BlackRock defaulted on $4.4 billion worth of debt.

That setback was not enough to disrupt the succession. In 2017, his father tapped Rob to help him lead the firm, whose portfolio, now at 90 million square feet, includes some of the world’s most recognizable properties.

When asked last year what he learned from the Stuyvesant Town debacle, Rob pointed to development milestones he takes credit for.

“We have a global portfolio of $65 billion, we did over 50 million square feet of development over the last 10 years, and during the last couple of years, we’ve not had a single impairment that has forced us into a difficult discussion,” he told TRD in June. “You have to be humble enough to learn.”

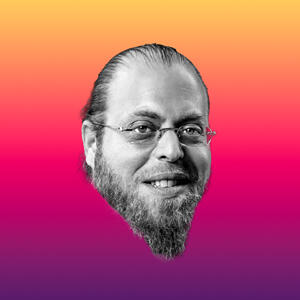

Billy Macklowe

Billy Macklowe

When you hear the last name Macklowe, Billy isn’t the first person who comes to mind. His father, Harry, is one of New York’s most prolific developers. The founder of Macklowe Properties, Harry Macklowe is often referred to as a titan, a tycoon or a legend.

Like Rob Speyer, Billy also joined his father’s firm in his mid-20s, after a short stint in banking. He was named president in 2002 and helped Harry lead the company through the financial crisis, including selling one of its crown jewels, the General Motors Building, for $2.8 billion to pay the firm’s debts.

After the crisis, their relationship soured. Billy branched out on his own to form William Macklowe Properties. He blamed his father for “making numerous mistakes that led the company to the brink,” according to the Wall Street Journal. But the family feud didn’t end there.

In 2016, his father sued Billy, claiming his son had threatened to stop providing administrative support to Macklowe Properties. The suit centered around who had the rights to the Macklowe.com domain name.

It wasn’t about money: The two were “fighting over the family name, the family identity,” commercial real estate attorney Joshua Stein said in 2017.

“Dad always had the experience of starting his own company,” Billy said in 2012. “I don’t think it’s a question of filling my dad’s shoes.”

The under-the-radars

Andrea Himmel

Andrea Himmel

Andrea Himmel says that when she graduated from Wharton in 2008, no one in real estate would give her a job. Her mother, Leslie Wohlman Himmel, co-founded the investment firm Himmel & Meringoff Properties, which has bought and redeveloped more thn 5 million square feet across New York City. Leslie wouldn’t hire her, either.

“You can never work here,” Andrea recalled her mother telling her. “Family businesses implode.”

Times change. She’s now the firm’s chief investment officer, a role she has held since 2018, but only after establishing a name for herself in private equity. Himmel joined Sanders Capital, an investment firm run by former AllianceBernstein CEO Lew Sanders, and eventually ended up running its energy portfolio. She went on to start two private equity firms that invest in oil and gas assets in Texas.

“After my mom saw me successfully raise money in that space, she said, ‘We would love for you to come here,’” Andrea recounted, acknowledging that people shrug her off as a nepotism hire.

“There are certainly folks who write off people with the same last name, but it’s motivation to work harder,” she said.

Andrea’s brother David is also active in the New York industry, though she said he shies away from the last name more than she does. David is an executive at Jamestown, the firm that owns One Times Square and Industry City in Brooklyn, among other properties.

Kathryn Kalikow

Peter Kalikow never demanded that his daughter, Kathryn, join his real estate firm, HJ Kalikow, but he did welcome it. Kathryn is the fourth-generation Kalikow to work in the family business — the first was her great-grandfather Joseph, who started investing in Bensonhurst after he arrived from Russia in the early 1900s.

“We’re as dynasty as you can get, really,” Kathryn said. “I didn’t think it was what I wanted — I wanted to find my own path.”

About 10 years ago, Kathryn made headlines for getting arrested for selling heroin and admitting a drug addiction. She worked as a sobriety counselor in Connecticut for six years, and planned on moving to New York at the beginning of 2020. After the pandemic hit, her career got put on hold, and Peter persuaded her to join the business.

“I did love that there was a family legacy aspect,” she said. “But I have a lot to learn.” She took a real estate economics class at NYU and says she tries to sit in on every meeting.

“We’re a mom-and-pop operation,” she said — one that happens to own a 1.3 million-square-foot tower at 101 Park Avenue.

The Dursts

Alexander, Helena and Lucas Durst

Alexander, Helena and Lucas Durst, and their cousin David Neil, make up the fourth generation of the Durst dynasty, which traces back to the early 20th century. Their great-grandfather, Joseph Durst, immigrated to the U.S. from modern-day Poland and started manufacturing clothing, eventually investing the profits in real estate.

Douglas Durst, who runs the Durst Organization with his cousin Jonathan “Jody” Durst, is dad to Helena and Alexander, who joined the firm in 2001 and 2005, respectively. Helena now oversees the company’s residential portfolio — about 2,000 units — a gig she took over from Alexander, who is now Durst’s chief development officer.

The legacies

John Kilroy Jr.

John Kilroy Sr. founded Kilroy Realty’s predecessor in 1952, first focusing on office campuses near the Los Angeles and Long Beach airports. He handed over day-to-day operations to his son while he was in his 50s — relatively young for retirement.

The younger Kilroy started buying up properties in Hollywood, San Francisco and Seattle. Today, the real estate investment trust has a market cap of $4.6 billion.

