This past spring, the head of leasing at a major office complex in Los Angeles got a surprising phone call from a broker representing WeWork.

Just days earlier, the co-working giant had passed on a 75,000-square-foot-plus space at the complex, which is a short drive from the beach. Now, the broker said, the company had changed its mind.

The landlord’s broker immediately knew what happened: WeWork had gotten wind of the fact that the owner was hammering out a deal with one of its rivals, Spaces (a subsidiary of office-suites giant IWG). Now it was offering to match the terms. But it may have been too little, too late. While a deal has yet to close, the broker for the complex said Spaces looks likely to lock it in.

So goes the world of co-working.

Related: Co-working goes corporate

Backed by millions of dollars in venture funding — in WeWork’s case, billions — co-working providers are adding offices to their portfolios at an astonishing pace. In some cases, they’re gobbling up entire buildings.

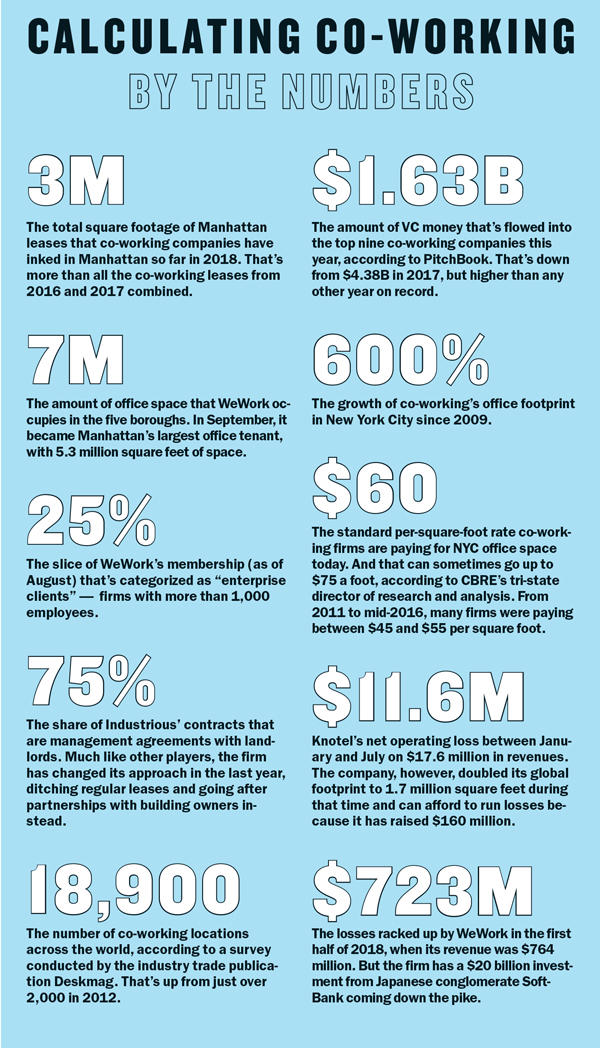

In September, WeWork made headlines when it became Manhattan’s largest private office tenant — with more than 5.3 million square feet under its control. In total, WeWork now occupies more than 7 million square feet of space in the five boroughs. Just last month, news broke that mega-landlord SL Green Realty was clearing out all of 609 Fifth Avenue, a 139,000-square-foot building at 49th Street, so that WeWork could take over. That’s not to mention the millions of square feet WeWork operates in other U.S. and international cities.

Meanwhile, Knotel, which was founded in 2016, already has 71 locations in New York. And Spaces’ CEO Martijn Roordink said he plans to open five outposts internationally every week — indefinitely. It seems at least one co-working company, whether it be a major market leader or a smaller niche firm, announces a new space almost daily.

The most recent market reports reflect the dramatic rise in activity among these firms and an upswing in Manhattan office leasing. This year, co-working companies have inked 3 million square feet in Manhattan leases — more than all co-working leases from 2016 and 2017 combined, according to CBRE market data.

Jonathan Wasserstrum, who runs the tech-centric office leasing brokerage SquareFoot, said some of these flexible office companies are “trying to grab up as much space as they can, as quickly as they can and at whatever numbers they can.”

All of this leasing activity comes at a time when the nascent industry is shifting gears and scrambling to find revenue streams beyond renting out desks to small companies and freelancers. Sources say there’s simply not enough smaller-scale co-working business to go around.

“That market is overcrowded,” said Ryan Simonetti, co-founder of office-amenities operator Convene, which has raised $280 million from investors, referring to the freelancer base of the co-working industry. “Growth for growth’s sake is a dangerous business.”

“You’re seeing a lot of those companies either be sold or consolidate,” he added. “Some of them are going to go out of business over the next 12 months.”

