In November, news broke that the shared-office provider WeWork raised $150 million in February 2014 from a number of high-profile investors, including Boston Properties’ Mort Zuckerman. The deal valued WeWork at $1.5 billion and catapulted it into the limelight. It was suddenly a “unicorn,” Silicon Valley-speak for a company that races to a $1 billion-plus valuation based on fundraising.

Over the next few weeks, there was little news from the startup, save for a couple of conference talks by co-founders Adam Neumann and Miguel McKelvey and a new lease signing at the Durst Organization’s 205 East 42nd Street. Then, on Dec. 15, the firm made another announcement: It had just raised an additional $355 million, valuing the company at a staggering $5 billion.

In just nine months, WeWork had tripled in value. It was suddenly worth more than twice as much as global brokerage giant Cushman & Wakefield.

Real estate is a slow-moving business. Skyscrapers take years to build. Families amass fortunes over decades, and hold on to them for generations. By these standards, WeWork, launched just five years ago, is the industry’s equivalent of Usain Bolt.

It has leased more than 3 million square feet of office space globally, with 1.85 million square feet of that in New York, making it one of the city’s largest tenants. But its impact eclipses its physical footprint. Landlords now say WeWork shapes their design decisions, and it’s changed the way startups think about their office needs.

“There are a lot of companies that start out in a WeWork environment, and that has influenced the design of our building,” said Toby Moskovits, CEO of Heritage Equity Partners, of her upcoming Williamsburg office project.

Budding real estate entrepreneurs are also eager to piggyback off the company’s success, with “We’re like WeWork, but for…” becoming a common sales pitch. WeWork, it seems, is everywhere.

But is it here to stay? Some argue that the firm’s lightning growth makes it vulnerable. “I definitely don’t think that now, at an all-time high [for office rents], they should expand,” said Juda Srour, founder of rival shared-office provider Jay Suites. “There’s a huge risk.” Others consider the firm overhyped and overvalued.

So will WeWork continue speeding ahead, or is it bound for a crash? The Real Deal took a closer look at the budding giant to get to the bottom of its business, its numbers and its prospects for the future. What emerges from talks with insiders, onlookers and investors is the portrait of a company that is less vulnerable than one might think.

Strength in numbers

If you think $5 billion seems like a lofty valuation for a startup, you’re not alone. “I don’t understand their valuation,” said a real estate tech entrepreneur who spoke on the condition of anonymity. “They seem to be valued the way a tech company is valued, but they are a commercial real estate company.” Even Neumann, in An Interview With The Wall Street Journal, acknowledged that if it were viewed as a traditional real estate concern, its valuation wouldn’t be as steep.[vision_pullquote style=”1″ align=””] “They seem to be valued the way a tech company is valued, but they are a commercial real estate company.”- Venture investor unaffiliated with WeWork [/vision_pullquote]

WeWork declined to provide any information for this article, and doesn’t disclose its earnings, but sources said it is valued around 100 times earnings. That’s an extraordinarily high price tag. SL Green Realty, the city’s largest commercial landlord, currently trades at 20 times its earnings. Regus, the world’s largest shared-office provider and a WeWork rival, trades at 34 times earnings. The average for all stocks listed on Nasdaq is 23.

And yet, the valuation is hardly an outlier during a venture-funding boom that has some observers worrying about a new dot-com bubble. “At least from a dollars and cents perspective, we’ve seen crazier things,” said a partner at a venture capital firm that hasn’t invested in WeWork but holds stakes in other real estate tech startups. Another venture investor, also unaffiliated with WeWork, said the valuation is high but “could be very justified” in the long run.[vision_pullquote style=”1″ align=””] “At least from a dollars and cents perspective, we’ve seen crazier things.” – Venture capitalist unaffiliated with WeWork [/vision_pullquote]

Tech startups attract funding based less on their current earnings and more on the promise of future growth. And if Neumann has his way, the growth will be immense. “In the next five years, we’re going to take over more than 50 million square feet [of office space],” he said at TechCrunch’s Disrupt conference in May.

WeWork rents out large tracts of office space with terms of 10 to 15 years, and then sublets small chunks to firms on a month-to-month basis. In exchange for this flexibility, as well as a plethora of amenities and networking opportunities, WeWork’s customers, dubbed members, pay a significant premium.

Zachary Ehrlich, founder of brokerage Mdrn., estimates he pays up to $200 per square foot at WeWork’s 261 Madison Avenue location. WeWork pays rents starting in the low-$40s per square foot for the space, according to real estate data firm CompStak. This likely allows for a comfortable profit margin, even after accounting for the company’s large investments in renovations, on-site management and amenities.

In some cases, landlords provide WeWork with discounted space in exchange for its commitment. Rudin Management, for example, gives WeWork a discount at 110 Wall Street. Michael Rudin, a vice president at the family firm, argued this makes business sense because WeWork is leasing the entire 300,000-square-foot building — which was previously 60 to 70 percent occupied — and is assuming much of the cost of renovation.

