UPDATED, March 9, 2021, 5:02 p.m.:

Sometimes you can lose and still win.

Douglas Elliman’s Manhattan sales dropped more than 23 percent last year from an eye-popping 2018 total of nearly $9 billion, but it still retained its No. 1 spot on The Real Deal’s tally of closed sales for 2019.

Elliman also managed to edge out its rival the Corcoran Group in TRD’s new three-borough ranking, which tallies sales for Manhattan, Brooklyn and Queens — but only barely. The firm logged $7.96 billion in sales across the three boroughs, just $117 million ahead of Corcoran’s $7.84 billion.

Elliman’s New York CEO, Steven James, shrugged off his firm’s drop in Manhattan sales.

“I think all sales are down for everybody,” he said. “It’s the state of affairs.”

But while Elliman’s Manhattan sales dropped last year, those of Corcoran and Compass jumped 35 percent and 111 percent, respectively.

Related: The residential firms with the highest dollar volume of listings

Some of the shifts can be explained by external factors. Elliman said last year that in Manhattan, the firm’s 2018 sales were somewhat inflated by deals signed at the peak of the market finally closing that year. And Compass’ dramatic leap was driven partly by its April 2019 acquisition of its comparably sized rival Stribling & Associates, which last year had bested it in the ranking.

Corcoran President and CEO Pam Liebman, however, attributed her firm’s surge in closed sales to its lead-generation systems, which the brokerage began laying the groundwork for in 2018 but only began making the most of last year.

“It took a while to get it going. It really started to see enormous success in 2019,” she said.

Few other firms saw sales rise last year, however.

Few other firms saw sales rise last year, however.

The number of all sales across Manhattan last year was down 1.8 percent from 2018 to 10,048, according to appraiser Jonathan Miller, who authors Elliman’s market reports.

The Big Apple’s luxury market was especially depressed under the weight of new development inventory piling up. The final quarter of the year saw sales over $5 million tumble 38 percent year-over-year. The number of sales recorded between $7 million and $20 million was nearly halved, according to Miller’s Q4 Manhattan market report.

“Who is more dependent on the high end is more exposed,” said Miller.

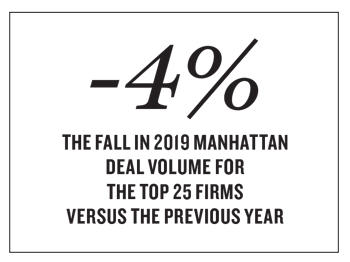

The elite brokerages were indeed hit the hardest. Together, the top 25 firms in Manhattan’s closed-sales ranking reported $23.1 billion worth of sell-side deals last year. That’s down from $24.1 billion for the top firms in 2018, according to TRD’s analysis — a nearly 4 percent drop.

On the other hand, more moderately priced properties, ranging from $3 million to $5 million, saw sales tick up more than 15 percent year-over-year, according to Miller.

Citywide, 2019 was a year of extremes, as a tax on high-end sales lobotomized the calendar — triggering a rush of closings just before the levy took effect on July 1, followed by a dearth afterward. June 2019 was the best month on record for residential real estate priced at $2 million or higher, according to a Wall Street Journal analysis, which found that a total of 673 deals valued at about $4.8 billion closed in that month alone.

But it remained a stubborn buyer’s market in Manhattan, with many units going unsold despite low interest rates, incentives and concessions. As a result, both firms and agents sought greener pastures farther afield from Manhattan’s forest of languishing condo towers, as markets rose in Brooklyn and Queens.

In fact, in both of those boroughs, more than 20 percent of deals in the final quarter of the year closed above the asking price.

To underline the growing significance of the outer boroughs to brokerages’ bottom lines, this year, for the first time, TRD’s ranking of the city’s top firms by closed sell-side deals also includes sales in Brooklyn and Queens. The rankings by headcount and listings also include the three boroughs.

