When Silverstein Properties was bidding on the Helmsley Carlton House eight years ago, company executive Marty Burger thought his firm had a pitch that would win the property.

“[We had] a very well-known hotel brand that agreed to let us use their name to sell condos,” Burger, who is now Silverstein’s CEO, recalled last month. “We thought that was our edge.”

But as it turned out, that edge was not sharp enough.

Instead of selling the famed hotel to Silverstein, the estate of Leona Helmsley — aka “the Queen of Mean” — went with private equity giant Angelo, Gordon & Co. and Extell Development, which paid $175 million.

While all the other bidders were focused on converting the property to condos, Extell’s Gary Barnett had crafted a different play. Not only would he convert the building into 68 cond-ops, he’d also create more retail. Those calculations, Burger said, allowed the duo to bid more.

And Extell ultimately sold that Madison Avenue retail to Thor Equities for the hefty price of $277 million.

“It made 100 percent sense,” Burger said of the retail play, “and I kicked myself for not thinking of it because [it was] just a different approach.”

While the sale of the Carlton House was years ago in a market that looks a lot different from today’s, it offers a window into the seemingly never-ending quest for New York City’s biggest landlords to grow even bigger.

For this issue, The Real Deal set out on its own epic quest — to create a first-ever ranking of the largest property holders in the city by both total square footage and annual net operating income. (The NOI is revenue minus expenses before taxes were paid as publicly listed by the city.)

The undertaking was massive, and many landlords did not participate, so their numbers may be undercounted, but the ranking offers a rare look at just how much real estate some of New York’s biggest players have to their names.

The undertaking was massive, and many landlords did not participate, so their numbers may be undercounted, but the ranking offers a rare look at just how much real estate some of New York’s biggest players have to their names.

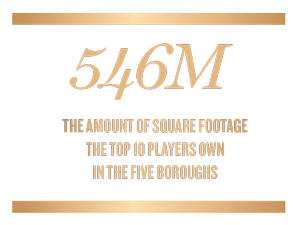

Together, the top 10 players on TRD’s list own roughly 546 million square feet of property citywide — with the city itself owning about 66 percent of that total.

That, of course, is just a fraction of the nearly 5.5 billion square feet of property and land citywide, but it’s still a sizable chunk that encompasses many of the largest properties in New York.

Meanwhile, the 10 owners with the highest NOI are throwing off a combined $7.5 billion a year — more than the GDP of the entire country of Liechtenstein. And that NOI doesn’t include condos they’ve sold, buildings they’ve unloaded or projects they currently have under construction, which are not yet producing income. TRD’s NOI tally is simply meant to measure income from leasing that firms are generating right now in New York.

The players who made TRD’s cut are a mix of famed private family firms, the country’s biggest real estate investment trusts, major universities and institutions, and firms that are backed by big institutional money.

And many are poised to get even bigger, especially as developers move deeper into emerging neighborhoods.

Jay Neveloff, partner at Kramer Levin Naftalis & Frankel, noted that every market has “its own value.”

“It’s just a question of what’s the next hot place,” he said.

Who’s on top?

To the surprise of nobody, the City of New York is the biggest property owner in the five boroughs — with a massive 362.1 million square feet to its name, according to TRD’s analysis. Think 1 Police Plaza, Stuyvesant High School and the New York Public Library building on Fifth Avenue.

That is more than one and a half times what the top 10 private companies on the list own combined.

Vornado Realty Trust — the Steve Roth-run REIT — took the No. 2 spot, with 29.7 million square feet.

Meanwhile, SL Green Realty clocked in at No. 3 with about 28.7 million square feet. Rounding out the top six were Tishman Speyer with about 20.5 million square feet, Blackstone Group with 20.1 million and the Related Companies with 18.7 million.

To determine who owned what, we set a snapshot date of June 30 and pulled thousands of property records from public sources, including ACRIS, the city Department of Housing Preservation and Development, the Department of Buildings and others.

Silverstein Properties’ 3 World Trade Center

Then we cross-referenced those buildings with the annual “notice of property value” that the city’s Department of Finance sends to landlords, which lists an estimate of NOI before taxes are paid. (Residential condos were excluded from the ranking, and NOI for commercial condos was estimated based on public records.)

Brookfield Property Partners, which has been on a development-and-expansion tear lately, took the No. 8 spot with about 17.5 million square feet of space.

