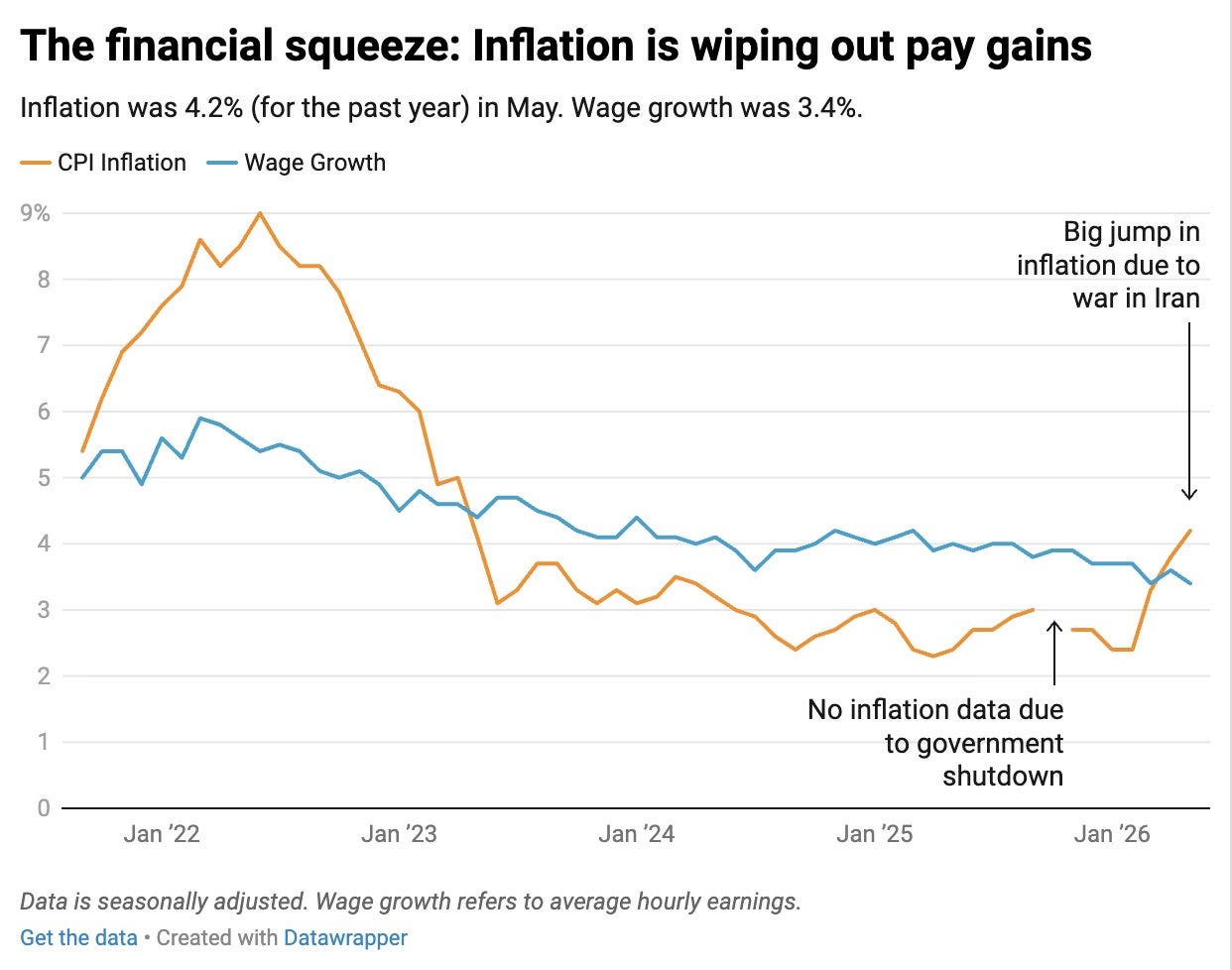

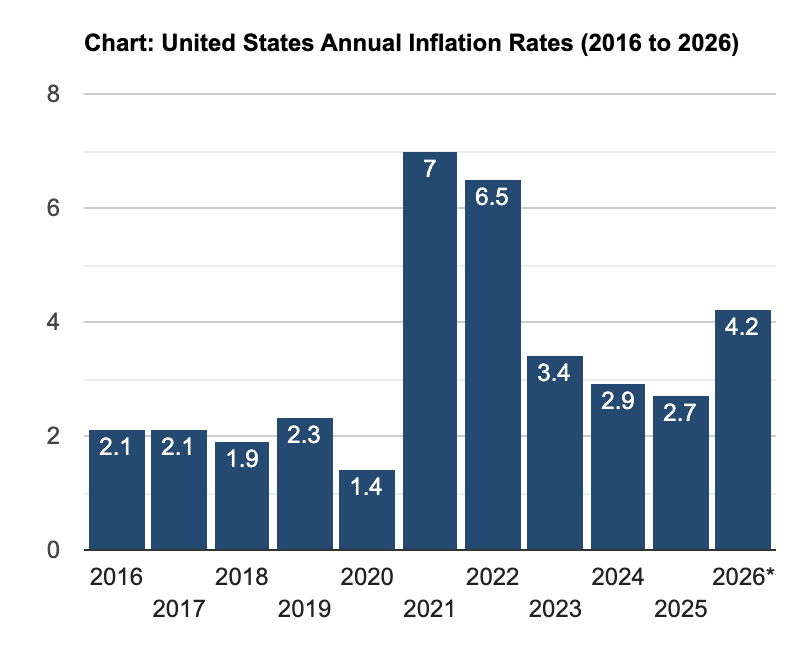

First, let’s set the stage. While the new Fed chair indicated yesterday at his first FOMC press conference that they will hold rates steady, yet inflation is 4.2 percent, the highest in three years, and outpacing wage growth. The good news was that the new Fed Chair showed his independence, despite widespread worry that he would be a dove and push to sharply cut rates, stoking inflation. If he didn’t show his independence, I suspect that mortgage rates would rise. The odds of a rate increase in 2026 continue to rise. According to the CME futures market, the probability of a 25-basis-point rate increase at the next FOMC meeting on July 29 is 34.2 percent, and 49.8 percent at the September 30th meeting. While Freddie Mac shouts for joy every time mortgage rates slip, the Iran War is not settled, and tariffs remain in place for new economic reasons, so it’s hard to imagine mortgage rates seeing much further decline.

As I have mentioned in prior posts, from July of 2025 to February 2026, we had a goldilocks scenario of a “not too hot and not too cold” mortgage rate environment. If mortgage rates drop too quickly, prices tend to surge, and with limited inventory, affordability plummets significantly. Before the Iran War began on February 28th, the spread between