Ultra-wealthy out-of-state buyers are flocking en masse to South Florida, scooping up multimillion-dollar homes and condos with plans to establish residency in order to avoid shelling out money to the government as a result of last year’s tax reform, brokers and developers told The Real Deal. The influx has local brokerages doing everything they can to capitalize on the trend, using their partnerships with far-flung firms to grow their client rosters ahead of the competition.

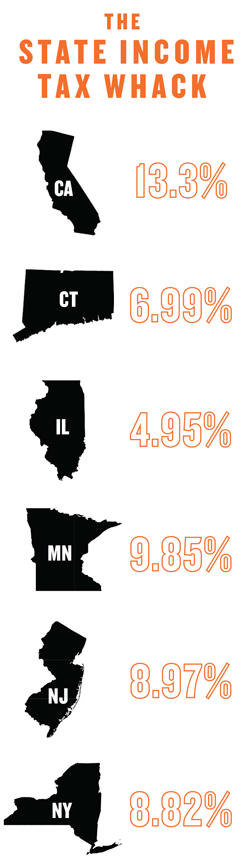

The out-of-staters are largely top-earning hedge funders, real estate bigwigs, big-time entrepreneurs and CEOs from states such as New York, New Jersey, Connecticut, California and Illinois — places with state income taxes as high as 13.3 percent, and even city taxes in the case of New York City. Florida, on the other hand, has no state income tax.

“It’s one thing when the tax reform gets passed, and it’s another thing when you’re sitting with your accountant and you say, ‘Shit, I could just to move to Miami,”’ said Oren Alexander of Douglas Elliman.

Nelson Gonzalez of EWM Realty International calls the new buyers “tax refugees,” and said they account for 90 percent of those looking at his high-end listings. He has shown properties priced over $10 million or $15 million to at least 40 such ultra-wealthy buyers in the past few months, he said.

When Gonzalez showed a unit at luxury condo building Apogee South Beach to three different buyers who were all in the elevator together, Gonzalez asked, ‘“Why Miami, why are you moving from New York?’ One said ‘Taxes,’ and the others said, ‘That’s why I’m here,’ ‘That’s why I’m here.’”

“Hedge fund guys make $50 to $150 million a year, and these guys can come down here and buy a $10 to $20 million house, and with the tax savings, they get a free house in two to five years, and they get to live in paradise,”Gonzalez said.

Real estate insiders point to Barry Sternlicht, chairman and CEO of Starwood Capital Group as a leader of the trend. In 2015, the mogul bought a waterfront vacant lot on Miami Beach’s North Bay Road and built a mansion for his permanent residence, then later moved his company’s headquarters from Greenwich, Connecticut to Miami Beach. During a keynote session at a University of Miami real estate event in 2014, Sternlicht said, “My generation, which is the tail end of baby boomers, we’re coming. We’re changing our addresses and we’re coming to low-tax states.”

In the U.S., the vast majority of states levy income taxes. For those earning at the top level, the state taxes can be as high as 8.82 percent in New York; 8.97 percent in New Jersey; 6.99 percent in Connecticut; and 4.95 percent in Illinois. California has the highest state income tax in the nation, topping out at 13.3 percent for those earning more than $1 million.

The Tax Cuts and Jobs Act, passed in December 2017, limited the ability of taxpayers to deduct state and local taxes (SALT) from their federal taxable income in 2018. That has dealt a significant blow, experts said.

Changing state residencies to avoid these taxes is not an easy task. You must provide proof that you are not in your former home state for more than 180 days a year. And to establish residency in Florida, you must secure a driver’s license and follow other legal requirements. Florida also has property taxes of about 2 percent of the assessed value, which is a lower rate than that of about half of the states in the country.

Changing state residencies to avoid these taxes is not an easy task. You must provide proof that you are not in your former home state for more than 180 days a year. And to establish residency in Florida, you must secure a driver’s license and follow other legal requirements. Florida also has property taxes of about 2 percent of the assessed value, which is a lower rate than that of about half of the states in the country.