But that did not count many of its biggest properties, including under-construction offices towers One Manhattan West (2 million square feet) and Two Manhattan West (1.7 million square feet). Nor did it include 666 Fifth Avenue (1.5 million square feet). At that tower, Brookfield struck a deal with Kushner Companies for a 99-year lease with an option to buy it, but the transaction occurred after our June 30 deadline.

The company has ramped up outside of Manhattan as well.

In April, it signed a contract to buy a seven-building development site in Mott Haven in the Bronx for $165 million. And the firm is also partnering with the Park Tower Group at Brooklyn’s Greenpoint Landing on four residential buildings at a projected cost of about $1.6 billion. Development sites counted only toward building totals, not square footage. They also don’t contribute much to NOI since they are not yet generating income.

But overall, Brookfield locked down about $1 billion in large projects across the city during the first six months of the year, according to a recent TRD analysis. And all of that is not to mention that the company recently announced plans to buy the REIT Forest City Realty for $6.8 billion.

Ben Brown, who took over as head of New York and Boston real estate at Brookfield in April, said the city’s shortage of large development sites has pushed the company into areas like Greenpoint and the South Bronx.

“We have that critical mass where we really have the opportunity to do some playmaking there,” he said. “[We] have that opportunity to create a whole ecosystem.”

While Brown acknowledged that the company has been more active than its competitors recently, he stressed that its pace is fairly normal for a $10 billion global firm.

NYC Property Owners With The Biggest Footprints

| RANK | FIRM/ENTITY | TOTALnSQUAREnFEET | NO.nBUILDINGS/nVACANTnPARCELS |

|---|---|---|---|

| 1 | NYC (government) | 362.1M | 4,941 |

| 2 | Vornado Realty Trust | 29.7M | 77 |

| 3 | SL Green Realty | 28.7M | 73 |

| 4 | Tishman Speyer | 20.5M | 36 |

| 5 | Blackstone Group | 20.1M | 31 |

| 6 | Related Companies | 18.7M | 156 |

| 7 | Columbia University | 17.9M | 246 |

| 8 | Brookfield Property Partners | 17.5M | 19 |

| 9 | RXR Realty | 16.5M | 22 |

| 10 | New York University | 14.3M | 111 |

| 11 | Durst Organization | 14.1M | 49 |

| 12 | LeFrak Organization | 13.9M | 86 |

| 13 | Rudin Management | 13.1M | 36 |

| 14 | Solil Management | 12.5M | 102 |

| 15 | Silverstein Properties | 12.1M | 14 |

| 16 | Cammeby's International Group | 11.5M | 82 |

| 17 | Mount Sinai Medical Center | 10.3M | 55 |

| 18 | Glenwood Management | 9.6M | 33 |

| 19 | Boston Properties | 9.5M | 10 |

| 20 | New York-Presbyterian Hospital | 9.3M | 58 |

“If you look at SL Green’s business, recently they’ve been disposing of a lot of their assets,” he said. “And that’s in an effort to buy back shares, which management thinks are cheap. … That’s just a different view and a different investment strategy than we’re deploying.”

And those different approaches play into each other, said Brown.

“If the majority of our peers are selling assets, that means that there’s either a very deep pool of buyers — and that makes things a little more difficult for us — or there’s a lot of supply on the market,” he said.

But even though SL Green is unloading assets now, it has still significantly increased its New York holdings in the last five years. In February, when the REIT, which is headed by Marc Holliday, filed its annual report with the U.S. Securities and Exchange Commission, it claimed to own about 28.7 million square feet of real estate across 70 properties in Manhattan. That square footage is slightly higher than TRD’s more recent figure and up from 23.2 million square feet of real estate across 32 properties that it claimed at the same time in 2013.

SL Green President Andrew Mathias cited the company’s redevelopment of One Madison Avenue and its under-construction, 1.5 million-square-foot office property at One Vanderbilt as a sign of its confidence in New York. The latter property is scheduled to open in 2020 and is 30-plus percent leased, with tenants including private equity firm the Carlyle Group and TD Bank.

In a statement to TRD, Mathias said there was “strong optimism for New York City’s economy, particularly in Midtown Manhattan, which just had the strongest quarter of leasing activity since 2015.”

Meanwhile, in its most recent annual report, Vornado reported that it had 23 million square feet of office and retail in Manhattan alone, along with 2,009 residential units plus the Hotel Pennsylvania. That compares to 22.2 million square feet of Manhattan office and retail five years ago — and 1,653 residential units plus the hotel.

