Developers might not know that in New York City from 2019 to 2023, the lowest-paid workers’ pay rose 6 percent while the highest-paid workers’ pay shot up 18 percent, according to a new study reported by The City.

But this trend helps explain the shift in strategy by Brooklyn house-flippers Carlos Saavedra and Nicole Eckstrom, the husband-and-wife team behind development firm Eckstrom NYC.

As The Real Deal’s Jake Indursky wrote, the couple started by turning row houses in Bedford-Stuyvesant into condos. Their first project, in 2016, was buying 541 Madison Street for $1.3 million and creating four $850,000 units.

But construction and financing costs eroded the margins on those projects, so Eckstrom pivoted to single-family homes, which proved more profitable. Single-family homes only need one kitchen so construction costs less, but another factor is that the income gap between the 1 percent and everyone else has grown recently in New York. (In the rest of the nation, lower earners’ gains were greater.)

“I don’t think we would be able to continue doing condominiums if we didn’t have the profits from one-families,” Saavedra told TRD.

This is unusual. Most products cost less when they are purchased in bulk. Compare 30-packs of toilet paper to 4-packs, and 2-liter bottles of soda to 8-ounce cans.

But large New York City homes often cost more per square foot than smaller ones. A major reason is the tremendous wealth and purchasing power of high-end buyers in New York City. Just one can effectively outpay four upper-middle-class buyers.

That’s why Eckstrom could price its single-family renovation at 170 Clinton Street at $14 million. The home is in contract. Carving it into four apartments would have cost more and sold for less.

“I’m still surprised how fast we sold 170 Clinton, and the price that we got for it,” Saavedra said. “The very first time we did it, I was like, ‘Oh, maybe we’re lucky,’ but not anymore.”

It’s definitely not luck. It’s math.

What we’re thinking about: The wealth gap in New York City contributes to the housing shortage by making larger homes more profitable than smaller ones. Should policymakers try to close the wealth gap? Or incentivize four-family projects to make them more competitive with mansion renovations? Send your ideas to eengquist@therealdeal.com.

A thing we’ve learned: The phrase “jumped the shark” was coined in 1985 by radio personality Jon Hein in response to a 1977 episode of the sitcom “Happy Days,” in which Fonzie, on water skis, jumps over a live shark.

Elsewhere…

— New York City’s water rates just went up 8.5 percent, but would have risen only 5.4 percent if the Adams administration had not reinstated rental payments from the Water Board to the city, according to an analysis by the Independent Budget Office. The $325 million average annual rent goes into the city’s general fund and is not used to provide water service. Rent was charged from 1985 through 2015, when the de Blasio administration suspended it after complaints from property owners and advocates.

— Readers had a lot to say about what would happen if New York rolled back rent control the way Argentina did. Most predicted similar results, but the New York Apartment Association’s response was tempered:

“Comparing New York City to Argentina is a little bit of apples to oranges, because New York City has much higher operating costs, including property taxes and high water and sewer costs that are controlled by the government. Easing rent regulation would definitely create more supply and that would lead to lower rents for many, but we wouldn’t see the type of sea change that Argentina has seen.”

