On the evening of Dec. 19, roughly 30 of Douglas Elliman’s top executives gathered at Bouley Test Kitchen in the Flatiron District for the residential firm’s annual managers’ party.

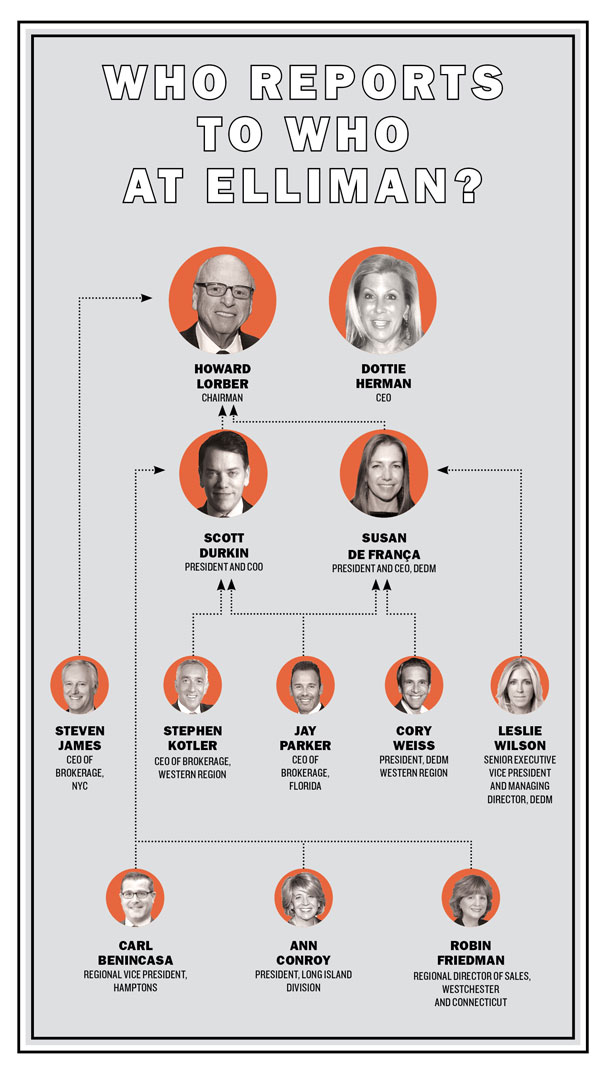

All the firm’s key players were on hand: Chairman Howard Lorber, CEO Dottie Herman, plus newly minted President Scott Durkin and Susan De França, the firm’s hard-charging development chief and rumored successor to Herman.

If there were any residual hurt feelings from the management shake-up two weeks’ earlier, they were not on display that night.

But the firm has been gripped by palace intrigue in recent weeks amid major changes to the C-suite — all while it’s been on an expansion tear and grappling with a slowdown in new development, one of its core revenue streams.

On the face of things, Durkin’s promotion signals Elliman’s intent to keep growing its physical footprint. The longtime Corcoran Group manager jumped to Elliman two years ago and has been instrumental in Elliman’s acquisitions of other brokerages ever since.

In August, Elliman acquired Los Angeles-based Teles, a fast-growing firm that had $3.4 billion in revenue in 2016. It also announced plans to acquire Boston-based Otis & Ahearn.

“Our next stop is San Francisco,” Durkin said in early December. “And we have a couple more we can’t say yet.”

But while Durkin has publicly projected a harmonious atmosphere at the firm, sources say tension and uncertainty are bubbling beneath the surface.

Just two weeks before the managers’ dinner, Lorber held a brief, early-afternoon conference call to announce Durkin’s elevation to firm president.

Sources said the news stunned Steven James, Elliman’s CEO of NYC brokerage, who was humiliated after being passed over and retreated to his office, where he festered the rest of the day, angry that he hadn’t been told of the reshuffling in advance.

Over the next few days, insiders said, James considered leaving the firm, but he ultimately decided to stay after talking to Lorber, who reassured him that he wouldn’t have to report to Durkin. Instead he will continue to report directly to Lorber and Herman.

In an interview late last month, Lorber declined to define a fixed chain of command — Elliman favors “open lines” of communication — but he said James reports to the top.

