When Westbury’s Westwood Village Apartments and six other multifamily properties hit the Long Island market last year, 15 bidders submitted offers.

The portfolio’s “durable and reliable cash flow” was a big draw, said CBRE vice chair Jeffrey Dunne, who along with a team of colleagues represented the seller, a unit of Dallas-based Lone Star Funds.

Dunne, whose capital markets group focuses on the Tri-State area, said the ability to improve amenities and interiors offered investors enough potential for appreciation to justify paying a premium. Fairfield Properties, which controls a multifamily portfolio across Long Island, ultimately won out in a competition that set a record.

The Melville-based firm paid $472.5 million in March to acquire 1,496 units in the seven-property portfolio spread across Nassau and Suffolk counties, by far the largest transaction in The Real Deal’s ranking of the biggest Long Island multifamily deals between April 1, 2018, and March 31, 2019. The acquisition by Fairfield also represented the largest apartment trade in Long Island history.

Fairfield agreed to shell out about $315,842 per unit for the former Lone Star portfolio. The company invested $100 million in preferred equity and received financing from Citigroup and Freddie Mac for the transaction. It was the largest deal ever undertaken by Fairfield, which is led by Gary and his nephew Michael Broxmeyer.

Besides the 242-unit Westwood Village, other Class B assets included in the deal were the Mid-Island Apartments in Bay Shore (232 units), Southern Meadows (452 units) in Bayport, Heritage Square (80 units) in East Meadow, Lake Grove Apartments (368 units) in Lake Grove and Cambridge Village (82 units) and Yorkshire Village (40 units) in Levittown.

“It had a good history,” Dunne said of the portfolio. “Tenants like it. Tenants stay. It checks a lot of boxes for people.”

High demand, rising rents

Long held out as the epitome of single-family suburban life, Long Island has become more accepting in recent years of multifamily development. A number of factors are currently driving activity in the region’s multifamily market.

On a national level, private equity real estate funds have been aggressively moving into the multifamily sector, with residential properties making up 22 percent of deal value for such funds — the largest share in recent years, according to a private equity real estate analysis released in May by accounting firm EisnerAmper. Between 2017 and 2018, EisnerAmper found, residential deal value for such funds rose to $72 billion from $60 billion.

Some private equity fund managers have cautioned that the multifamily residential sector has reached its peak and could be ready for a looming correction. EisnerAmper’s report, however, noted that if “property valuations do begin to fall… real estate deal activity may continue at record levels as fund managers look to deploy capital against a new dynamic.”

“Space is limited out here,” said Lisa Knee, the New York-based co-chair of EisnerAmper’s national real estate practice. “We run into the water at some point. The units that are here are in high demand.”

On Long Island, single-family homes remain pricey, and there are relatively few alternatives. The median closing price on Long Island homes was $455,000 in April, a 3.4 percent year-over-year increase, according to the Multiple Listing Service of Long Island, which covers Nassau, Suffolk and Queens. The median price in Nassau was $505,000 in April, up 3.1 percent from 2018, while Suffolk had a 5.6 percent increase, to $380,000, per MLSLI data.

Over in the rental market, the vacancy rate on Long Island was just 2.3 percent in the fourth quarter of 2018, according to a market report from real estate services firm NAI. In contrast, the rental vacancy rate across the U.S. was double that last year, at 4.6 percent, JLL said in its most recent national multifamily investment outlook.

(Click to enlarge)

