We are excited to announce that Jonathan Miller, who has long authored the most authoritative report on the residential real estate market, is partnering with The Real Deal. Below, you’ll find his Housing Notes column, which will now run on our site several times a week. In addition, Miller’s quarterly report for New York City, which he published through Douglas Elliman for more than three decades, will now be “The Real Deal report, prepared by Jonathan Miller.” Miller’s data venture, Streetmatrix, which provides hyperlocal data, will provide statistics to TRD Data subscribers.

— TRD editors

Rebranding a mortgage giant

Years ago, searching for simple marketing terms using URL addresses was a thing. URLs such as Business.com, Hot.com, Cars.com, LasVegas.com, Insurance.com and Hotels.com all come to mind. Remember when the URL Toys.com was won at auction by Toys ‘R Us? What a get! By now, I thought that the URL marketing era was way over. Apparently, I missed this rebranding tidbit: back in 2024, the Chicago-based mortgage company Guaranteed Rate rebranded to Rate. The year before the rebranding, Guaranteed Rate, which originated nearly $22 billion in volume, was the ninth-largest U.S. mortgage lender. But the rebranding may have worked as they were the seventh-largest U.S. mortgage lender in 2025.

Apparently, it was an AI play as captured by Housingwire in 2024:

“Today, we’re rebranding as Rate,” the company posted on LinkedIn. “Just like our streamlined name, we’re committed to making the mortgage process smoother, faster and smarter, using AI to empower both customers and loan officers alike. It’s more than a new name. It’s a new era.”

Analyses of AI in the mortgage industry can drive a 10–50 percent increase in origination volume by enabling staff to handle more loans, close faster and expand capacity without proportional growth in headcount. Having been through the massive paperwork nightmare of obtaining mortgages for purchases and refinances, I can see tremendous AI upside in any industry built on pushing a lot of paper.