“In New York, where most of the money is made, that’s Steven James,” he said. “And Steven speaks to Dottie, he speaks to me.”

Meanwhile, rumors abound about whether Herman, who until recently served as both president and CEO, is on her way out. Lorber aggressively denied it.

“She’ll have to be carried out,” he said, joking, “I’ll be the same way.”

‘One person doesn’t work’

Douglas Elliman isn’t the only New York City residential brokerage at an inflection point. Realogy — parent company of Corcoran Group and Citi Habitats — recently announced that CEO Richard Smith would be succeeded by Ryan Schneider, an executive with finance and technology chops. In New York, Brown Harris Stevens promoted Bess Freedman to co-president, alongside longtime brokerage chief Hall Willkie.

For his part, Lorber insisted that this latest round of changes made sense given how large Elliman has grown.

“Having everyone report to one person doesn’t work,” Lorber said in early December after the Durkin announcement, referring to Herman. “You need someone else in there.”

Herman, who purchased Prudential Long Island Realty in 1989, teamed up with Lorber in 2003 to buy the Manhattan brokerage for nearly $72 million. She currently owns 30 percent of the company. The other 70 percent is owned by Vector Group, in which Lorber holds a 5.6 percent stake that’s worth around $170 million based on its latest stock price.

Sources have long characterized Elliman’s balance of power as tilted in Lorber’s favor, despite Herman’s loyal following. Agents and managers have been known to line up outside her office at 575 Madison Avenue, eager to bounce ideas off her, they said.

“She was a shrink for half of them. He’s not like that,” said a former employee.

Lorber, meanwhile, has a penthouse office a few blocks away at 712 Fifth Avenue. “When something really needed to get done, they’d go to Howard,” the ex-employee said.

Lorber has also been the key dealmaker on landing new development assignments, often by putting money into projects. Vector’s New Valley, for example, is an investor in projects like 111 Murray Street and 10 Madison Square West, which Elliman is marketing.

“I just lost a deal to them because Howard became an investor,” said one marketing executive. “I don’t happen to have the luxury of that business model.”

In recent months, however, Herman — who is worth $270 million, according to Forbes — has stayed out of the spotlight, fueling rumors that she’d been sidelined. Durkin’s promotion lent credibility to those claims, even after Herman posted a cheerful photo of herself — with Durkin and De França — at Art Basel in Miami.

In mid-December, Herman flatly denied that she’s leaving.

“I own 30 percent of the company,” she said, noting that she personally recruited Durkin. “I’m not an employee. I don’t have any insecurity.”

While this latest reshuffling has ruffled feathers, Elliman has been making management changes for the past few years. For example, Stephen Kotler, the firm’s former COO, moved to L.A. in 2015 to head the firm’s West Coast expansion. (Durkin was appointed COO in his place.)

And the firm has also recently made personnel cuts.

In 2016, Elliman fired Nicole Oge, who oversaw a massive marketing expansion, and it laid off Cliff Finn, head of leasing for new rental projects. Then in 2017, the firm terminated Richard Pérez-Feria, the editor-in-chief of Elliman Media, who had been tapped by Oge to turn Elliman magazine into a 300-page lifestyle publication. Brokerage executives now acknowledge the magazine lost its way and have relaunched it with a renewed focus on real estate.

Many of Elliman’s recent initiatives have Durkin’s fingerprints all over them — from its expansion in Westchester and L.A. to its newly forged relationship with Zillow Group. In November, StreetEasy and Elliman announced that the listings portal would build a back-end listings system for the firm, replacing Limo, the brokerage’s longtime system.

“I’ve never seen the company run so well [as it has] over the last year, two years,” said Kotler, adding that Durkin is well-liked and has a reputation as a good listener who can roll up his sleeves.

Durkin, he said, was an “important partner” during Elliman’s acquisition of Teles, which added 500 agents and 20 offices to the firm’s ranks. But others are more skeptical of Durkin, who spent 26 years at Corcoran and is a Barbara Corcoran protégé. “I thought [his promotion] was surprising, with Scott coming in so quickly,” said one brokerage chief.

