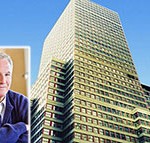

Six months after Shorenstein Realty Investors defaulted on the $350 million loan backed by its ground lease at 1407 Broadway, the debt’s special servicer has filed to foreclose.

The Bay Area-based investment firm quit paying interest on the CMBS loan late last summer, a few months before the Garment District office tower loan was set to come due, according to a complaint filed Friday.

Shorenstein had twice pushed back its maturity date on the floating-rate loan and had one more extension available. The default likely took that option off the table. In November, the loan landed in maturity default.

Shorenstein tried to hammer out a modification in the months following the default, servicer commentary shows. In December, it sent a workout proposal to lender Barclays and by February, Barclays had responded with a counter-proposal.

It’s unclear whether negotiations are still underway. At times, lenders and special servicers will pursue foreclosure while proceeding with modification talks.

A representative for the firm declined to comment.

Rising rates likely drove the fallout. Shorenstein took out the debt in late 2019 at a 3.4 percent interest rate. By the time the firm missed its interest payment, the federal funds rate had surged by 5.25 percentage points.

Occupancy may have pressured revenue, too. At the end of 2022, 16 percent of 1407 Broadway was vacant, according to the most recent data from Morningstar.

Shorenstein has at least three problem offices on its hands.

Around the same time it quit paying interest at 1407 Broadway, the borrower asked that two of its Philadelphia office properties, 1700 and 1818 Market, be transferred to special servicing to “engage in loan modification discussions,” according to Morningstar.

Philadelphia’s “beat up” office market has failed to recover from the pandemic, a CBRE report found last year.

Read more

Commercial

New York

Shorenstein falls behind on 1M sf Garment District office tower

New York

Shorenstein to buy 1407 Broadway ground lease for $330M

Commercial

New York

Savanna hands Harlem office building back to lender