TRD’s ranking methodology, though expanded in geographical scope, remains the same as in past years. To determine the numbers, we scraped thousands of listings from real estate data firm LavaMap across Manhattan, Brooklyn and Queens. With the listing data, we then cross-referenced these listings with closed deals in public records and checked these numbers with the brokerages. Firms also had the opportunity to submit deals for review.

Buy-side deals are not counted toward a firm’s total in TRD’s sell-side ranking, nor are sales handled in-house by developers. Off-market transactions are also excluded, as those cannot be publicly verified.

Elliman is not the only firm that struggled in Manhattan last year. Of the firms on last year’s top ranking for Manhattan sales, more than half saw a year-over-year decline.

Warburg Realty’s Frederick Peters was characteristically candid when asked about a year where his firm, which ranked No. 8 overall, saw a 43 percent drop in Manhattan sales. “It sucked,” he said. “You want me to elaborate?”

Manhattan view

Compass saw a huge leap in Manhattan closed-sale volume, booking $4.24 billion last year — more than double its 2018 tally of $2.01 billion. The firm’s New York regional president, Rory Golod, chalked it up to “continued momentum.”

Corcoran’s 35 percent bump in its Manhattan book gave it $6.13 billion in sales.

Engel & Völkers enjoyed a 24 percent jump in Manhattan sales, with $89 million in closed deals, and Oxford Property Group boosted its business by 23 percent in the prime borough. Sotheby’s International Realty and R New York saw upticks of 15 percent and 12 percent, respectively.

Most other top firms saw either small gains or steep drops in Manhattan sales last year.

No. 6-ranked Halstead booked $1.03 billion in Manhattan, a narrow gain of 3 percent, while its sister company, Brown Harris Stevens, which claimed the No. 4 spot, had $1.46 billion in closed sales — down 19 percent from 2018.

“Business was all over the place,” said BHS CEO Bess Freedman. “But we did do a lot of big deals in 2019, so I think that’s part of the story.”

But the firm’s highest-profile deals were on the buy side, and so were not counted for this ranking. Specifically, BHS broker John Burger represented Amazon chief Jeff Bezos in his $80 million condo purchase at 212 Fifth Avenue, and Sami Hassoumi worked with hedge funder John Griffin for his record-breaking $77 million townhouse buy. Halstead President Richard Grossman said that a larger portion of its business had also shifted to the buy side.

Meanwhile, CORE saw its Manhattan sales drop 65 percent from 2018, and Fox Residential Group (which didn’t make the ranking) suffered a 73 percent fall in its Manhattan book last year.

The biggest year-on-year plunge in Manhattan sales among top brokerages comes courtesy of Keller Williams NYC, which saw a 77 percent dropoff in 2019, with just $47 million in sales. But in perhaps the best indicator of how much all firms suffered last year, that total was still enough to keep Keller Williams NYC in this year’s top 25 ranking for Manhattan sales.

Seller beware

Seller beware

Any agent will tell you that it was their seller that was the problem in 2019.

Warburg’s Peters has a simple diagnosis for the phenomenon: a bad case of the “endowment effect.” That is, the tendency to value your own property higher than the market does.

“This is absolutely the psychological issue that is at the center of our business,” he said.

Consultant Nancy Packes agreed that, though some developers burdened with unsold new inventory have begun the painful process of rationalizing prices, it’s a more difficult step for homeowners looking to sell.

“Individual sellers, unlike professional developers, are much more likely to be emotionally biased in favor of the value of their home and unable to process objectively the evidence that comes from marketing that says the home is overpriced,” she told TRD.

Packes also noted that when brokers advise compromising on price, individual sellers may resist due to suspicion about the motive.

“Also, the homeowner may believe that the broker is interested in speeding up the sale process to get the commission and not in optimizing the owner’s price,” she said.

Liebman said Corcoran turned down many listings in 2019.

