Take the luxury-sports-car view of household wealth.

For roughly 10 years, I had a used, triple-black midlife crisis Porsche Boxster S convertible that brought me hours of joy but was admittedly pedestrian in the luxury sports-car world. I’m going to use a real sports car in the application of a proper analogy of the surge in household wealth. I’ll explain.

This weekend we stayed with friends in the Hamptons (on eastern Long Island), largely a second home luxury market east of New York City, and took a tour of all the homebuilding going on out there and believe me it looks a lot better from the passenger seat of a 1988 Porsche 911 Carrera with the M491 “Turbo Look” option, running the stock G50 5‑speed, whose original 3.2 flat‑six has been rebuilt and enlarged to 3.4 liters. (translation: it’s quick and hugs the road). Yet I didn’t see a single Porsche Boxster S all weekend. The sheer number of luxury cars and high-performance sports cars, along with the massive scale of new construction since the pandemic began, is hard to process. Zipping around hamlets such as Westhampton Beach, Westhampton, Quogue, and Hampton Bays, it was fair to suggest that at least 50 percent of the housing stock has been either significantly upgraded or torn down and replaced with homes two-to-three times larger since the lockdown. How is the vast scale of this new construction even sustainable? Then consider the perfect moment of high compensation for Wall Street, set alongside the surge in household wealth since the pandemic began and the dominance of cash buyers.