It’s “really a no-brainer,” said Camille Douglas, senior managing director at LeFrak, the co-developer of 1 Hotel & Homes South Beach and the future North Miami mixed-use project SoLe Mia. “If you already think it’s nice to have a place in Miami, you’re now hugely motivated to pull the trigger. And it is almost free to become a Florida resident because your tax savings will support it.”

For Eloy Carmenate of Douglas Elliman, the volume of out-of-state residents earning tens and hundreds of millions of dollars who are looking at Miami properties is unprecedented. “I’ve never seen this super wealth come into town like this year,” he said. They’re looking at both condos and houses, Carmenate said, often from Miami Beach’s North Bay Road to the Sunset and Venetian islands.

“They’re pretty down to earth and unassuming,” he said. “They want to be able to walk down the street without bodyguards, go to restaurants.”

According to April figures from the Miami Association of Realtors, people from New York City ranked first among all cities searching for properties on MiamiRealtors.com. California ranked as the top state.

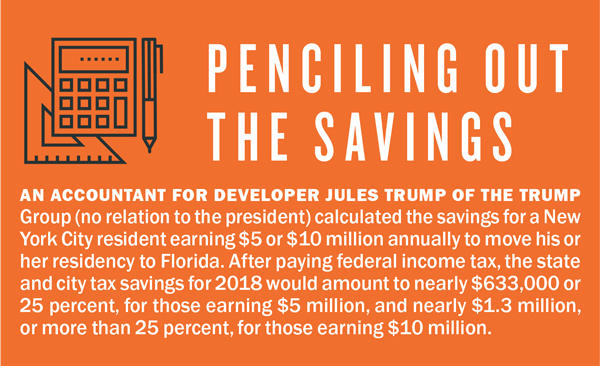

Developer Jules Trump of the Trump Group (no relation to the president) has watched wealthy families come down from the Northeast to vacation at his Acqualina Resort & Spa in Sunny Isles and become buyers at his Mansions at Acqualina and Estates at Acqualina intending to stay.

“After a few days at the hotel, the kids start pressuring, and the wife starts pressuring, and from a little thought in the back of their heads, it becomes a thought that ‘I’ve got to be crazy not to do it,’” said Trump. “They see that the living here is a much nicer lifestyle than what they could ever have in the Northeast.”

Real estate insiders say that while a handful of other states — including Alaska, Nevada, South Dakota, Texas, Washington and Wyoming — do not currently have an income tax, Florida is often viewed as the most desirable residence.

Reaching the out-of-staters

Some brokerages are shifting their strategies to reach buyers from high-tax states. Cervera Real Estate, which has a partnership with Stribling & Associates, held a seminar in New York to educate agents on how to purchase real estate and establish residency in Florida, said Alexandra Goeseke, Cervera’s director of general real estate. Cervera, which in the past typically received several referrals a month from Stribling, is now seeing many more referrals out of New York, she said.

Douglas Elliman is taking advantage of the presence it has in New York, New Jersey, Connecticut and California, said Jay Parker, CEO of Douglas Elliman’s Florida brokerage. “We’re at a point where the Trump tax plan has paid into our strategy perfectly, because we have agents in those markets that are already comfortable on referral business, and have a client pool that is now motivated and forming inquiries about that transfer [of residency].”

Agents like Elliman’s Carmenate say they are traveling to the Hamptons and New York City repeatedly to market properties and make presentations to prospective buyers.

One Sotheby’s International Realty is also working with its affiliates in markets such as New York, New Jersey, Connecticut and California, according to the firm’s president, Daniel de la Vega. Over the summer, its agents will host events in the Hamptons. “Our strategies include traveling to these markets and hosting events where both brokers and clients alike can learn more about South Florida real estate,” de la Vega said.