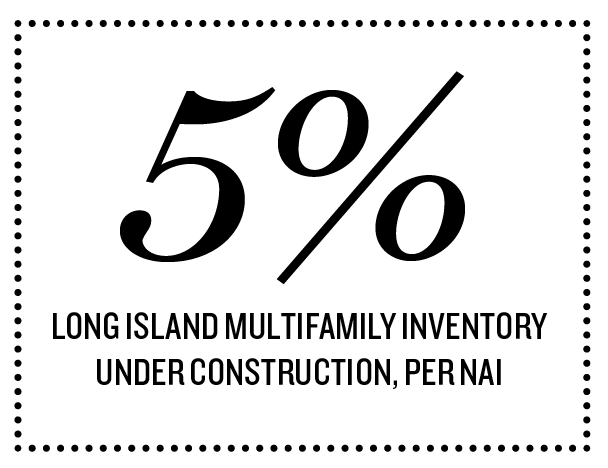

Perhaps not surprisingly, Long Island’s apartment rents have continued to creep up. The average monthly asking rent for the 49,015 multifamily units on Long Island hit $2,180 last year, according to NAI, a result of steady growth of between 3 to 4 percent over the past few years. NAI found that just 5 percent of Long Island’s multifamily inventory is under construction, another sign that tight demand is unlikely to change as investors bet on rents continuing to rise.

At the same time, New York City’s multifamily market has slowed due to concerns about potential changes in rent stabilization laws for the state. In April, New York Assembly Speaker Carl Heastie introduced a series of bills that could rewrite the rules for vacancy decontrol and bonuses, as well as for programs that allow landlords to raise rents based on renovation work tied to major capital improvements and additions to individual apartments.

Investment opportunities

While some multifamily market players are taking a wait-and-see approach before moving ahead with deals involving rent-stabilized units, those firms behind Long Island’s biggest trades of 2018 had no desire to discuss their plans with TRD.

The Broxmeyers behind Fairfield were unavailable for comment — the company’s principals are related to late Long Island real estate mogul Mark Broxmeyer, who once tried to buy Major League Baseball’s Montreal Expos. Their firm has been a repeat buyer in the multifamily space. Fairfield currently owns more than 10,000 apartments in Nassau, Suffolk and Queens.

Before closing on its deal with Lone Star this year, Fairfield put down $15.6 million in 2018 to acquire a 42-unit apartment complex in Farmingdale from Terwilliger & Bartone Properties. That deal, which came in at No. 4 onTRD’s list of top Long Island multifamily trades, marked a quick turnaround for the seller. Terwilliger & Bartone bought the Cornerstone for an undisclosed sum in 2015 before flipping the property to Fairfield last summer.

Before closing on its deal with Lone Star this year, Fairfield put down $15.6 million in 2018 to acquire a 42-unit apartment complex in Farmingdale from Terwilliger & Bartone Properties. That deal, which came in at No. 4 onTRD’s list of top Long Island multifamily trades, marked a quick turnaround for the seller. Terwilliger & Bartone bought the Cornerstone for an undisclosed sum in 2015 before flipping the property to Fairfield last summer.

Fairfield inherited $355,563 in tax exemptions given to the property by the Nassau Industrial Development Agency, including a 20-year payment-in-lieu-of-taxes agreement that kept annual property taxes at $105,000 with a 1.67 percent annual increase. Fairfield is also counting on Cornerstone tenants paying premium monthly rents: A dozen studios are listed for between $2,200 and $2,600, 26 one-bedrooms are asking $2,800, and four two-bedrooms are seeking between $3,200 and $3,400.

“While the market often dictates projects, this fit well into our strategy,” said a Terwilliger & Bartone spokesperson when asked about the sale of Cornerstone to Fairfield. “We were able to transform this area and become a catalyst for redevelopment that has led to enormous interest and success for the project.”

Terwilliger & Bartone is now developing the Cornerstone Hauppauge, a $30 million project that broke ground in September 2018 on a nine-acre parcel near the Long Island Expressway. The 98-unit luxury development designed for renters 55 and over is one of several Long Island projects it has in the works. The Farmingdale-based developer has also embarked on a 50-unit development near a Long Island Rail Road station in Kings Park set to open in 2021, as well as a project in Patchogue, slated to open the same year, that will feature luxury homes near another LIRR station and the ferry to Fire Island.

Other top multifamily trades also had close ties to public transportation. The second-largest transaction onTRD’s list involved the Allure in Mineola, which was one of two buildings sold by J.P. Morgan Asset Management for $150.4 million to San Francisco-based Friedkin Realty Group in a deal facilitated by JLL. It’s two blocks from the village’s LIRR station and in a walkable neighborhood with shops and restaurants.

Friedkin, which did not return a request for comment about the deal, forked over an average $546,909 per unit for the 275 apartments in the five-story property.

