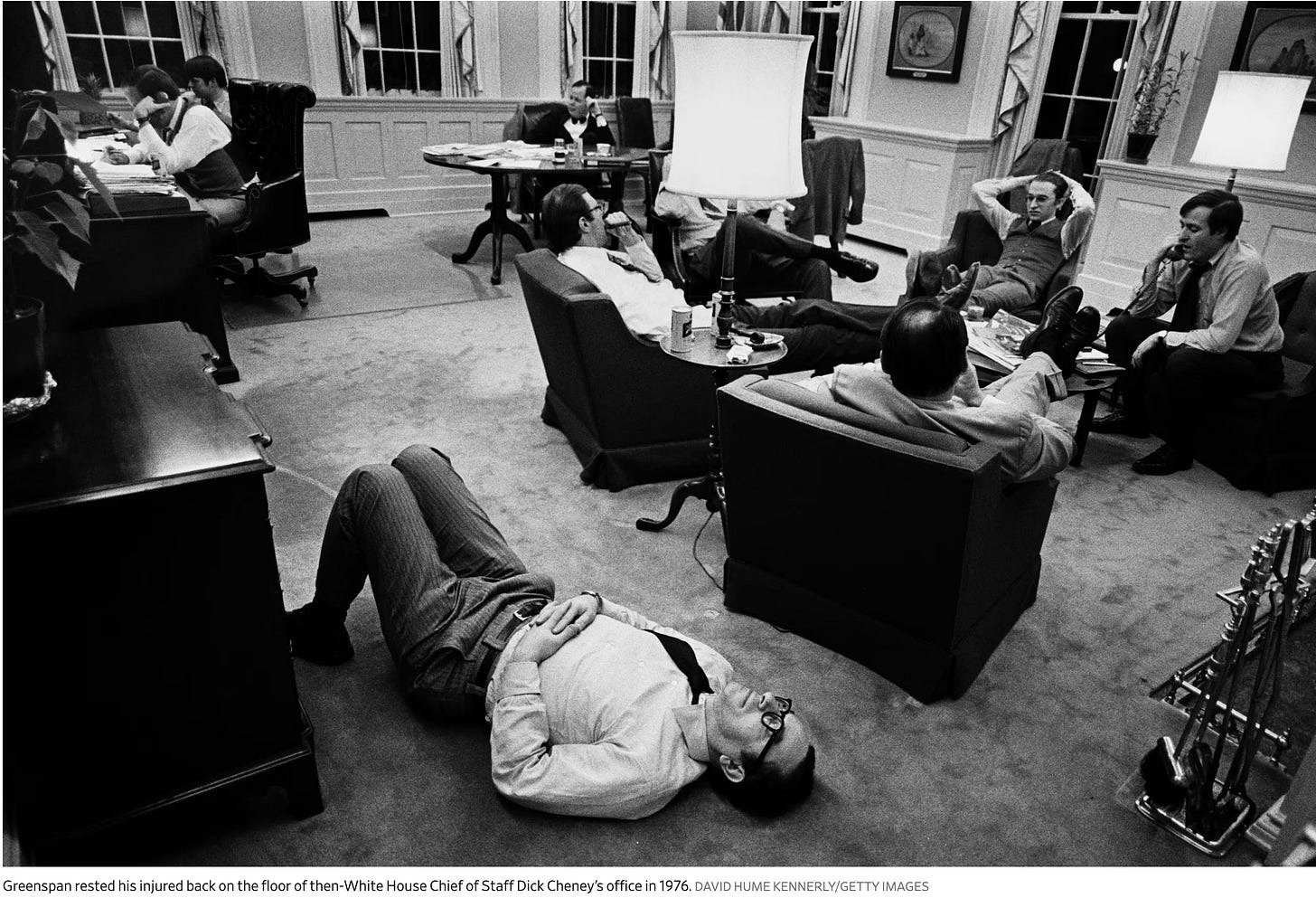

Former Federal Reserve Chairman Alan Greenspan just passed away at 100 years old. He served as Fed Chair from 1987 to 2006, riding through the late-1980s financial market crash, the 1990s economic expansion, the dot-com bubble, and the early-2000s recession. There is a great reflective piece on his legacy in the Wall Street Journal, “Greenspan Left a Lasting Mark on America — and Me”, that I really enjoyed. He severely injured his back in the early 1970s and famously wrote all his speeches in longhand while soaking in the bathtub as therapy.

