The total amount of new commercial debt issued in the city’s three most

populous boroughs fell slightly in the first half of the year compared with the

same period in 2010, new data provided by PropertyShark.com to The Real Deal

shows, even as commercial sales have rebounded strongly from the recession.

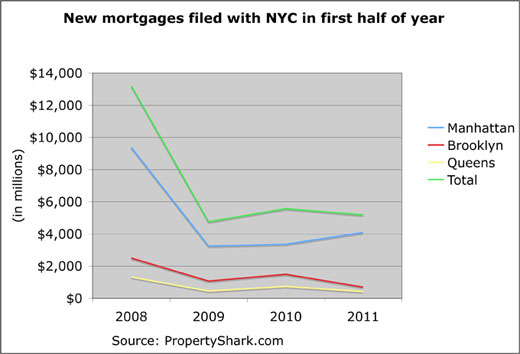

There were $5.2 billion in new commercial mortgages filed with the city through

June 27 of this year for Manhattan, Brooklyn and Queens. That’s down 7 percent

from the same six-month period in 2010, when $5.6 billion in new mortgages

were inked, but up from the first half of 2009, when $4.8 billion in new mortgages

were filed (see chart above).

The anemic rate over the past three years represents an approximately 60

percent decline from the level of the $13.2 billion in new mortgages filed in the

first half of 2008.

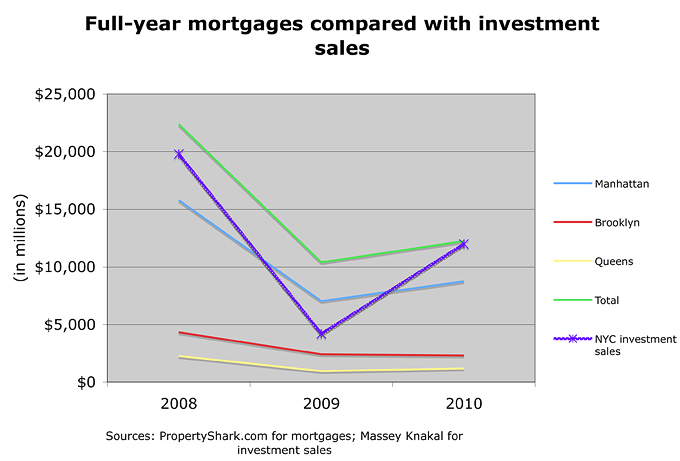

In contrast, investment sales in the five boroughs fell from $19 billion in 2008 to

$4 billion in 2009, then rebounded to $12 billion in 2010, data from investment

sales firm Massey Knakal Realty Services shows (see chart comparing mortgage and sales data below).

PropertyShark.com compiled figures from mortgage documents for commercial

properties filed with the city register. Those documents generally exclude

refinancings and assumptions of debt that are filed under assignments or other

records.

The low level of new debt was counterintuitive, because sales and refinancings

have been strong, real estate insiders said.

Some offered as a possible explanation that buyers are not taking out new debt

to acquire buildings, but instead are assuming the old loans. In many instances,

buyers are acquiring property with less debt, cutting the so-called “overhang”

from the city’s overall real estate market.

“Because of the massive deleveraging that is occurring, the overhang is enough

to absorb the significant increase in transaction volume,” Robert Knakal,

chairman of Massey Knakal, said, based on the PropertyShark.com data.

Gregg Winter, president of commercial finance firm Winter & Company, said part

of the explanation could also be newly tight-fisted lenders.

“I guess part of the reason is that underwriting standards have gotten tougher,”

he said. “So on the one hand it is both harder to get a loan, and loan-to-value

ratios are lower, while on the other hand, buyers and sellers are having difficulty

reaching a meeting of the minds.”

The largest new mortgage debt issued through June 27 this year was for

$281 million on SL Green Realty’s 919 Third Avenue, as part of a $500 million

refinancing arranged by Holliday Fenoglio Fowler.

The largest in Brooklyn was $61 million that Vornado Realty Trust borrowed at

the King’s Plaza Shopping Center in Mill Basin; while the largest in Queens was

a $31 million mortgage secured by four apartment buildings including the 234-

unit property at 47-25 48th Street in Woodside.