“They weren’t realistically priced. I don’t want agents dragged down by feeling that they’re not having success. To use a common expression, work smarter, not harder,” she said.

According to Olshan Realty, of the 935 contracts signed at $4 million or more in 2019, the average price drop from the original ask was 10 percent. Average days on market for luxury properties stretched to 496 days, a four-year high.

In the report, President Donna Olshan said these were “clear signs of strong buyer resistance” and called the market “fragile.”

Sotheby’s CEO Philip White, however, said his firm had a “great” year.

“Our average sales price at Sotheby’s is pretty high, over $3 million,” he said.

Indeed, Sotheby’s average deal value for Manhattan sales was $3.94 million in 2019, up nearly 23 percent from the year before.

Despite the market slowdown, White said he’s not concerned, because it’s “more about quality over quantity.”

Serving Kings and Queens

Quantity did seem to create greater returns for many firms in 2019, as those playing the volume game racked up sales in Kings County and the borough of Queens.

Elliman’s three-borough sales total got a $1 billion boost from its deals in Brooklyn and Queens, while Corcoran’s overall tally gained $1.66 billion from its deals in Brooklyn alone, where 26 percent of its brokers are based.

Keller Williams NYC did 72 percent of its deals in the outer boroughs last year, transforming its 21st rank in the Manhattan leaderboard into a 13th-place finish in the three-borough ranking.

Outside of Manhattan, the hottest market has long been the gentrifying hipster theme park of Brooklyn.

“Every successful 30-something wants a brownstone in Brooklyn,” said Halstead’s Grossman. “In the last 10 or 15 years, that’s really been the miracle of Brooklyn.”

Corcoran’s Brooklyn business accounted for 21 percent of its overall sales total this year, while Halstead did even better, booking 23 percent of its business in the borough.

“We were the first Manhattan firm to go there 22 years ago. We continue to expand,” said Liebman of Corcoran’s plans for the borough. “We’ll probably go further into Brooklyn this year, maybe further south.”

Brooklyn’s strength is even more apparent for midsized firms. Citi Habitats made 34 percent of its sales in Brooklyn last year, and 43 percent of Nest Seekers’ business was there.

Brooklyn’s strength is even more apparent for midsized firms. Citi Habitats made 34 percent of its sales in Brooklyn last year, and 43 percent of Nest Seekers’ business was there.

Compass’ Golod said the firm, which had 12 percent of its business in the borough last year, plans to dig into the market even more with two new offices in Fort Greene and Brooklyn Heights slated to open this year.

Though Queens provided just over 2 percent of the deal volume for the firms in TRD’s ranking in 2019, it also has the greatest potential for growth — a point noted early on by Halstead, which opened offices there five years ago.

Halstead was the ranking’s top firm in Queens last year, closing $179 million — or 11 percent of the firm’s business, the highest percentage among the top 25 firms behind Queens-based Modern Spaces, which did 85 percent of its business in the borough.

Grossman said the firm expects growth in the borough to increase. He pointed to the growing LIC office market, noting that residential development should follow.

Though Queens saw sales prices continue to climb throughout 2019, Grossman noted that the borough is still a value play, particularly compared to Brooklyn. And other firms appear to have noticed.

Compass opened a Long Island City office last year and is launching an Astoria outpost imminently. Corcoran and Nest Seekers International’s star broker Ryan Serhant also opened outposts in Long Island City in the past year.

Asked about other firms’ increasing expansion outside of Manhattan, Grossman said, “imitation is the best form of flattery. They’re following in our footsteps.”

Headhunting

The eternal tug of war between firms to recruit and retain brokers — and the occasional necessity to cull staff to curb costs — makes headcount a useful measure of a brokerage’s health. But a large staff doesn’t necessarily translate to a fatter bottom line.

The average deal for Elliman’s 2,460 brokers across the three boroughs was $3.2 million, while Corcoran’s 1,697 agents averaged $4.6 million per deal. Compass’ 2,112 brokers’ average deal was $2.29 million last year. (A few high-priced sales can skew the average upward.)