“His son has built the company into a huge operation,” John Cushman III, the former chairman of Cushman & Wakefield, told the Los Angeles Times when John Kilroy Sr. died in 2016.

Jaime Lee

Jaime Lee has emerged as the face of Jamison Properties, a residential landlord in L.A. that has delivered more than 5,000 units since 2013.

After toying with other interests in college, studying English and considering an MFA in creative writing, Jaime submitted to her father’s “master plan” — a real estate company run by his children. She joined Jamison as an office assistant before college. By the time she went to law school, she was managing the California Market Center, a 1.8 million-square-foot development in DTLA.

Asked whether she would ever take over from her father as the head of Jamison Properties, a large residential landlord in L.A., Jaime said that decision was still up in the air.

“I think as long as he is involved he will always be the patriarch, and he’s the founder,” she said in September. “We’ll see what happens.”

Christopher Rising

Chris Rising wanted to be a football player, not a real estate one. After playing for Duke University, he became a high school football coach, went to law school and worked at Pillsbury, Madison & Sutro, then chose to become a broker at Cushman Realty. Eventually, he started his own firm, The Rising Real Estate Group.

Meanwhile, his father Nelson had become the CEO of publicly traded MPG Office Trust. At the time, MPG owned the U.S. Bank Tower and was considered the largest office landlord in Downtown L.A. Chris was hired to oversee acquisitions. Once Nelson resigned as CEO in 2010, Chris went with him. The two then founded Rising Realty, now a major Downtown L.A. office landlord and industrial owner.

“I was very pleased when Christopher chose to join me in real estate,” Nelson said in 2019.

Bret, Rufus and Patricia Hankey

Bret and Rufus Hankey

Don Hankey didn’t score his fame from his real estate holdings, but from giving out car loans to those with bad credit. But, the billionaire was thrust into the spotlight in recent years after loaning $82.5 million on Nile Niami’s Bel Air megamansion “The One.” Hankey filed to foreclose on the unfinished mansion after Niami defaulted.

All three of Hankey’s adult children work at his conglomerate.

Rufus Hankey founded his own housing development firm (though it’s part of Hankey’s conglomerate) called Knight Development Group. Bret Hankey is heading up his father’s subprime auto loans business Westlake Financial. Patricia, Don Hankey’s daughter, is a risk manager for Hankey Capital, the entity that gave Niami the hefty loan.

Rommy Shy

Rommy Shy — son of the infamous L.A. landlord Barry Shy — took the reins of his father’s investment company SB Properties as chief management officer in 2007. Entities linked to SB Properties sold five buildings in Downtown L.A. last year for $402 million.

Despite some involvement with his father, Rommy has moved on to the brokerage business. He’s currently the president of his own firm, Royalty Realty, where he has sold about $200 million worth of homes across L.A.

The renowned

Gil Dezer

Gil Dezer

“He told me to go earn my worth in the market,” Gil Dezer said of his father, Michael Dezer. “Then he said, ‘I’ll pay you 10 percent more because you’re my son.’ That was the deal.”

Gil has run luxury condo builder Dezer Development since 2007, after his father stepped back from the company. He gives himself credit for building up his development brand in Miami: constructing six Trump-branded towers as well as the Porsche Design Tower and Residences by Armani/Casa.

But he proved himself to his father — and the rest of the Miami real estate industry — before that.

“After 2008, I was able to pay off $475 million in debt in 2011,” he boasted. “I was the one who paid off the loans. It opened the door for us.”

When asked if anyone brushed him off because he was his father’s son, he emphatically interrupted: “Absolutely, all the time. People said, ‘The rich kid is just having fun.’ But it became obvious that the company was mine and I’m the one calling the shots.”

Gil’s favorite hobby, which he also inherited from his father, may have fed that perception. He owns dozens of expensive sports cars, including a Bugatti Chiron and a McLaren F1, and he says he drives them all.

Jackie and Jeffrey Soffer

Jackie and Jeffrey Soffer

“I wanted to be a ski instructor in Denver,” Jackie Soffer told TRD. Her father, real estate developer Donald Soffer, had other plans. He told her he didn’t send her to college for four years for her to work at a ski school, she recalled.

“So, I did what I was supposed to do,” Jackie said.

Today, Jackie is the CEO of her father’s firm, Turnberry Associates, which owns the Grand Hyatt Miami Beach and the 2.8 million-square-foot Aventura Mall. She ran the family firm jointly with her brother, Jeffrey Soffer, for decades before Jeffrey split off in 2019 to launch his own company. Despite running Turnberry, though, she still lets others give her father credit for her achievements at the company.

A few weeks ago, she and an associate were touring Destin Commons, a roughly 500,000-square-foot shopping center in northwest Florida. He asked Soffer when her father built it.

“I did, 20 years ago,” she said. “I never cared about making a name for myself.”

Jackie’s children will have to earn their own, she said. “They have to feel like they earned it and weren’t given it. I think the worst thing is to have children who are entitled.”

At one point during the 25 years she worked with her brother at the family firm, Jeffrey fell for a scam involving a fake Saudi prince, who had proposed to buy into the Fontainebleau Miami Beach for well above the hotel’s valuation. The buy-in never came, but Jeffrey handed over $150,000 worth of gifts to the con man.

The siblings split up in 2019, with Jeffrey going on to found Fontainebleau Development, which owns the Fontainebleau Miami Beach and recently scored a $2.2 billion construction loan for a project on the Las Vegas Strip.