We are excited to announce that Jonathan Miller, who has long authored the most authoritative report on the residential real estate market, is partnering with The Real Deal. Below, you’ll find his Housing Notes column, which will now run on our site several times a week. In addition, Miller’s quarterly report for New York City, which he published through Douglas Elliman for more than three decades, will now be “The Real Deal report, prepared by Jonathan Miller.” Miller’s data venture, Streetmatrix, which provides hyperlocal data, will provide statistics to TRD Data subscribers.

— TRD editors

Pretend the FTC is a neutral regulator

It’s been widely reported that Compass, the largest real estate brokerage in the world by agent count and volume, dodged a regulatory bullet (avoiding an extensive antitrust investigation) and got its merger with Anywhere effectively rubber-stamped for approval. Compass hired an attorney known to the White House who would help crush any regulatory merger inquiry.

Mike Davis, known for his efforts to get conservative judges seated on the federal bench, is helping make their pitch. Davis has become a sought-after adviser to companies with deals facing government review. He helped Compass make its case to (Todd) Blanche’s office.

Back in January, The Wall Street Journal broke the story of how Compass circumvented antitrust scrutiny of the merger. Gail Slater, the head of the Justice Department’s antitrust division, wanted to review the merger but was blocked. Attorney General Pam Bondi ultimately fired two antitrust officials under Slater. This was a sad day for a competitive business environment, but a heck of a scoop by WSJ.

After the Compass-Anywhere deal was cleared, a group of members of Congress sent a letter to the Attorney General criticizing the approval as having occurred under “extraordinarily questionable circumstances,” indicating political concern that the review may have been too lenient or rushed.

FTC merger guidelines ignored for Compass-Anywhere

Using the Federal Trade Commission (FTC)’s “Merger Guidelines [2023]” for the Compass-Anywhere merger.

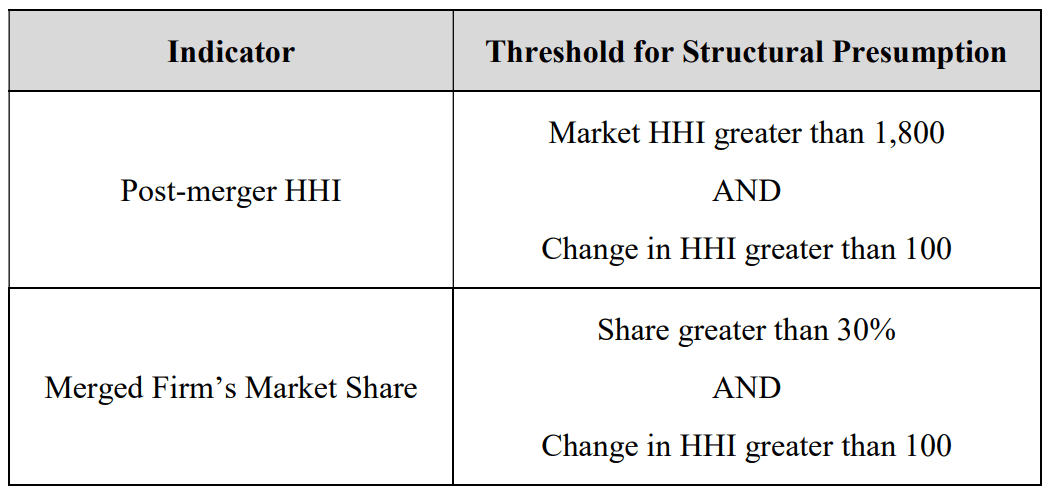

The FTC relies on two indicators to measure merger risk. The one I understand is the market share sales volume threshold that raises a red flag if the newly merged entity (Compass-Anywhere) has a sales volume market share at or above 30 percent, which would make the merger illegal. Nationwide, their market share has been reported at almost 20 percent, well below the allowed threshold, but higher in some large submarkets, according to Capitol Forum, an independent intelligence platform on regulatory risk.

Market concentration and the change in concentration due to the merger are often useful indicators of a merger’s risk of substantially lessening competition. In highly concentrated markets, a merger that eliminates a significant competitor creates significant risk that the merger may substantially lessen competition or tend to create a monopoly.

The second indicator is the Herfindahl-Hirschman Index (HHI), defined as the sum of the squares of market shares. The index is small when there are many small firms and grows larger as the market becomes more concentrated, reaching 10,000 in a market with a single firm. Markets with an HHI greater than 1,800 are highly concentrated. I don’t know what the Compass score is for HHI.