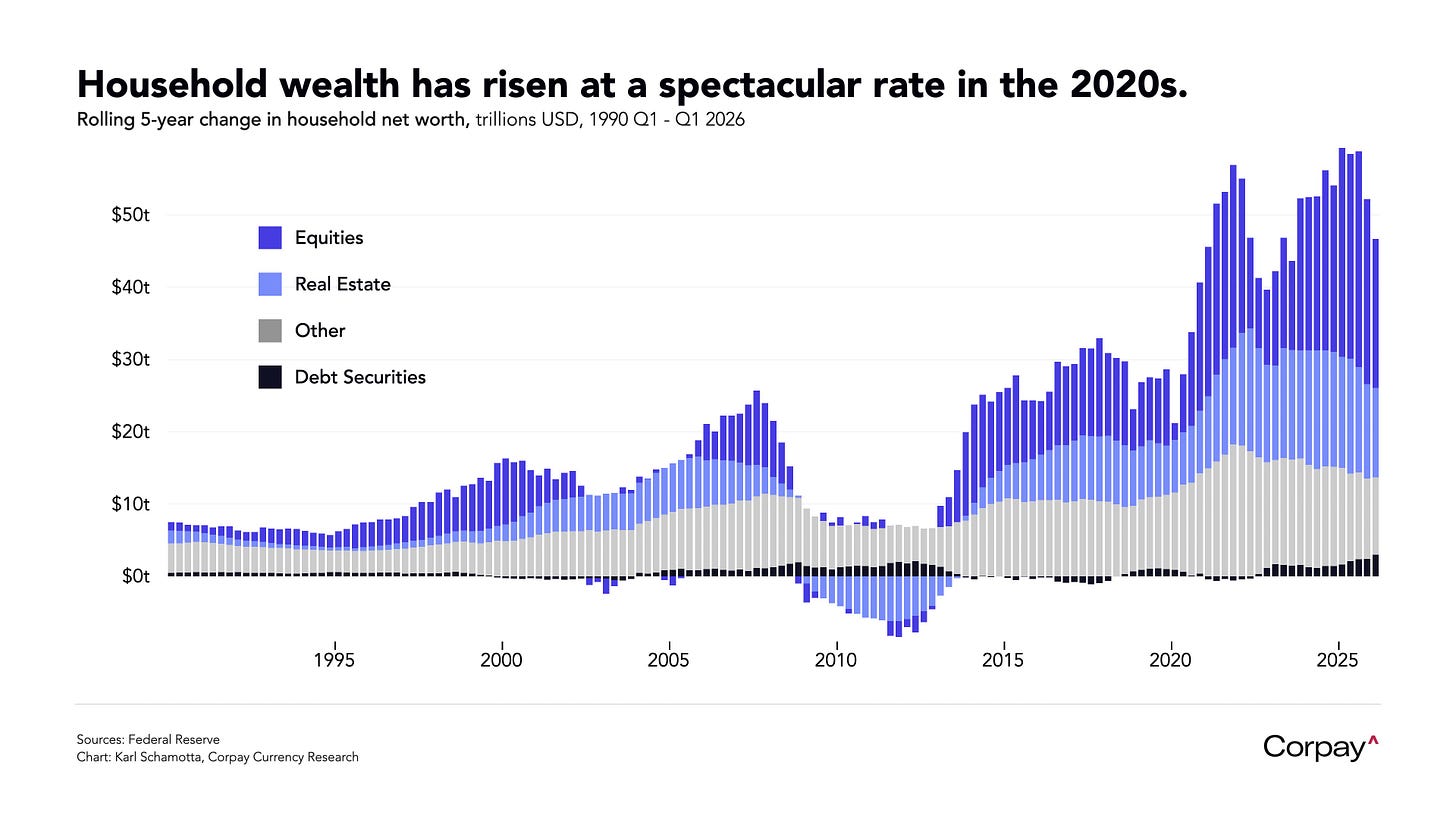

But why did household wealth rise so much?

Both the financial markets and real estate have contributed significantly to the explosion of household wealth since the pre-pandemic era, on a scale not experienced before.

This surge in wealth, expressed through the housing stock (and sports cars), is clearly Wall Street-related, as explained in my first-quarter Hamptons market analysis, but it is not the only driver of this market.

The pandemic-era surge in household wealth was driven by an unusual combination of forced saving and a massive asset-price boom in housing and equities, all layered atop inequality that has been expanding for years worldwide. An interesting snippet from the IMF back in 2021, as we exited the dark days of Covid:

Household saving increased sharply during the COVID-19 crisis in many countries. Lower consumption, both as a result of lockdowns or precaution, combined with an increase in disposable income from government transfers allowed households to put more money into their bank accounts, buy shares, a house, or pay back their debt. Along with saving, surging equity and housing prices also made certain households a lot wealthier.

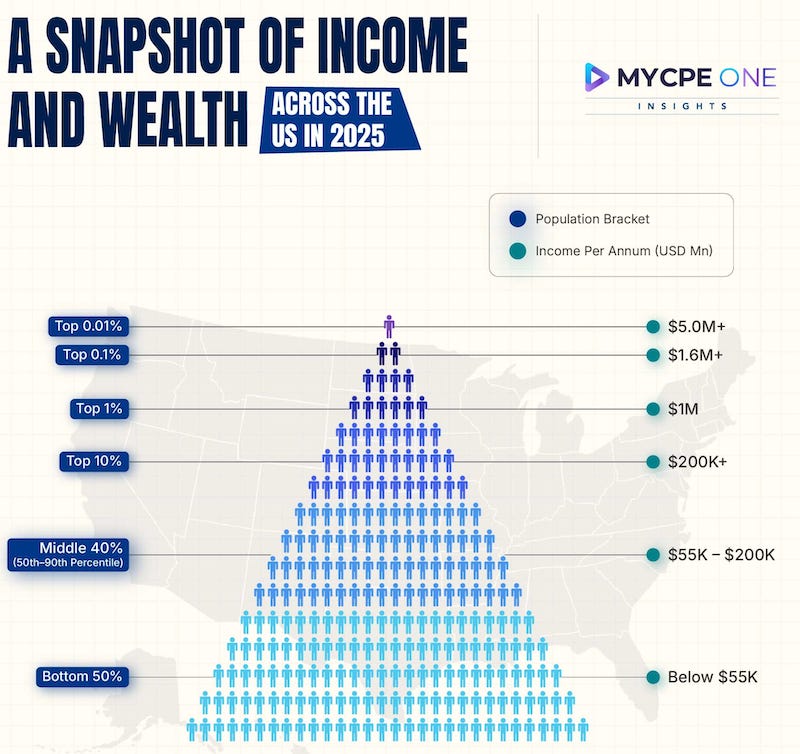

Household metrics of the top 0.1 percent

The top 0.01 percent of the wealth distribution accounts for nearly 140,000 U.S. households, who, according to the Fed, each have a net worth of nearly $190,000,000. The wealth of the overall population has expanded by about 8x since 1989, while the top 0.1 percent has increased more than 13x, illustrating just how much faster the .01% group’s assets have grown than the remainder.

Beyond the income itself, what is most interesting about this analysis is that their wealth is growing much faster than the number of individuals. In fact, over the last few decades, the top 0.1 percent have gained wealth faster than the top 1 percent overall, which in turn have gained faster than the top 10 percent, while both have outpaced the middle 50–90 percent and the bottom 50 percent in relative terms. The history that forms this pattern makes me think it won’t end anytime soon.

