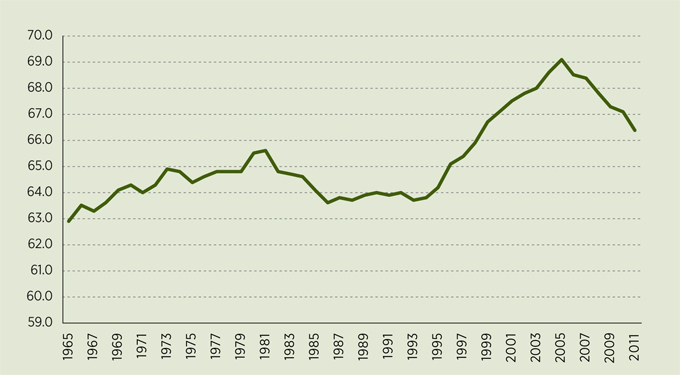

Homeownership rates (source: MBA)

While some bemoan falling homeownership rates as another symptom of the flailing economy, research released today by the Mortgage Bankers Association shows the fall is merely a correction back to historical norms. “The question of why homeownership rates are falling now is really a question of why they were so high during the middle of the last decade,” said Stuart Gabriel, a UCLA business school professor and one of two head researchers on the project.

For three decades, from the late-1960s to the mid-1990s, homeownership rates remained stable between 64 and 65 percent. But in 2004 it reached an all-time high of 69.2 percent, thanks to a combination of loosening mortgage credit standards and an inclination among Americans less than 35 years old to take on more risk compared to their forefathers. Since lenders and investors have taken a more conservative approach following the crash, homeownership rates fell back to 66.4 percent in the first quarter of 2011.

How much further prices decline depends on whether socioeconomic conditions return to their pre-2000 levels. “If underwriting conditions and attitudes about investing in homeownership settle back to year-2000 patterns,” Stuart Rosenthal, a Syracuse University professor and the project’s other lead researcher, argued, “and, if the socioeconomic and demographic traits of the population look similar to those of 2000, then the homeownership rate may have bottomed out and will not decline further.” However the closer these conditions remain to their 2009 levels, the more likely ownership rates fall another 1 to 2 percent.

— Adam Fusfeld