Trending

Return to lender: 10 malls Brookfield may give up, and why

Firm is in default on over $1B in loans on 5.6M sf across US

It was a gamble when Brookfield Property Partners paid over $9 billion in cash for GGP’s 125-mall portfolio, but the company had a plan. Shortly after the deal closed in August 2018, Brookfield said it would “future proof” most of those malls, turning moribund properties into mixed-use “mini cities” by adding residential and office space.

The future, it turns out, had other plans.

The coronavirus pandemic has battered Brookfield’s massive retail holdings, with its malls among the hardest hit.

Now, with brick-and-mortar stores struggling and debts mounting, 10 Brookfield malls are at risk of being handed over to their lenders, according to a Real Deal analysis of mortgage data from Trepp and rating agency Fitch, and media reports. Those properties are backed by a combined $1.2 billion in loans — nearly all them securitized — and comprise 5.6 million square feet of real estate.

Loan servicer commentary found most of the mortgage payments are over 90 days delinquent. Some of the malls could be handed back to lenders via foreclosure or a deed-in-lieu — when a borrower gives up the property to avoid foreclosure. In other cases, servicers noted Brookfield was not likely to continue funding its loan on the property. Brookfield has already handed the keys to its lender on the Florence Mall in Kentucky, according to Trepp. For its North Point Mall in Georgia — the largest of the 10 on the list — the lender confirmed Brookfield already handed over the title.

The Brookfield malls that either have or are at risk of being turned over to lenders are scattered throughout the country, with several in the South and Midwest. They are:

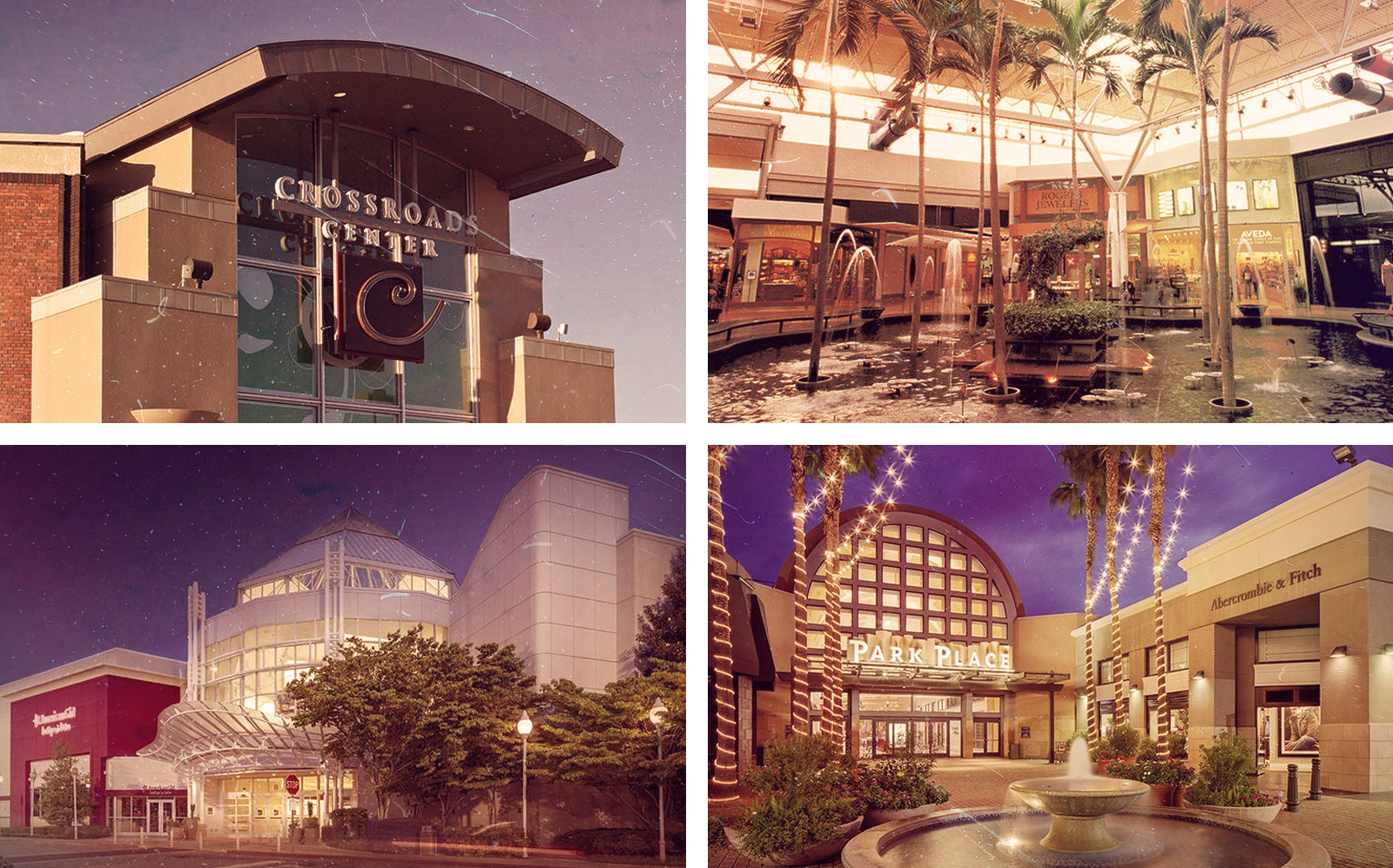

1. North Point Mall | Alpharetta, Georgia | 1.3M sf

2. Crossroads Center | St. Cloud, Minnesota | 766K sf

3. Mall St. Matthews | Louisville, Kentucky | 670K sf

4. RiverTown Crossings | Grandville, Michigan | 636K sf

5. Bayshore Mall | Eureka, California | 516K sf

6. Park Place | Tucson, Arizona | 478K sf

7. Florence Mall | Florence, Kentucky | 384K sf

8. Valley Hills Mall | Hickory, North Carolina | 325K sf

9. Meadows Mall | Las Vegas | 309K sf

10. Pierre Bossier Mall | Bossier City, Louisiana | 265K sf

* The square footage corresponds to the portion of each mall Brookfield owns, except North Point, which notes the entire size of the mall.