Playing hardball

While growing a business comes with some obvious challenges — from creating economies of scale to increasing brand awareness — there’s one lesser-known issue that these companies are zeroing in on: preventing rivals from increasing their footprints.

Shlomo Silber, who runs the New York-based co-working company Bond Collective — which last month announced two new spaces, one in Soho, the other in Greenpoint — recalled touring a space in Chicago’s Fulton Market area last year.

“We were very excited about the space, and we had a [letter of intent] out and we were ready to go,” said Silber, whose firm has seven New York outposts. “And then we were told that Industrious was touring it, and they ended up getting the space.”

On the surface, it seems there would be more than enough space to meet demand.

There’s no shortage of Manhattan office space — as of 2018’s third quarter, available space in the borough stood at about 54 million square feet, according to brokerage Newmark Knight Frank. And flexible office space still only accounted for 2.5 percent of the Manhattan market as of this May.

But that percentage is misleading.

That’s partly because not all spaces are created equal when it comes to co-working — these firms are gunning for small floor plates that can be broken up into suites with lots of light, reasonable rents and a plentiful supply of young workers nearby.

In other words, “Mad Men”-era Midtown offices with drop ceilings and cavernous floor plates are out.

In New York, there are only so many properties that meet the criteria. And far fewer are available for lease at a given time.

“Whenever we see a building that’s an obvious building where a shared workspace would work, we’re always going to be negotiating against a different competitor,” Silber said.

Amid this competition, some co-working companies are turning to pricier properties.

CBRE’s Nicole LaRusso, the firm’s director of research and analysis for the tri-state area, noted that from 2011 through the middle of 2016, co-working firms were paying somewhere between $45 per square foot and $55 for space.

RXR Realty’s 530 Fifth Avenue

“Now they’re paying routinely more than $60, and more than $70 or $75 in some cases,” she said.

The limited supply of suitable office New York space means that these players can often successfully stunt a rival’s growth by snatching potential locations.

That backdrop helps explain the turf war playing out at the Flatiron Building, where WeWork is reportedly competing with the Office Group, a Blackstone-owned flex office provider, to lease the 180,000-square-foot building. If clinched, the iconic building would be the first U.S. location for the U.K.-based company. A source connected to the property said no decision has been made yet on which tenant will win out.

Silber said it’s often brokers who stoke competition between flexible office companies by playing them off each other.

“Landlords and brokers are trying to get you to try to get into the building because your competitor wants it,” he said. “So they’re kind of causing that a little bit.”

The exclusivity obstacle

As flexible office companies vie for space, some are seeing their efforts stymied by contracts that were written at the start of the decade, when the industry was in its infancy.

Jay Suites’ Jack and Juda Srour

Those contracts often include exclusivity clauses, which prohibit landlords from leasing space to another co-working company in the same building. That language has further restricted the available space for co-working companies and fanned the space war even more.

Juda Srour, who co-founded Jay Suites with his brother in 2009, said every one of the company’s locations has an exclusivity clause.

Related: Who’s keeping it real?

The firm, which has seven Manhattan outposts, takes those contracts seriously. In August, it filed an injunction against Tribeca Associates at 30 Broad Street, seeking to block the landlord from leasing space in the building to Knotel.

“I wouldn’t sign a lease that could move another co-working company into the building,” Srour said, adding that competition from within a building could easily eat into his business.

But with demand from co-working and flexible office startups rising, landlords are resisting these clauses, industry insiders say.

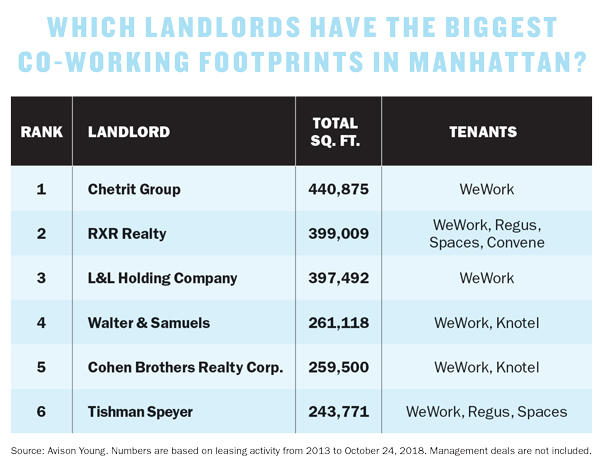

“My landlord clients are very loath to provide exclusivity,” said Avison Young principal John Ryan, who brokered a 116,000-square-foot lease with Convene at 530 Fifth Avenue in September on behalf of RXR Realty. (See chart of landlords with highest concentration of co-working leases).