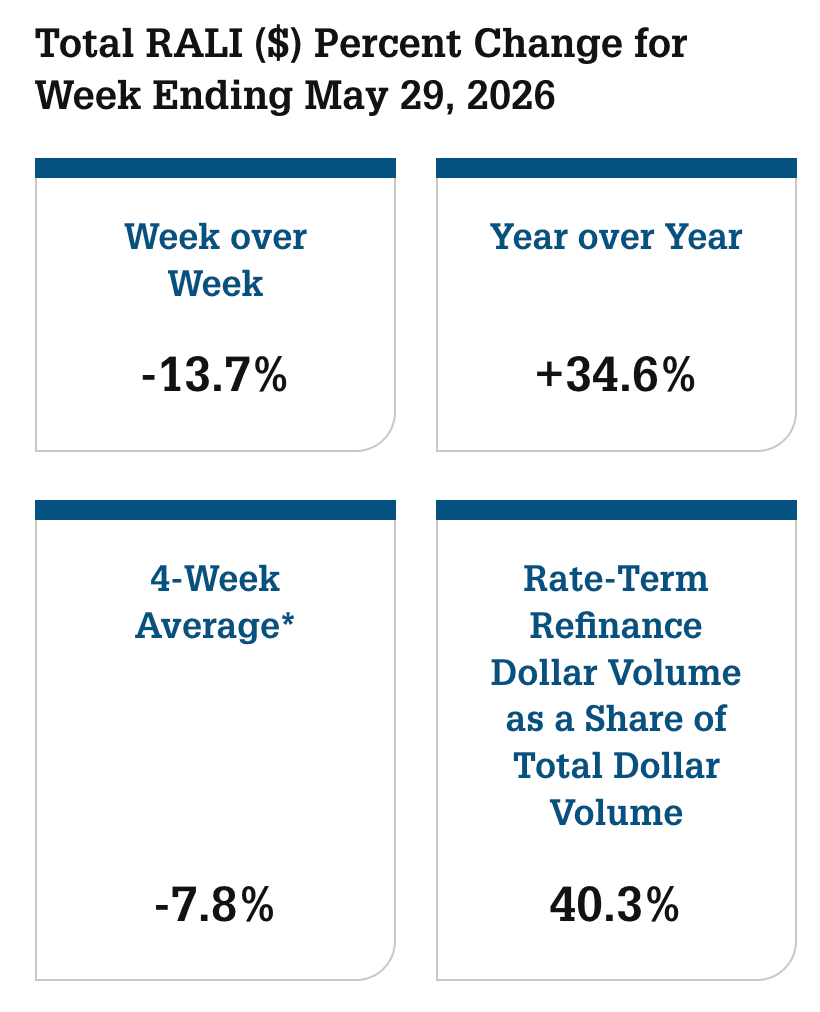

Residential mortgage volume rising from last year is less certain for 2026

Before the Iran conflict began on February 28th, forecasts from the Mortgage Bankers Association (MBA) and the GSEs projected higher dollar volume and more units in 2026 than in 2025, driven by a slight uptick in home sales volume and a rebound in refis from extremely depressed levels. Remember that just before the Iran war began, mortgage rates fell just below the 6 percent threshold, and Wall Street was forecasting as many as two Fed rate cuts during the year.

Source: Fannie Mae

But that entire mindset ended once the war began. Since February 28th, 30‑year mortgage rates have climbed into the mid‑6 percent range, hitting a seven‑month high. National existing- and new-home sales are running well below pre‑pandemic norms, even after the modest pickup in late 2025 and early 2026. Yet higher mortgage volume was driven more by growth in refinance activity than by growth in purchase mortgages, with volume up 30-35 percent annually.

The reason for the surge in refinance growth as a percentage was the collapse of refinance mortgage volume when the Fed pivoted from 2022 to 2025. With 2025 being a low base year, even a small absolute increase in qualifying borrowers or lender push can create 20–40 percent year‑over‑year growth in refi applications, which is what Fannie Mae’s RALI is showing for late May 2026. I always think of a low base year, as when I describe moving from one sale to two sales, it is a 100 percent increase, but it is still only one sale.

Purchase mortgage volume is running modestly above year-ago levels despite higher mortgage rates, but pales in comparison to the change in refinance activity. Going forward, I’m betting that there will be a reduction in the inflationary impact of the tariffs after their implementation was ruled unconstitutional, and that the White House will eventually lose interest in keeping them as a national policy.

My base case remains that 2026 total mortgage volume will slightly exceed 2025, but overall volume expectations are lower than pre-Iran war due to rising mortgage rates. Also, the tail risk of a flat or down year has increased significantly.

‘Rate’ branding now extends to athleisure clothing

THOUGHT: If mortgage rates are rising and anticipated mortgage industry volume is lower than expected, perhaps it is time to diversify the business model? Rate’s rebranding seemed to work back in 2024, so why not have a mortgage company launch a clothing brand in 2026?

In today’s world, there is a clear blurring of reality and fiction in new stories. Many news headlines read like Onion articles, so my initial reaction when a friend of mine shared this X/Twitter post was “no way!”

When this tweet came to my attention, I immediately thought of the following meme and all the hundreds of variations that have been shared with me.

And then I thought of an extreme example, in which Allbirds, a former hot shoe maker, became an AI company overnight.

But the extension of Rate’s brand to clothing is actually true. Even the wording in the press release seems to position them to eventually offer more clothing options beyond athleisure. Here’s the Business Insider press release from June 1st.

Final thoughts

Rate’s rebrand and AI push helped it climb slightly in market rank, but the bigger story is a weaker 2026 outlook as higher mortgage rates weigh on demand. The apparent surge in refinancing is misleading, driven mostly by comparison to a very weak 2025 rather than real strength. In response to this uncertainty, Rate’s move into clothing reflects a broader shift at risk of a The Onion-style headline, that a large U.S. mortgage lender explored a new revenue stream to operate more like a consumer brand, perhaps as traditional loan volume becomes less reliable.

Life is becoming an Onion headline.

The actual final thought — NSFW thoughts about college grade inflation.

Read more Housing Notes columns and sign up for email newsletters here.

Read more

Development

Chicago

White Sox open to making The 78 a two-stadium megadevelopment

Residential

Chicago

@properties top brass express support for Guaranteed Rate CEO amid scandal