Representatives for Vornado, Tishman Speyer and Blackstone declined to comment.

But with the exception of major players, sources say many buyers are sitting on the sidelines now and are not in growth mode.

Investment sales in Manhattan have not increased since 2015, when they hit a record high of $55 billion. Although a recent report from Avison Young predicted that Manhattan below 96th Street could see $20.7 billion in trades by the end of the year — an uptick from 2017 — activity in July was down for most major property classes.

Investment sales in Manhattan have not increased since 2015, when they hit a record high of $55 billion. Although a recent report from Avison Young predicted that Manhattan below 96th Street could see $20.7 billion in trades by the end of the year — an uptick from 2017 — activity in July was down for most major property classes.

Chris Delson, a partner in the real estate group at the law firm Morrison & Foerster, noted that most companies have not been aggressive about buying or selling recently. But he attributed that to a long streak of price increases that has made some firms nervous about overpaying.

“The up cycle has been going on for so long that I think the smart money out there is somewhat cautious,” Delson said, “just because it has been going on for so long and prices have run up for so much.”

While most of the firms did not provide TRD with their NOI numbers — it would be a welcome shock if they did — they are raking in a lot of cash.

SL Green ranked No. 1 with an annual NOI of $1.44 billion for its New York holdings. It was followed by Vornado (with about $1.17 billion), Boston Properties ($793.6 million), Tishman Speyer ($788.3 million) and the Durst Organization ($713.6 million).

While the city owns more property than any other entity in New York, we did not include it on the NOI chart because it’s not generating revenue from many of its properties. We did include hospitals and universities because while they are not real estate firms they do make money off of their real estate.

That contrasts with a company like Boston Properties, for example, that has high-profile towers like the GM Building and 250 West 55th Street.

The firm declined to comment, but rents at 250 West 55th have gone for between $80 and $140 per square foot. And an analysis from Fitch Ratings last year found that the GM Building could make $184.3 million annually moving forward.

Neveloff said the overall amount of money available in real estate had risen tremendously over the last few decades.

“You’ll see names of individual players, but that doesn’t tell the story,” he said. “There’s so much more wealth around than there was before.”

Looking for B locations

Even if buyers here are taking a collective breath this quarter, they have challenges beyond market forces to contend with: namely, where they can build.

Development sites — whether that’s vacant land or buildings that can be demolished or repurposed — are scarce and expensive.

Still, developers don’t seem overly concerned about the city’s finite space. In fact, while it may be clichéd to note that they are pushing deeper into the boroughs and developing new neighborhoods, the cliché is still true.

Brookfield’s Manhattan West project

“Every neighborhood is viable,” Silverstein’s Burger said. “You used to say, ‘Oh, I’d never go there. It isn’t a good neighborhood.’ Now, every neighborhood is desirable for some reason.”

The company — which has 12.1 million square feet and logged an NOI of nearly $600 million on the ranking — made its first major push into the outer boroughs this year. It acquired a seven-parcel development site in Astoria stretching two blocks between Steinway Street and 42nd Street.

Durst also recently expanded into Queens with the 2,400-unit Hallets Point project and its purchase of the Clock Tower site in Long Island City, where it is planning a 958-unit rental building. TRD’s analysis showed Durst with 14.1 million square feet of property — including high-profile towers like One Bryant Park, 1133 and 1155 Sixth Avenue and the Bjarke Ingels-designed rental Via57 West.

“It used to be we would not go outside of Manhattan,” company Chairman Douglas Durst said, “and now we look at all the boroughs.”

As developers broaden their geographic horizons, the value of assets in areas that have not historically been considered prime has seen a boost, Delson said.

“Maybe this is in a B location,” he said, explaining developers’ thought process, “but I can renovate it, put some money in and either make it an A building or an A-minus building.”

In the last few years, the pool of buyers has expanded as well, according to investment sales powerbroker James Nelson, a principal at Avison Young.

A lot of these realities stem from the foreign -investment explosion.

In the 1990s and early 2000s, the market was geared much more heavily toward a smaller pool of family buyers. At that time, he said, he could easily predict who the first dozen players to call would be when a new property hit the market.

“It was a lot of the same families, certainly for the multifamily sector,” he said. “You have a lot of generational holders.”

Scott Rechler, CEO of RXR Realty, pointed to the increase in institutional buyers over the past two decades, which he attributed to investors focusing more on financing buildings through equity than debt. This tends to ensure that once buildings are off the market, they stay off the market.