Source: WSJ

In 2018, I did an in-person Squawk Box hit on CNBC in their Times Square studio with Andrew Ross Sorkin and Robert Frank. One of the things I have to remember when being interviewed on CNBC or on Bloomberg is that viewers are looking to trade on the information being shared. I had just released research on the Manhattan real estate market and recall it was looking weak at the time. The Sorkin interview focused on pricing, which reminded me of the stock-market-like thinking behind the housing bubble of the decade before. Sorkin asks:

“Should all New Jersey homeowners move to Florida?”

After my interview, I remember going to the makeup area, seeing former Fed chair Alan Greenspan climb into a seat to get prepped for his hit. He was in his early 90s at the time and could hardly stand up, plagued with severe back problems for seemingly much of his adult life. As everyone in the room rushed to help him climb into the chair, he pushed them away, not wanting assistance. One of the world’s most powerful financial regulators needed no help. I watched the nearest television for his hit, and it was sharp, defying a body that thought otherwise.

The federal funds rate is the interest rate banks charge each other for very short‑term (usually overnight) loans, and the FOMC sets a target range for where that rate should trade. The Fed does not set mortgage rates, but the federal funds rate can influence the direction.

In the WSJ piece on his passing the author said:

Much of economic activity, he believed, was driven by “animal spirits” which can’t be modeled. “Human nature is essentially immutable,” was his constant refrain. People extrapolate the good times too much in booms, and the bad times during busts.

I simply call that “analysis paralysis.”

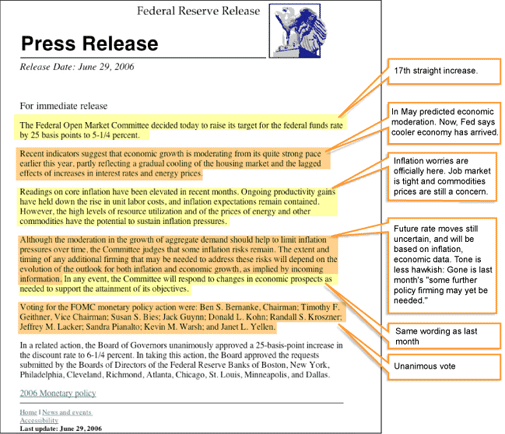

Fedspeak

Alan Greenspan parsed each word in his press releases very carefully, a practice that became known as “Fedspeak.” I began writing blog posts about what he meant, following the Wall Street Journal’s excellent graphical interpretations released after each FOMC meeting. In a “60 Minutes” interview, Greenspan described the process as:

I would engage in some form of syntax destruction which sounded as though I were answering the question, but in fact, had not.

Source: WSJ

The goal of Fedspeak was to manage expectations by preventing the financial markets from front‑running policy changes based on his wording, thereby preserving the impact of actual FOMC decisions when they were announced.

I created a chart for the 1987 start of the Greenspan era, the end in 2006 with his retirement and then up through the modern day.

Rate obsession and lack of underwriting on housing

Alan Greenspan’s policy mix of very low short‑term interest rates, a hands-off regulatory take and public encouragement of complex mortgage products helped fuel the 2000s housing boom, increase leverage and worsen the eventual bust, even though he later argued the bubble was driven mainly by global long‑term rates outside the Fed’s control.

Cheap short‑term money pushed down borrowing costs and mortgage rates, especially for ARMs and hybrid products, which in turn fueled a surge in purchase and refinance activity. Between 2000 and 2006, national home prices climbed by roughly 80 percent as easy credit, speculative demand and few underwriting standards magnified the impact of low rates. I still quip that the era of mortgage lending standards required that borrowers needed to either have a pulse or be able to fog a mirror, and sometimes even those requirements were waived.

In this environment, lenders freely originated high‑LTV, low‑doc, and subprime loans and quickly securitized them (liar loans), while the Fed largely refrained from tightening standards. Greenspan would spend the rest of his career trying to explain how the housing bubble was not his fault.

This became known as the “Greenspan put,” convincing investors the Fed would backstop major asset‑price declines and thereby encouraging greater risk‑taking in housing and related securities.

During this era, it was clear that our firm’s banking clients were slowly losing their minds as all kinds of exotic mortgage products sprang up due to the lack of federal oversight.

Final thoughts

I’ve long said that we over-obsess about interest rates, and ultimately, mortgage rates for housing. Alan Greenspan helped cement interest rates, especially the federal funds rate, as the headline gauge of monetary policy. I believe this caused the broader over‑emphasis on rates as “the economy’s health meter”

The lack of regulatory oversight broke the proverbial back of the U.S. housing market, which I believe we are still living with its distortion.

The actual final thought — Take note of the sunset in Manhattan.

Read more Housing Notes columns and sign up for email newsletters here.