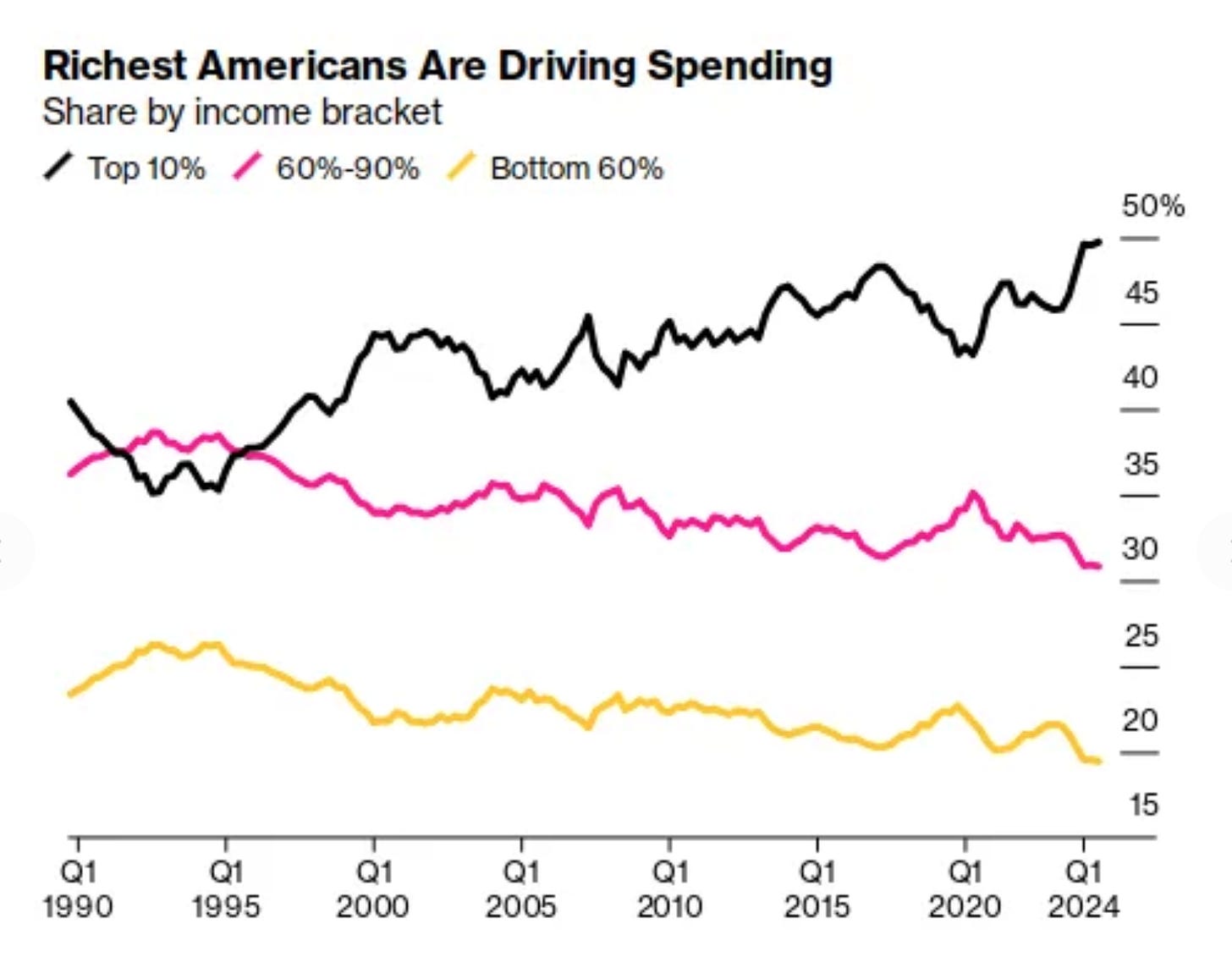

Note the use of the word “driving” here.

Source: Bloomberg

Final thoughts

There was a structural shift in housing, in which the top end functions more as a luxury asset than as shelter, with rapid teardown cycles and upsizing resetting market norms. It also reflects a decoupling from local fundamentals, as cash-heavy, finance-driven buyers sustain demand and reduce sensitivity to interest rates, potentially prolonging the cycle.

The actual final thought — A form of resiliency for retail you’d never expect.

Read more Housing Notes columns and sign up for email newsletters here.

Read more

Commercial

New York

Housing Notes: Wall Street is adding more finance jobs to NYC than anywhere else

Development

New York

Luxury new development deals climb to 10-year high