NYC Property Owners With Highest Annual Net Operating Income

| RANK | FIRM/ENTITY | TOTAL NOI | NO. OFnBUILDINGS/nVACANTnPARCELS |

|---|---|---|---|

| 1 | SL Green Realty | $1.44B | 73 |

| 2 | Vornado Realty Trust | $1.17B | 77 |

| 3 | Boston Properties | $793.6M | 10 |

| 4 | Tishman Speyer | $788.3M | 36 |

| 5 | Durst Organization | $713.6M | 49 |

| 6 | Brookfield Property Partners | $660.9M | 19 |

| 7 | RXR Realty | $653.1M | 22 |

| 8 | Related Companies | $642.3M | 156 |

| 9 | Blackstone Group | $632.5M | 31 |

| 10 | Silverstein Properties | $599.5M | 14 |

| 11 | Rudin Management | $498.5M | 36 |

| 12 | Fisher Brothers | $475.5M | 11 |

| 13 | Columbia University | $464.9M | 246 |

| 14 | New York University | $459.7M | 111 |

| 15 | Jeff Sutton/Wharton Properties | $439.1M | 105 |

| 16 | Mount Sinai Medical Center | $408.1M | 55 |

| 17 | Solil Management | $340.3M | 102 |

| 18 | Paramount Group | $322.8M | 6 |

| 19 | Glenwood Management | $302.5M | 33 |

| 20 | New York-Presbyterian Hospital | $300.7M | 58 |

“Properties being sold, particularly the higher-quality Class A assets, are being sold to buyers that are long-term holders,” said Rechler, whose firm had about 16.5 million square feet of property in the city and an NOI of about $653 million.

“So,” he noted, “it’s unlikely that they come back onto the market anytime soon.”

The cost of development has skyrocketed over the years as well — making it harder for new players to get in the game.

Alex Goldfarb, managing director at investment bank Sandler O’Neill, said Manhattan development sites can now easily go for more than $1,000 per square foot. In general, this has made companies much less eager to stockpile several development sites at once.

If a developer is able to assemble a site that can actually produce income, “then, yeah, you’re happy to do that and wait,” Goldfarb said. “But to just lock up a bunch of parking lots and hope at some point it comes around? You’re probably not going to do that.”

Goldfarb cited Vornado as a company currently focused on smaller, safer projects. However, with the No. 2 NOI in the city, the company, which is building the ultra-luxe residential tower at 220 Central Park South, has undoubtedly been strategic about when it gets aggressive.

Roth has been famously quiet about the under-construction project. But the company got in early, buying the property in 2005 for $132 million and spending $40 million to buy out its rent-regulated tenants.

“They’re not mega, certainly, not like replacing the Hotel Pennsylvania,” Goldfarb said, referring to the projects the company is currently working on. “So the projects are smaller in scale, so there’s less financial risk.”

Still a blood sport

News flash: New York real estate is famously cutthroat. And that means if an owner wants to get bigger, it often must be more aggressive than everyone else.

Even a company like Brookfield that’s been picking up assets left and right loses some. Brown cited the St. John’s Terminal site in Lower Manhattan as one that got away. Despite Brookfield bidding on it, Oxford Properties Group and Canada Pension Plan closed on a $700 million purchase of the south portion of the site at the beginning of the year from Westbrook Partners and Atlas Capital Group.

“We liked it a lot and spent a lot of time on it,” Brown said. “Unfortunately, we weren’t successful in getting it.”

But others said the industry is no more competitive now that it’s been in the past. Today, Brown said, many major players are focusing more on developing than acquiring.

“The past couple of years in New York, there’s probably been a lot more competition on the development side,” he said. “I think people still had very rose-colored glasses on. I think that’s tempered a bit.”

Silverstein’s Burger characterized the city’s current market as “heady,” mainly because there are so many different sources of capital pouring in.

“Zoning changes. Demand changes,” he said. “Today, anyone who’s a developer in New York would love to build a multifamily building, because multifamily is gold.”

Kaufman Organization President Steven Kaufman — whose company did not make the ranking but had about 4.7 million square feet of real estate, according to TRD’s analysis — said new players like office-sharing companies WeWork and Knotel are upping the cost of staying in the game. “With new owners in the marketplace spending a lot of money on buildings,” he said, “the older legacy owners such as ourselves are in a position where we have to spend more to stay competitive.”