Last week, famed short-seller Carson Block marked Blackstone Mortgage Trust for death, or something like it.

The founder of hedge fund Muddy Waters said the real estate investment trust was at risk of a liquidity crisis, according to Bloomberg.

As much as 75 percent of Blackstone Mortgage or BXMT’s borrowers are unable to cover interest expenses without rate swaps, which offer insurance against rising rates, Block said on CNBC. Some $16 billion in swaps on the REIT’s $23 billion loan book are set to expire next year.

The firm’s analysis, which targeted BXMT’s collateralized loan obligations — the short-term, floating-rate debt favored by value-add multifamily buyers — showed “most of those assets are underwater, basically below the loan values, by about 20 percent.”

Given that distress, Block forecast that most borrowers will be unable to refinance and that Blackstone Mortgage, to insulate itself from heavy losses, would be forced to modify loans.

Short-sellers are known for publicly bashing the stocks they are wagering against. But insiders say a similar real estate story is playing out across the bridge lending space, a market that bet big on multifamily syndicators.

“What [Block] found, it lines up with what we’re seeing in the deals we’ve looked at,” said Brian Underdahl, head of analytics for Nuvo Capital Partners. His firm is helping to recapitalize the troubled deals of syndicators who pooled money to buy properties when interest rates were low.

Those investors’ debt service on floating-rate loans has soared. Meanwhile, buyers have demanded higher cap rates, driving building values down by as much as 40 percent in some markets. Industry observers say sponsors who regularly borrowed at 70 to 80 percent leverage have seen their equity wiped out. For most, that means refinancing is off the table unless they can inject more capital.

Meanwhile, debt funds, many with sizable exposure to the space, aren’t yet willing to take losses. Rather, they are turning a blind eye to a maturity or technical default if a sponsor continues to make interest payments.

Insiders say lenders can’t do that forever. As Block predicted for BXMT, sector-wide defaults are poised to mount. As more loans come due, industry observers expect lenders will formally extend loans, hoping rates eventually subside.

Falling rates, however, may not be the savior the industry is banking on.

BXMT: Nothing to see

Blackstone pushed back on Block’s assessment and predictions.

Pointing to a BXMT third-quarter fact sheet, a spokesperson countered that the trust’s borrowers had virtually no rate swaps, as Block said, only rate caps. (Both instruments provide insurance against rising rates.)

The report noted that 93 percent of sponsors that had a cap expire in the past year bought a new one, and 95 percent of the REIT’s loans were performing as of Sept. 30.

Further rebutting Block’s predictions of refinancing difficulty, the sheet showed 90 percent of BXMT loans that matured in the past 12 months had either been repaid, fulfilled the requirements for an extension, or been extended with more capital from sponsors.

The REIT also highlighted in its third quarter earnings call that its multifamily loans are conservatively leveraged at 68 percent on average, setting those sponsors apart from other syndicators.

Taken together, those figures show health, but are a snapshot of a trailing 12-month period in which distress was just starting to show. For multifamily firms with CLOs, money troubles cropped up just before the summer and spread through the fall.

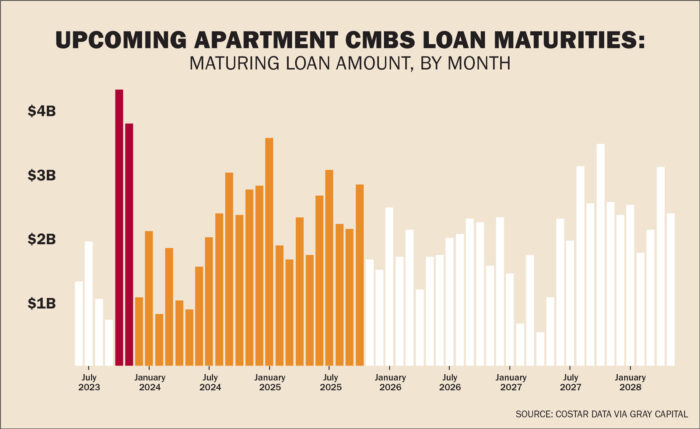

BXMT’s figures also predate the multifamily market’s wall of maturities. A record number of securitized loans backed by apartments are coming due by the end of 2025. The first wave of maturities hit in the fourth quarter of 2023, and another is expected in the second half of next year.

Insiders expect both peaks to drive more delinquencies and defaults.

Blind eye

As fourth-quarter due dates flew by and sponsors failed to repay their debts, many bridge lenders did nothing, according to people in the industry.

The strategy: Don’t look a gift horse in the mouth.

So long as the borrower continued to make payments after the loan matured, even if they were less than the regular monthly amount, lenders were willing to accept whatever the borrower could scrounge up.

Lenders are taking a similar strategy with loans in technical default, for example, those flagged for failing to meet mandated debt-to-income ratios.

“As long as a borrower is timely paying the debt service during the term of the loan, I have not seen any lenders foreclosing on anyone,” said Anton Mattli, founder of Peak Financing.

That’s likely because it would mean taking a haircut. Auctions have often drawn bids below the amount of the debt and lenders aren’t yet willing to execute short sales.

Work it out

Eventually, lenders will be forced to act and it’s likely they will turn to workouts.

“You can’t just drag along with people not covering payments,” Underdahl said. “It’s possible lenders would prefer to work out an extension or restructure as opposed to taking a loss.”

The hope among lenders is that interest rates dip sometime next year, allowing borrowers to refinance at lower rates or purchase cheaper rate caps.

As of Dec. 1, federal funds futures — a measure of where the Federal Reserve’s secured overnight financing rate will land — showed investors believe there’s a 45 percent chance of a rate cut at the Fed’s March meeting and a 75 percent chance at its April 30-May 1 meeting, according to Reuters.

Some insiders think the market is being optimistic. Conservative lenders are underwriting as if rates will stay put through 2024 or go slightly higher.

“I frankly do not see that there will be a significant drop in interest rates, but obviously one can hope for it,” Mattli said.

He noted that any substantial dip would have to be brought on by a major recession, a “black swan event” that would freeze credit markets and make it even tougher to secure financing.

But even if interest rates merely ease, the dip may not offer the quick fix on which many lenders and borrowers are banking. Multifamily properties have lost so much value, observers say, that an equity infusion is needed to right their debt. Lower rates reduce debt service but they don’t create capital.

Block’s predictions for Blackstone Mortgage spotlights that lose-lose scenario.

The short-seller estimated the losses to the Blackstone trust’s $23 billion in loans could reach $2.5 to $4.5 billion even if the Federal Reserve were to lower interest rates, Bloomberg reported.

That means the trust’s equity could be eviscerated. But Blackstone countered that liquidity is at “record levels.”

Read more

Commercial

National

Arbor stock falls after short-seller report

National

Syndicators are sinking. Who’ll make it out alive?

Commercial

National

The Distress Record: Multifamily woes continue for some of the biggest players