Jay Suites is something of an industry outlier — having largely sat out the urgent push for more space. The company signed several leases early in the current market cycle, but as office rents have ballooned in recent years it has bided its time. Srour said that the company’s average rent is $38 per square foot and argued that its cheap rents give the company independence from investors.

“I think you need to have the right leases and think about the future,” he said. “We’re probably one of the few without financing, without seed money. We grew organically, and we did it a bit differently than everybody else.”

Space at all costs

The biggest VC-backed firms, however, are following a completely different playbook.

Knotel and WeWork, for example, have insatiable appetites for space and are willing to sign as many leases as possible at pricey rates even if they lose money in the short term. The thinking, sources say, is that they will become profitable in the future — a go-to tactic for venture-backed firms.

Knotel projects that it will make an EBITDA — earnings before interest, tax, depreciation and amortization — profit margin of 22 percent once it has grown to 2.5 million square feet of “mature” spaces with an average occupancy rate of 90 percent, and projects that it will be making an income of $88 per square foot, according to internal company numbers obtained by The Real Deal. (In July, Knotel made $73.30 per square foot, but it claims to have an average $86 on mature spaces).

For now, Knotel, WeWork and others have red ink on their books.

Knotel, which is headed by Amol Sarva, had an operating loss of $11.6 million on $17.6 million in revenues between January and July, according to the internal stats. And as of July, the company’s weighted occupancy rate across all properties was only 58 percent. Knotel declined to comment, but it can afford to run losses because it has raised $160 million.

A Convene space at 101 Greenwich Street

The company nearly doubled its global footprint during that January-to-July stretch, to 1.7 million square feet. Given that newly opened locations often take time to fully lease up and turn a profit, those losses are not necessarily surprising, sources say.

WeWork’s losses are on an entirely different scale.

In the first half of 2018, it racked up a net loss of $723 million on $764 million in revenues, according to technology news website Recode, which focuses on Silicon Valley.

The growth-at-all-costs model does have its detractors.

Marcus Moufarrige, COO of office-suites company Servcorp — which was founded in Australia 1978 and helped pioneer the office-suite business — described the rush for more space as a “Ponzi scheme,” alleging that some co-working startups are using the money they get from landlords for building out their spaces to cover their operational losses.

“It’s a Ponzi scheme using tenant incentives from landlords to fund the losses you’re making from the [location] you opened last time,” he said. “WeWork used that to great effect until they really started raising money, and a lot of people learned from that.”

Arif Shah, a senior director at WeWork, rejected that characterization, calling it a “wild assumption.”

He also said that before opening a location, WeWork does a detailed analysis of the neighborhood — including worker and company demographics — and assesses demand.

“We use a combination of proprietary software and desktop and ground research to do this,” he said. “These are the factors that determine our decision to sign a lease.”

Dangerous growth

Convene’s Simonetti argued that the real threat to the industry is that there are too many co-working spaces in New York City catering to companies with 10 or fewer people.

One of the many companies operating in that space is the Yard — which was founded in 2011 and has 13 New York City locations. Several sources told TRD that the firm has been offered for sale to rival companies. The Yard denied that, saying it is merely “working with an investment advisor to secure growth equity.”

In September, it was offering desks to new members for just $20 per month for the remainder of the year. To put that in context, the Yard normally charges upwards of $400 per month for a dedicated desk.

Yard co-founder Morris Levy characterized the price drop as a marketing strategy at the time.

“We do need to make some noise sometimes,” Levy told Crain’s. “Every single one of our members has heard of our competition. I can’t say that every one of our competitors’ members has heard of us, because we’re the small guy.”

Others, including the upscale company NeueHouse, are on the hunt for more cash to compete, industry sources said.

WeWork, which is backed by Japanese conglomerate SoftBank — now poised to take a $20 billion stake in the company — not only has the means to sign lease after lease, it can also afford to entice potential customers with incentives.

Last fall, the company offered a year’s free rent on two-year deals to any company that switched over from a competitor. And this September, it was offering 50 percent off the first year’s rent and a 100 percent commission to any broker who poached a customer from a key competitor like IWG, Knotel and Industrious, which is headed by Jamie Hodari.

Convene’s Simonetti argued that eventually the flexible office industry will be dominated by a few big companies. Small firms can survive, but only if they can offer a niche product that is different from its big competitors — such as the women-only startup the Wing, which has raised $40 million and counts WeWork as an investor.

“Right now, we are looking at 10 potential companies in that space that are looking to sell, and I get another book or two a week from companies that are either looking to raise money or sell,” Simonetti said. “So the consolidation wave is happening.”