Then there’s the question of how many deals agents close. Elliman’s agents were among the most productive in terms of deal volume, averaging 1.7 closings each last year, while Compass’s brokers averaged 1.37 deals. Corcoran did not disclose the number of deals it closed.

Meanwhile, lead-generation firms struggled. Triplemint’s 172 agents averaged a mere 0.37 deals. Elegran’s 103 brokers averaged only 0.33 deals per broker, and LG Fairmont’s 185 agents closed just 13 deals last year — an average of only 0.07 deals.

Aaron Graf, CEO of LG Fairmont, said providing agents with leads doesn’t guarantee success.

“It takes a talented person with a lot of help to consistently close leads,” he said. “One good agent can close more leads than three.”

That realization led to Graf slashing his firm’s headcount by a whopping 45 percent, to 185 from 338.

“We decided to maximize the revenue per agent rather than the headcount,” he explained, saying the firm will never be larger than 200 agents going forward.

But LG Fairmont’s sell-side revenue per agent of $92,495 also lagged in 2019 — well behind comparably sized firms Ideal Properties ($118,236), Level Group ($168,403) and Triplemint ($308,087).

LG Fairmont did not confirm or contest TRD’s data on the firm.

Keller Williams NYC also saw a big cut in its bench, with a 38 percent drop in numbers to 425. The previous year, the No. 12-ranked firm had 686 agents in its ranks — and that represented a 16 percent decline from the year before.

CEO Ilan Bracha said it was part of right-sizing the firm to weed out unproductive agents. It came as Bracha sold the franchise late last year in the aftermath of a $2 million lawsuit from former landlord Dow Jones over unpaid rent at its 1155 Sixth Avenue office. The firm will be combined with Keller Williams Tribeca and be run by Tribeca’s CEO, Mark Chin.

On the flip side, Compass increased its ranks by 115 percent with 1,000 new agents in Manhattan.

Many firms that were stalwarts of the headcount ranking when it was a Manhattan-only affair have been pushed out of the top 25 this year. Bohemia Realty grew its team by 43 percent, but that wasn’t enough to keep it from slipping five notches to No. 26. Bold New York grew by 38 percent, but it didn’t even crack the top 30 this year.

Other perennials that fell out of the top 25 include Warburg, CORE, Elegran, Spire Group, City Connections and Engel & VÖlkers — most of which either grew or held steady last year.

On the other hand, No. 5-ranked Winzone Realty is a newcomer to TRD’s headcount ranking, because its 861 brokers are all based in Brooklyn and Queens. Same with No. 8-ranked E Realty International, whose 660 brokers are all in Queens.

Supporting your own

Last August, Michael Walker, R New York’s recently hired residential sales manager, found himself at Manhattan’s Small Claims Court. He was there to provide support to one of the firm’s 774 agents.

Though court appearances may seem tangential to the job for the 100 percent commission firm’s newest executive, it’s an example of the brokerage’s hands-on approach and mounting pressure among firms to prove their worth to agents.

At BHS, President Hall Willkie is known to personally stage listings for agents and isn’t above rearranging furniture for them himself.

Broker Lisa Lippman recalled Willkie advising her on the estate sale of a unit at 50 Central Park West that was crammed with items dating back to the 1950s, when its late owner moved in.

Together, they had auctioneers and collectors thin out the items before replacing all the furniture and painting to bring the apartment to market. Despite the apartment being appraised at $5.5 million, it closed for $7.5 million.

Lippman said Willkie’s input is one of the things she loves about BHS.

“I have direct access to Hall and Bess,” she said. “They’ll come see [listings] with me, and they’ll give me advice.”

Even larger firms are making a point of providing their brokers with moral support — amid the stress of a sluggish market.

Elliman began running frequent training sessions with brokers and managers that amounted to group therapy where agents could talk through their feelings.