the 10-year treasury and the 30-year fixed was compressing, helping mortgage rates drift lower very slowly. The narrowing spread reflected banks’ growing comfort with the state of the economy. In fact, it looked like the Fed was going to cut rates one or two times before the end of the year, and that outlook ended instantly as the war in Iran began. Instead of remaining below 6 percent, we have seen mortgage rates rise during the Iran War conflict to around 6.5 percent.

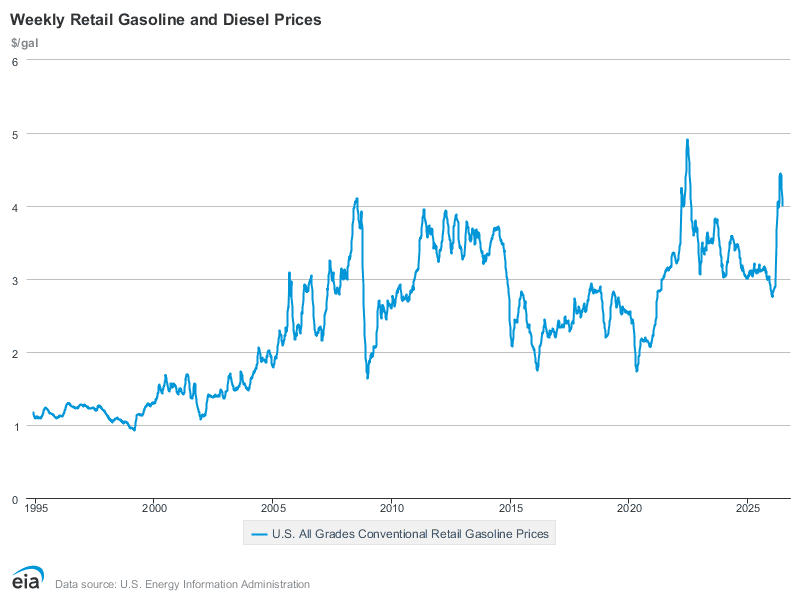

Energy prices rising but not as much as feared

The issue with higher energy costs isn’t just about the price of gas at the pump, but their impact on nearly everything in the economy. A former CFO of a national bank once explained to me that most mortgage lenders anticipate the direction of mortgage rates; it is largely driven by energy prices. All your uncles and in-laws who have been rage-posting on Facebook in their underwear about high gas prices for the past five years have mysteriously gone quiet over the past few months. Yet gas prices have surged by 35 percent to 50 percent since the war began, and inflation just clocked in at 4.2 percent, a clear re‑acceleration, and puts us firmly back in “too hot for comfort” territory at more than double the 2 percent Fed target rate (which has been above that level for 5 years).