The Real Deal has not previously reported on the loan troubles tied to North Point, Crossroads, Bayshore, Valley Hills and Pierre Bossier malls.

At least three other malls that Brookfield partially controls have been in default for months, according to the data. They are: Fox River Mall in Wisconsin, Glenbrook Square Mall in Indiana and Greenwood Mall in Kentucky.

Turning point

While the total number of at-risk malls is just a fraction of Brookfield’s retail holdings — 170 properties and 148 million square feet — the loan troubles come at a critical time.

Just weeks ago, Brookfield Asset Management announced its plan to take private Brookfield Property Partners — its real estate arm — in a deal worth roughly $6 billion at the time. Brookfield Asset Management pitched the move as a way to buy the shares at a discount to their true value.

Brookfield Property Partners declined to comment for this article but like most mall owners, it faced mounting challenges even before the pandemic. Those pressures — namely from e-commerce competition — only intensified over the last year as governments forced mall closures or restrictions and retail tenants like J. Crew, Brooks Brothers and others declared bankruptcy. The trend has had a damaging effect. A new report from Green Street estimated the value of Class A luxury malls has fallen about 45 percent since 2016 levels.

When Brookfield acquired GGP’s 125 Class A malls in 2018, it already owned about a third of the Chicago-based company. Two years earlier, a Brookfield Asset Management fund paid $2.8 billion for Rouse Properties, which owned about 30 Class B malls. Rouse had been spun off from GGP in 2012.

Several of Brookfield’s problem malls were from the Rouse acquisition, including Bayshore Mall in California, Valley Hills Mall in North Carolina and Pierre Bossier Mall in Louisiana.

Brookfield’s grand plan to convert many of its malls into residential or mixed-use properties is still a work in progress but some of those efforts have not worked out. It had made strides with North Point Mall. Brookfield recently handed over the title to lender New York Life Insurance, though in 2019 it scored rezoning approvals to bring hundreds of residential units to the property. And in July, Brookfield ended plans to redevelop a former mall in Burlington, Vermont, claiming it didn’t fit with its strategy.

Trouble ahead

Because of the economic devastation Covid has caused, other major mall owners like Simon Property Group and Starwood Capital Group have also given up on properties, deciding the value of the malls was worth less than the debt.

A number of malls being handed back are financed through commercial mortgage backed securities, and the loans are non-recourse. That means in case of a default, the lender can only go after the mall itself, not the borrower’s other assets.

There will likely be more of that to come, said Manus Clancy, senior managing director at Trepp. He estimates 30 to 40 more malls will be returned to their lenders in the months ahead.

Owners “are already realizing that there is no equity value in the mall,” Clancy said. But he added, “sometimes borrowers have changes of heart … these situations can pivot from one potential outcome to another.”

Dan McNamara, a principal at the hedge fund MP Securitized Credit Partners — whose firm has been betting against mall properties — said mall owners’ move to give up on their properties is often pragmatic, and agrees it may keep happening.

“These guys are smart, savvy investors,” he said. “They are not going to support a CMBS mall that is below the [value of the] mortgage.”

At the company’s third quarter earnings call in November, Brookfield Property Partners CEO Brian Kingston refused to say how many mall properties it would return to lenders. “It’s a relatively small number of assets where we think the debt is in excess of the value of the asset,” he said. The quarter was another miserable one for the firm, which is also one of the biggest office landlords in New York City. Brookfield reported a $135 million net loss, though retail rent collections improved dramatically from the second quarter.

Amid the gloom, Brookfield was able to secure a major refinancing for its Oakbrook Center mall outside Chicago. In October, a Brookfield venture secured a $475 million loan from Morgan Stanley on the 2.2-million-square-foot property. And in December, it negotiated a one-year extension on its roughly $280 million loan for Tysons Galleria Mall in Virginia, according to Commercial Real Estate Direct. The loan had been transferred to special servicing when Brookfield skipped the September deadline to pay it off.

Then there’s the $198 million loan Brookfield has on Park Place Mall in Arizona. According to the servicer note, Brookfield said it no longer intends to support the 478,000-square-foot property “with additional infusions of equity.” It could also send back most of the 895,000-square-foot Crossroads Center mall in Minnesota. That loan was in default and transferred to special servicing in October. Brookfield said it was unwilling to inject “additional funds to support the loan, but is willing to continue to manage the property.”

While the outlook for Brookfield’s mall portfolio is a looming question, Clancy said the company itself will weather the storm. Brookfield is more diversified than other mall owners, he said. “They are going to be fine in the through and through,” and Brookfield’s hobbled malls “won’t present a systemic risk for them.”