Brown Harris Stevens is using its internal referral network and sending agents from Florida to New York to give presentations to agents, said BHS Miami President Phil Gutman. Social media is also being targeted to the Northeast, highlighting property listings and the South Florida lifestyle. It’s helping drive viewers to the brokerage’s website, where traffic has spiked about 25 percent from Northeast buyers, he said.

Brown Harris Stevens is using its internal referral network and sending agents from Florida to New York to give presentations to agents, said BHS Miami President Phil Gutman. Social media is also being targeted to the Northeast, highlighting property listings and the South Florida lifestyle. It’s helping drive viewers to the brokerage’s website, where traffic has spiked about 25 percent from Northeast buyers, he said.

And Beth Butler, general manager of Compass Florida, said agents in South Florida “are relying on agents in other parts of the country to work their databases and send people our way, and that has been working effectively.” In the $3 to $5 million range, families are gravitating to secondary markets like Naples and Jupiter, she added.

For the Keyes Company, CEO Michael Pappas said sales have skyrocketed in the million-dollar-and-up sector of the market — up 35 percent in the first quarter, year-over-year. “These are sophisticated buyers. Many times, [a purchase] is the beginning of their move,” he said.

Keyes’ commercial brokerage is also hearing from a number of financial firms that want to relocate to Palm Beach County or open branches in the state to escape onerous taxes.

Financial firms are mostly looking at Boca Raton and West Palm Beach, said David Joseph, director of Keyes’ commercial division. Biltmore Capital Advisors, an investment adviser based in Princeton, New Jersey, opened an office in Boca Raton. The firm purchased three office condos in February. Atlantic Street Capital Management, a Stamford, Connecticut-based private equity firm, leased nearly 4,000 square feet at 515 North Flagler Drive in West Palm Beach in April. Parker of Douglas Elliman attributed the increase in high-end residential sales to tax reform, but he said they are also being driven by the “strong maturation of our market.”

“A lot of people are able to make the move, but now we have a product and a market that can substantiate their tastes,” Parker said.

Taxes aren’t the only thing drawing out-of-staters to South Florida, according to de la Vega of One Sotheby’s. Sellers are slashing their prices, especially on the high end of the market, where inventory is excessive. “As you go up in price point, days on the market are increasing and months of inventory are increasing pretty significantly,” de la Vega said. “Everything is price-sensitive and everything becomes a comparable.”

In May, AQR Capital Management co-founder Cliff Asness paid $26 million for a penthouse at 321 Ocean, marking the most expensive condo sale of the year. But the five-bedroom unit actually sold at a 51 percent discount off the $53 million asking price in 2015.

And about a month earlier, Asness’ business partner John Liew picked up a unit at the nearby Apogee in Miami Beach for $13.5 million, $1 million off the ask. Both Liew and Asness are billionaires who live in Greenwich, Connecticut.

Common concessions

Incentives are also a factor for sales. On the new construction side, developers are offering buyers sweeteners to close deals.

For projects that are nearly or just completed, developers are including the finishing touches for buyers — offering to throw in flooring and wall treatments that wouldn’t normally come with a new unit, said Edgardo Defortuna, president and CEO of Fortune International Realty.

Of the six units remaining at Fortune’s Jade Signature, a luxury condo tower in Sunny Isles Beach, Defortuna said he is “finishing” three units. At other projects, he’s seen developers offer the same for units on the less popular configurations for a limited period of time.

That means the developer is eating the cost, which typically ranges from $100 to $150 a foot to “finish a unit well.” The Estates at Acqualina and Turnberry Ocean Club are among those delivering units finished.

For buildings that aren’t as close to opening, developers are still reducing deposit requirements and offering discounts on a per-square-foot basis “if the price is right,” Defortuna said.

While Elliman’s Parker said the firm isn’t “engaged in any sort of incentive-based draws,” some projects Elliman is marketing are now offering furniture packages to buyers for an extra fee.

As the flow of out-of-staters continues, certainly one thing is changing for brokers, according Danny Hertzberg of Coldwell Banker’s the Jills: “We’re all becoming a bit of tax experts.”