After the binge comes the purge. The condo auction market is heating up in Jersey City, as developers look to move the glut of apartment inventory amassed during the heady building boom in recent years.

Distressed sales of properties are also expected to accelerate in the area, with lenders increasingly looking to wipe their hands clean of troubled mortgage loans.

The urge to purge is the fallout from a frenzied period of condo construction in Jersey City — a stone’s throw from Wall Street — where about 5,000 new units came on the market at premium prices, sources estimate.

Condo prices in Jersey City, which saw a steep run-up during the boom, have dropped between 15 and 25 percent since the height of the market in 2006, experts estimate. Meanwhile, the number of condos closing today in Jersey City is down about 45 percent compared to the peak of early 2007, according to the Marketing Directors, which sells new developments in markets across the country, including Jersey City.

Selling at auction

To nudge condo sales in a market saturated with inventory, marketers are increasingly turning to auctions.

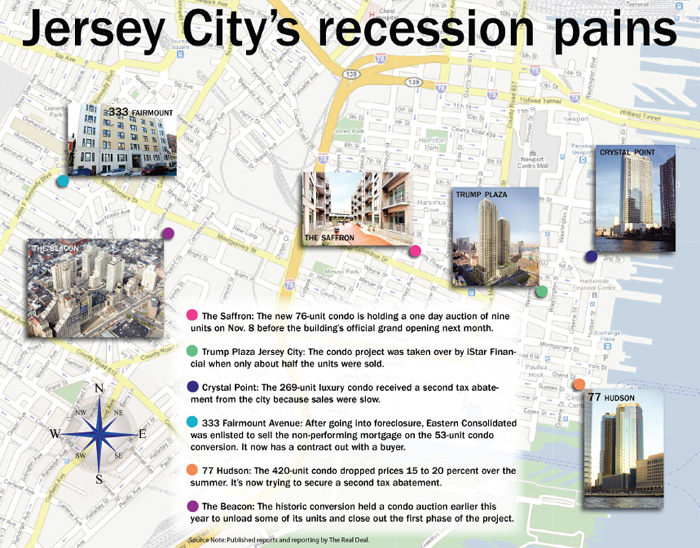

The Saffron, a new 76-unit luxury condo in downtown Jersey City, is taking an unprecedented tack in the market with the one-day auction of nine units before its official grand opening next month.

Developers typically leverage auctions to close out sales at a building, not launch them. But current market conditions have changed the mindset, said Jeff Hubbard, senior marketing director of Sheldon Good & Company, which is conducting the auction.

“An accelerated marketing strategy is now being used to increase the velocity of sales,” Hubbard said. Auctions create “some urgency that doesn’t exist.”

Opening bids at the auction, which will be held on Nov. 8, start at $175,000 for a one-bedroom, compared to standard opening prices, which range from $340,000 to $415,000. The developer is angling to sell between 15 and 20 percent of the inventory, Hubbard said. It’s an absolute auction for nine units, so there is no reserve price, Hubbard said. “The rest [of the units] are subject to seller’s acceptance.”

In June, Sheldon Good & Company also conducted a condo auction at the Beacon in Jersey City to close out phase one of the project.

Meanwhile, Accelerated Marketing Partners is gearing up to conduct auctions at “iconic properties” in Jersey City, said Jon Gollinger, CEO and cofounder of the company, which specializes in auctions at luxury high-rise buildings.

Part of the reason why projects are not moving is because consumers don’t know the fair value of a property these days, Gollinger said. “They don’t want to catch a falling knife,” he noted.

In distress

Some of Jersey City’s new condo constructions and rental conversions that sprouted during the boom have now moved into the distressed column.

As The Real Deal has reported, 333 Fairmount Avenue, a 53-unit Art Deco condo conversion, is one of them.

The property went into foreclosure this summer, and the lender, Chinatrust Bank, enlisted Eastern Consolidated to sell the nonperforming commercial mortgage.

After about 90 days marketing the property, Eastern Consolidated now has a contract out with a buyer that has “substantial experience owning and managing similar projects and in purchasing imperiled projects,” said David Schechtman, senior director of the firm’s turnaround and distressed group. Eastern expects to negotiate more bank dispositions akin to the Fairmount, in both Jersey City and the surrounding areas.

But until recently, there’s been resistance from lenders, who had been taking a wait-and-see approach.

“For the past two years, tons of brokers have been calling up banks and saying, ‘You have a project in trouble; I have someone who wants to buy your problem at a discount,’” Schechtman said. “Banks were saying, ‘We are comfortable with our position. We don’t want your help.’”

Today, the banks are becoming more receptive to the idea of selling their interest in a failed condo property at a loss, he said.

One question is how much trouble nonforeclosed condos are in.

According to Gollinger, a property that is only 50 percent sold is likely to be under some kind of “duress.”

At Trump Plaza Jersey City, a luxury condo development, iStar Financial took control when only about half the units were sold, Dean Geibel, chief executive of Metro Homes, the codeveloper of project, told The Real Deal in August.

Brokers said the condos were overpriced. “The developers just didn’t lower their prices to where the market was,” said Tom Pichi, a broker with Metropolitan and Waterfront Residential Brokerage.

Discounts and abatements

To steamroll sluggish condo sales in Jersey City, new developments are looking to leverage multiple tax abatements, and are signing on portfolio lenders to sweeten the deal for buyers.

Crystal Point, a 269-unit luxury condo on Jersey City’s waterfront, raised some eyebrows this summer when it requested — and was granted — a second tax abatement from the city because sales were slow.

According to Adrienne Albert, the chief executive of the Marketing Directors, the exclusive sales agent for Crystal Point, the development opened with prices adjusted for the downturn. Prices for a one-bedroom currently start at $505,000.

Crystal Point is now about 40 percent sold, and should be fully completed in 2010.

Meanwhile, the 420-unit, 77 Hudson development finished construction this year, and dropped prices 15 to 20 percent over the summer, from $781,000 for a one-bedroom to $669,000, said Dawn Tsien, executive vice president with Prudential Douglas Elliman, which is helping to market the property.

“Obviously, the economy has affected everyone, [but] the building is holding its value” and sales picked up in August, she said.

Nonetheless, the development has a second tax abatement pending. The feeling was, if Crystal Point could get another abatement, why couldn’t 77 Hudson?

“It’s [about] a sense of fairness in the marketplace,” said Tsien.

Beyond tax abatements and discounts, developments like Crystal Point and 77 Hudson are lining up portfolio lenders to secure end-loan financing for prospective buyers. That’s because the market downturn has made it increasingly difficult for developers to meet the Fannie Mae/Freddie Mac requirement that 70 percent of units in a new development be sold before they will back loans in the building.

Portfolio lending has become “an important element of a developer’s marketing program in today’s environment,” Hubbard said.

The Jersey City condo market is expected to see further downward pressure due to the ongoing softening of the Manhattan market, sources said.

Many of the people buying luxury condos in Jersey City had been priced out of Manhattan.

“Now they don’t have to go to Jersey City — they can go to Manhattan,” said Laura Skoler, owner and broker with Century 21 Plaza Realty.