Some Elliman insiders — who declined to speak on the record — said Durkin’s appointment lays the groundwork for De França to take over as CEO.

“At some point in business — at my age, Dottie’s age — you start to think about who the new leaders are going to be,” said Lorber, 69. (Herman is 64.) “We’re not quite there yet.”

But by tasking Durkin with day-to-day operations, Elliman is taking pressure off the CEO job — a move some speculated could be part of a strategy to move De França into that spot. With Durkin now president, De França could feasibly take the CEO job while also running the ever-important Douglas Elliman Development Marketing.

“Her forte is development, and that’s an integral part of our market, yet that’s under duress,” said one insider. “So, to pull her out of that … could be a very difficult thing.”

New development shakeout

Formerly a top sales executive at Related, De França joined Elliman in 2011 to lead its struggling new development division.

By 2013, DEDM had $3 billion in contracts and sales — up from $300 million in 2012.

“I made a promise to Dottie and Howard when I joined them that I would use my best efforts to grow the largest and strongest new development division in the city,” she said in a 2013 interview, in which she vowed to unseat Corcoran Sunshine Development Group as the city’s dominant new development marketing firm.

Although De França hasn’t fully realized that goal, she has closed the gap significantly. DEDM currently has $30 billion worth of new development projects in the pipeline and the firm ranked No. 2 on TRD’s most recent roundup of the city’s top new development marketing firms, with $5.92 billion in sales between June 2014 and May 2017. Corcoran Sunshine took the No. 1 spot with $9.13 billion in sales.

But amid a slowdown in the new development market, Elliman has struggled with profitability. The low point came in May, when it announced just $100,000 in profits for 2017’s first quarter, as new development closings dried up. That was despite selling $5.6 billion worth of real estate during the quarter and having $30 billion worth of new development work in the hopper.

“If I returned results of $100,000 a quarter, I’d be calling all of you here begging for a job,” quipped Corcoran CEO Pam Liebman, taking a jab at Lorber at TRD’s new development forum that month.

In October, Elliman eliminated Roy Kim’s position. Kim joined the firm in the newly created job of chief creative officer at the market’s peak in 2015. “The financial challenges facing new development today are not a secret,” said Kim, who was focused on the sector.

The firm has also been grappling with slow sales at Bruce Eichner’s Madison Square Park Tower and Macklowe Properties’ 200 East 59th Street.

In Miami, HFZ Capital Group recently scrapped plans for a 67-unit project at the Shore Club that Elliman was slated to market. And in L.A., it stepped away from marketing Greenland USA’s $1 billion Metropolis development after selling two-thirds of the units. (Sources said the decision was mutual.)

“In 2017, many [projects] were furloughed or late getting to the market. That’s something we can’t predict or change,” said Durkin.

On a Nov. 7 earnings call with Vector investors, Lorber addressed a year-over-year drop in profitability during the third quarter to $4.2 million from $8.7 million.

“We think our growth will continue,” he said. “[But] we want to watch our expenses, obviously, so we can try to trim down when we can.”

Of course, Elliman isn’t the only firm contending with a tough market.

Manhattan new development units sat on the market an average of 264 days during the third quarter, up 65 percent year over year, according to appraisal firm Miller Samuel. The median price of a new condo also dropped 23 percent to $2.8 million. But some former Elliman employees said the new development division isn’t a golden goose like it is at Corcoran.

“At Douglas Elliman, it’s not the same thing,” the source said. “New development exists to draw in really big-name brokers, and most of the money goes to them.”

Lorber himself has acknowledged that. “Her model is a much better way for a company to make money,” he said at TRD’s forum, referring to Liebman and Corcoran.

As an entrepreneur, he said, he’s “willing to invest that money to build.”

De França said that Elliman will continue to expand its “boots on the ground” in California and Florida over the next three to six months. DEDM currently has $17 billion worth of new development listings, including $11 billion in New York.

Lorber said the company’s next focus is on ensuring that all of its regions are profitable. “Our numbers suffer from the new territories we’re in,” he said. (California agents, for example, earn higher splits on average.)

“I don’t want to cut back if it hurts our business. I don’t like throwing away money,” he noted. “But my basic philosophy is, I’ll spend what I have to spend.”