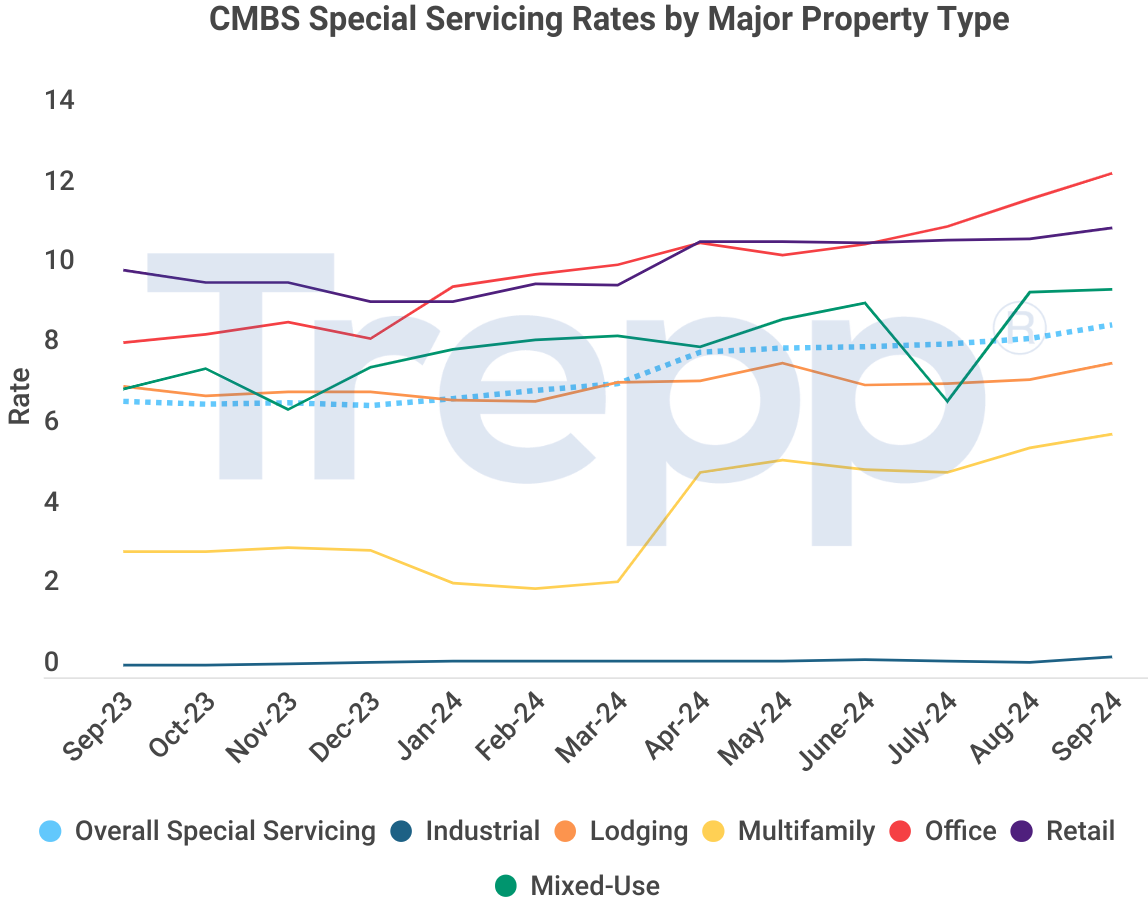

— A year ago, CMBS loans on retail were the most likely to go into special servicing (an indication that borrowers were struggling to repay them). No. 2 on the distress list, with a rate about 25 percent lower, were office loans. But now the office-loan special servicing rate is No. 1, about 10 percent higher than for retail CMBS.

The chart below by Trepp breaks it down. In September 2023, about 10 percent of retail CMBS financing was in special servicing, versus 8 percent of office CMBS. Last month, the office rate was 12.6 percent versus 11.2 percent for retail.

Closing time

Residential: The priciest residential sale Friday was $9.4 million for 1981 East 2nd Street in Brooklyn. The Gravesend single-family home, whose buyer just sold a $9.5 million home blocks away, is two stories and approximately 1,800 square feet. The last sale on the property was in 1999 for $4.9 million, property records show.

Commercial: The largest commercial sale of the day was $20 million for a Holiday Inn Express at 833 39th Street in Sunset Park. W&L Group sold the property to CH Associates XII.New to the Market: The highest price for a residential property hitting the market was $29.1 million for Unit PH44/46TER at 180 East 88th Street. The listing covers three different units that total 8,600 square feet. The Upper East Side condo is a new development, with Corcoran Sunshine Marketing Group representing the listing.

New to the market: The highest price for a residential property hitting the market was $29.1 million for Unit PH44/46TER at 180 East 88th Street. The listing covers three different units that total 8,600 square feet. The Upper East Side condo is a new development, with Corcoran Sunshine Marketing Group representing the listing. — Joseph Jungermann