“I think that’s what’s needed,” said James. “They’re never going to get past the worries unless they verbalize it.”

He said it was a practice the firm picked up in the early 1990s after the real estate market took a nosedive during a national recession.

Corcoran also set up training to coach its agents on how to manage sellers’ expectations and turn down listings when sellers aren’t receptive to dropping prices.

But pep talks can only go so far, and Compass has taken to supporting its agents in the troubled market with cold, hard cash.

The SoftBank-backed firm launched a short-term loan program last year called Compass Concierge, which fronts money to sellers for upgrades and staging that improve the odds of closing the deal at a higher price — helping its agents win more listings and get deals across the finish line.

Compass Concierge has been a draw for brokers who’ve jumped to the VC-backed firm since the loan program launched. When broker Rachel Glazer left BHS for Compass last August, she cited Concierge as the main pull.

“It’s a huge thing, more so than the tech. It’s a way to win listings,” she said. “No other brokerage offers anything like that.”

Darren Sukenik and Benjamin Glazer, two of Elliman’s heavy hitters in new development, echoed the sentiment when they decamped for Compass in December.

James begs to differ, however, saying his firm also offers its agents and their sellers cash upfront to stage apartments and then gets reimbursed once the deal closes. As with Compass Concierge, a seller who stops working with an Elliman agent has to pay back the firm.

“They’re aren’t the only ones doing this,” he said.

Buying time

In a buyer’s market, working with buyers seems like a no-brainer, but Halstead’s Grossman described the realization as “a real ‘aha’ moment” for agents and even himself.

Grossman said he realized that pivoting to buyer representation was the future in spring 2018, when one of the firm’s top producers, Jay Overbye, shared over lunch that he was focusing on cultivating his network of buyers over chasing listings.

“When one of my top agents, known as a listing agent … said, ‘I’m putting a lot more energy in working my buyer pool,’ that was an epiphany,” Grossman said.

In 2019, Halstead’s business tipped to roughly 62 percent buy-side deals, according to Grossman. He said sell-side and buy-side deals are typically split evenly.

Elliman’s James also pointed out that his firm had a good year in buy-side deals.

When he recounted the firm’s biggest wins of the year, Elliman agents brought in the buyer rather than seller in each case. Those deals included Ken Griffin’s record-smashing $238 million penthouse purchase and developer Steve Witkoff selling his penthouse at 150 Charles Street for $31.8 million.

“A lot of agents have had to shift where they’re spending more time [with] buyers,” James said.

Though Elliman’s banner deals were all on the buy side, and BHS clocked big transactions where its brokers brought buyers, not everyone saw buyer representation as a bright spot.

“It doesn’t do you that much good to be a buyer’s representative, because the buyer doesn’t want to act,” said Peters of Warburg. “It absolutely wasn’t a bright spot.”

Peters said the one sign of hope in 2019 came near the end of the difficult year as sellers finally began showing a willingness to compromise.

According to Miller Samuel’s decade report, the average discount for listing prices in Manhattan last year was 6.1 percent, up from 2018’s 5.2 percent, but still below the prior decade’s average of 7.1 percent.

“To the degree there was a bright spot, [it] was about sellers acknowledging the realities and pricing accordingly,” he said. “It was what was, and now we’re moving on.”

Liebman said Corcoran didn’t see a surge in buy-side deals, and its business was pretty evenly split between sellers and buyers. Instead, she credited Corcoran’s strong year to agents focusing on the fundamentals and being open to deals at all price points.

“While everyone was complaining about the taxes, which certainly had an effect, we tried not to listen to the noise. This is the hand we are dealt; how do we achieve success?” she said. “We’ll sell studios and a $200 million apartment. We’re here to service the whole market.”

CORRECTION: This story was updated to clarify that deals done through entities such as Corcoran Sunshine Marketing Group were included in the analysis. A previous version of this article said Corcoran Sunshine’s deals were excluded.