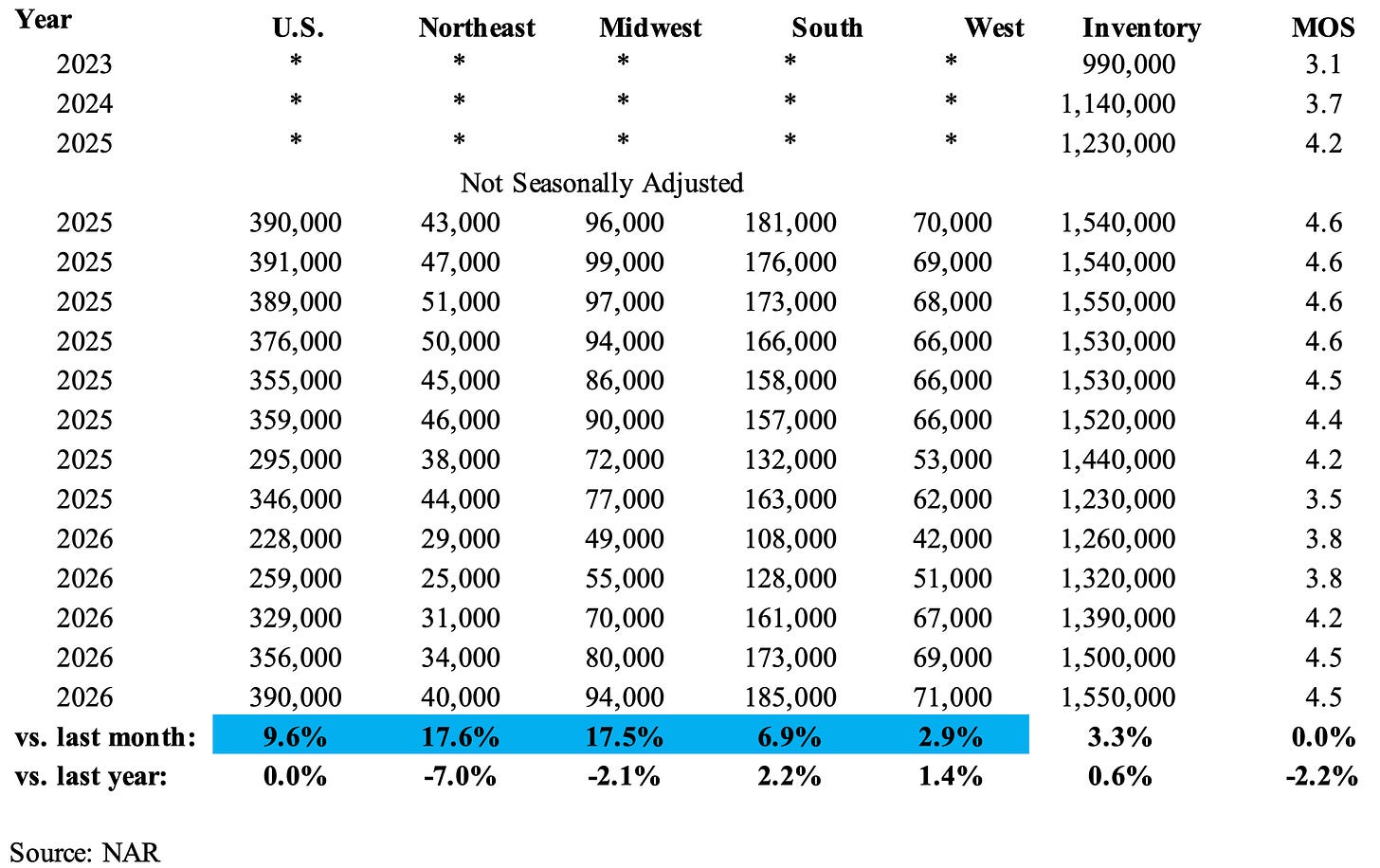

Recent sales surge was enhanced by delayed market

You can see the delay in NAR’s Existing Home Sales release for May reflected in the blue month-over-month percentage change. Those large gains reflect the delayed market start, rather than an unusually robust spring market.

When considering the impact of the Iran war on the housing market, I think of March–April as a negative war‑and‑rates shock on top of an already tight, mortgage rate‑sensitive market, with some contract dates pushed out, or consumers taking longer to make decisions. But those April and May consumers weren’t able to clutch their pearls indefinitely.

Yesterday, I was speaking at a REBNY event, and a question came up about the best way to characterize the market. I described the housing market as about a month delayed because the Iran War delayed the start of the spring selling season; therefore, the peak selling season will likely extend deeper into the summer.

Final thoughts

The Iran war abruptly ended the “Goldilocks” mortgage‑rate window, flipping markets from expecting cuts to assigning real odds to a 2026 hike and nudging mortgage rates into the mid‑6 percent range. What has been looking like a surprisingly strong spring is really that delayed demand, pulling the traditional peak roughly a month later into summer.

National economic strategy is clearly a mess, as it works against a housing market recovery.

The actual final thought — Sometimes things come back unexpectedly.

Read more Housing Notes columns and sign up for email newsletters here.

Read more

Residential

National

Housing Notes: If the mortgage fits, wear the rate