FTC’s “Merger Guidelines [2023]”

Why the New York AG is looking at Compass antitrust issues

The Real Deal broke the story: NY AG probing Compass over antitrust concerns: Authorities contacted top New York City brokerage leaders. Not surprisingly, given the largess of the Compass-Anywhere merger and its bypass of the extensive federal scrutiny expected, Compass is being investigated for possible antitrust violations by the New York State Attorney General. This is likely due to its outsized market share dominance in some locations, such as Manhattan.

The dominance has been confirmed. Housingwire reported that, according to the RealTrends Verified data, Compass has more than an 80 percent market share in both Newport Beach, California and Manhattan. The analysis indicates that Compass-Anywhere:

market share concentrations “well above presumptively illegal thresholds,” in at least a dozen states.

The Capitol Forum’s analysis of the data showed that Compass would control 30 percent or more of local brokerage markets across the U.S., making its market coverage of these cities illegal:

- Los Angeles: 40 percent

- Raleigh: 46 percent

- Houston: More than 50 percent

- Austin: More than 50 percent

- Honolulu: 54 percent

- Seattle: 57 percent

- Denver: 60 percent

- Boulder: 60 percent

- Brooklyn: Over 60 percent

- Washington D.C.: Over 60 percent

- Boston: Over 60 percent

- San Francisco: 64-65 percent

- Nashville: Close to 70 percent

- Newport Beach, California: Over 80 percent

- Manhattan: Over 80 percent

Who cares about a real estate monopoly? We should care

Everyone in the residential real estate industry should care about this current situation, and using critical thinking is required. The consumer should care because Compass’ market dominance in these locations may result in higher commissions, limited access to listings and more double-ending and double-dipping on deals (two Compass executives have denied this to me directly) and a healthy application of the law of unintended consequences. Double-dipping and double-ending are misaligned with market dynamics because they amplify exactly the things policymakers, regulators and serious market participants are trying to fix: excess costs for consumers, conflicts of interest and clarity about how brokerage value is delivered. The federal antitrust regulators were stopped by the Department of Justice from analyzing this deal and blocking needed corrective action in some of the markets this company dominates.

REBNY in the hot seat using “what if?”

While I have no firsthand knowledge of any post-merger concerns between Compass and REBNY, the real estate world now looks very different after a new national monopoly has been established. Let’s explore.

There is no love lost between the Real Estate Board of New York (REBNY) and Compass.

Back in 2021, REBNY fined Compass $250,000 for “repeated violations” of the REBNY’s universal co-brokerage agreement (UCBA), and even briefly suspended the firm from the RLS before a panel converted the suspension into a monetary penalty plus mandatory management training. REBNY’s email to members cited Compass’ targeting of competitors’ exclusives, including encouraging agents to have sellers “disavow” existing exclusive agreements so the listings could be moved to Compass.

Compass then sued REBNY, alleging that it worked with traditional brokerages to stifle upstart competitors by making it harder for agents to take clients with them when switching firms, thereby protecting the status quo. The case hung around in federal court, with some antitrust claims dismissed and others, focused on REBNY’s client‑retention rules, allowed to proceed as potentially anticompetitive. Meanwhile, Compass’ growth and its acquisition of Anywhere have triggered antitrust scrutiny from the New York Attorney General.

Final thoughts

With the inclusion of Anywhere, Compass has an 80 percent market share of Manhattan’s real estate brokerage business, which is REBNY’s home turf. That is an excessively high market share for any business to have over the market it serves (it is ±2.5 times the FTC’s legal threshold of 30 percent).

For REBNY, the mission is to preserve control over the rules and data infrastructure, while for Compass, those same rules limit its monopoly playbook of aggressive recruiting, private listing management, and all the things a firm can do in a market it dominates beyond the legal limit.

What happens to REBNY if Compass quits REBNY?

I would think that after losing a residential firm that accounts for 80 percent of the market volume, REBNY would have to abandon residential real estate and focus exclusively on commercial real estate, especially in its lobbying efforts, an area where it has been particularly effective. Looking through the lens of this market reality highlights why monopolies in any industry are bad for everyone but the shareholders.

The actual final thought — When your pipes burst.

Read more Housing Notes columns and sign up for email newsletters here.

Read more

Residential

New York

NY AG probing Compass over antitrust concerns

Residential

New York

What the NY AG’s antitrust investigation could mean for Compass