Similarly, the New York-based Feil Organization, a family-owned real estate investment and development firm that owns a half-dozen multifamily properties across Long Island, paid $22.8 million in September to buy the Freepark Apartments in Freeport, the third-largest deal onTRD’s list. The property is a two-minute drive from an LIRR station in Freeport, a boating and fishing haven known for its Nautical Mile dining and shopping district, which was recently named one of the “coolest” places in the country to live by travel website the Matador Network.

Westwood Village in Westbury

“People like to be where there’s a hub and a center,” said EisnerAmper’s Knee. “You want to be where there are buses, trains and transportation.”

Changing demographics

Long Island is home to one of the highest percentages of residents aged 65 and older in any of the country’s major markets — and many of them are looking to downsize.

Meanwhile, many of the children and grandchildren of those aging baby boomers, some of whom have found it hard to afford a home on Long Island, are sticking around in the suburbs to compete for scarce rentals. Finding a home for those disparate segments of the population is what some suburban landlords are hoping to capitalize upon by investing in multifamily projects on Long Island.

Garvies Point, a $1 billion development on Glen Cove’s waterfront by Uniondale-based RXR Realty, is scheduled to start leasing this summer on its first phase, which includes 385 apartments. JPMorgan Chase recently retained Cushman & Wakefield to market a 38,544-square-foot lot it owns in Great Neck where luxury rental apartments are planned. And Stamford-based Post Road Group has turned to CBRE to market Hawthorne Court, a 434-unit building in Central Islip, which could attract bids of $95 million, or nearly $220,000 per unit, according to Real Estate Alert.

And while living close to commuting hubs is key, so is cost. A recent survey by nextLI, a project run by Newsday, found that a majority of young adults want to leave Long Island within the next five years for somewhere with a lower cost of living. The challenge for Long Island will be to find apartments for those fleeing the region’s increasingly expensive housing market.

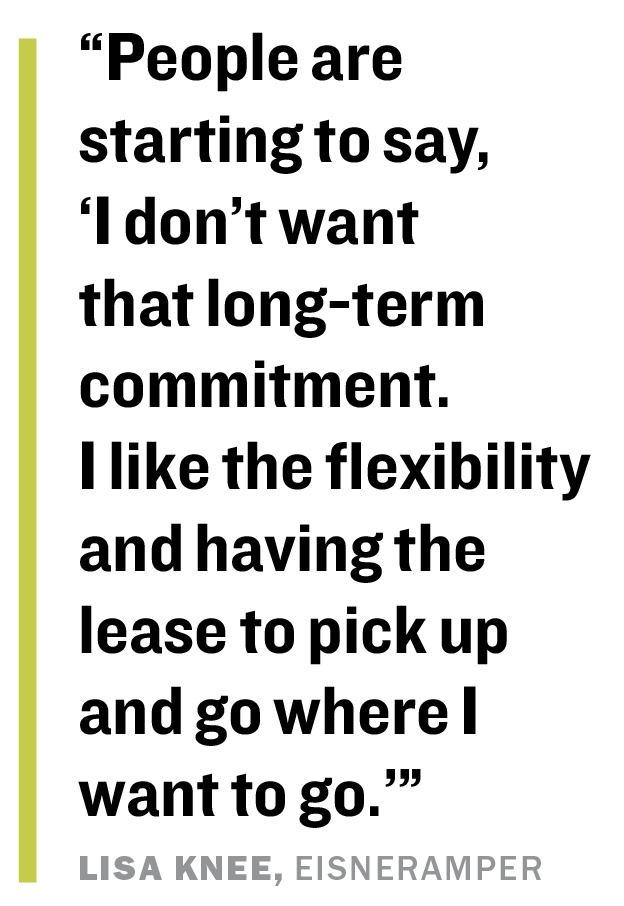

“People are starting to say, ‘I don’t want that long-term commitment,’” Knee said. “‘I like the flexibility and having the lease to pick up and go where I want to go.’”

CORRECTION, 6/6/19: An initial version of this story misstated the relationship between Gary and Michael Broxmeyer.