[vision_pullquote style=”1″ align=””] “In the next five years, we’re going to take over more than 50 million square feet [of office space].” – Adam Neumann, WeWork [/vision_pullquote]

“At the end of the day, we have this growing company that’s taking the entire building and doing a nice buildout, and we are spending significantly less than we would have with a complete repositioning,” Rudin said. “Worst case, if WeWork went out of business, we would be left with a better building than before Hurricane Sandy.”

From left: 110 Wall Street and Michael Rudin

WeWork is getting similar discounts at a minimum of six of its 15 current New York locations, according to CompStak. Observers reckon each location generates millions in profits for the company, and its potential for profitability only increases with each new location, as does the appeal of its much-touted member network. Jason Bauer, whose brokerage Voda Bauer is headquartered at a WeWork space on East 42nd Street, said the rent premium he pays is more than offset by the business he gets from other WeWork members. Voda Bauer is WeWork’s official residential partner in New York, giving it first crack at a huge pool of potential clients.

From left: Goldman Sachs’ Lloyd Blankfein, Benchmark’s Bruce Dunlevie, Mort Zuckerman and JP Morgan Chase’s Jamie Dimon

The founders’ unusual backgrounds — Neumann grew up on a kibbutz in Israel, McKelvey in a five-mother collective in Oregon — led WeWork to place huge emphasis on community, something that has clicked with investors.

“I thought they really did think not just about real estate space but about establishing a community, which I thought then and still think now would attract a lot of people,” Mort Zuckerman, co-founder and chair of Boston Properties, told TRD. He said he chose to invest based on his belief in both WeWork’s business model and in Neumann, whom he described as “enjoyable,” “inspiring” and having “a great feel” for his work.

“I am, shall we say, very happy (with the investment),” Zuckerman added.

The test to come

Rapid growth and glowing assessments like Zuckerman’s have led many to conclude that the future belongs to WeWork. It’s certainly managed to attract top talent. Recent hires include Arthur Minson, former CFO of Time Warner Cable, Michael Gross, former CEO of Morgans Hotel Group and Todd Bassen, former head of New York acquisitions for Invesco.[vision_pullquote style=”1″ align=””] “I am, shall we say, very happy (with the investment).” – Mort Zuckerman, Boston Properties [/vision_pullquote]

But doubts persist about its ability to weather a downturn. WeWork is signing long-term leases at historically high rates, despite the favorable terms it may get. Will it still be able to charge members, who have no long-term commitment, the rates it needs to stay profitable if the real estate market, or the economy as a whole, tanks?

From left: Todd Bassen and Arthur Minson

At an April event in Brooklyn, McKelvey addressed this question, as first reported by Bloomberg.

“Everyone said our business wouldn’t succeed then because it’s a downturn,” he said, referring to WeWork’s predecessor Green Desk. “And now they’re saying it won’t succeed because it’s a bubble. I think that whole idea is bullshit. Because as we all know sitting in this room, the world has changed completely.”

A third venture investor unaffiliated with WeWork, also speaking on the condition of anonymity, said he goes “back and forth” on the question of the company’s viability.

“Because you look at their spaces,” he continued, “and it’s all these small businesses, and if there’s a major downturn in the economy, do they get fucked? I don’t know, because it seems like there are not just tech startups there. I think they’ve done a pretty good job of building out their diversity.”[vision_pullquote style=”1″ align=””] “Because you look at their spaces,” he continued, “and it’s all these small businesses and if there’s a major downturn in the economy, do they get fucked?” – Venture capitalist unaffiliated with WeWork [/vision_pullquote]

WeWork is often portrayed as a haven for tech startups, but that’s only partially correct. Walking through the hallways one is also likely to see lawyers, flacks, budding hoteliers and tailors, among others. What is true though, is that small businesses make up the bulk of WeWork’s membership.

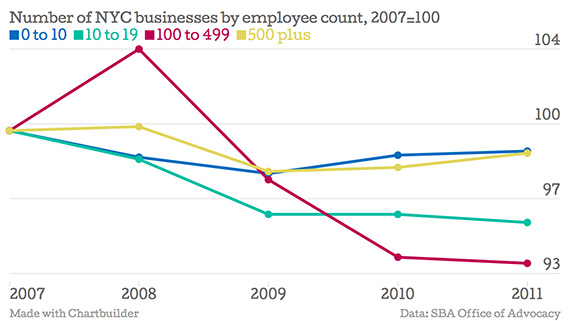

Conventional wisdom says that small firms are vulnerable to downturns. However, a look at the available data shows that heavy reliance on small businesses may not be a disadvantage during tough economic times – on the contrary.

The chart above shows changes in the number of businesses by employee count between 2007 and 2011, based on research from the federal Small Business Administration. The data show that small businesses didn’t disappear at a higher rate than their larger counterparts during the economic crisis that began in 2008. In fact, firms with between 100 and 499 employees saw the steepest decline. Meanwhile, the number of firms with less than 10 employees, which make up a large chunk of WeWork’s members, barely declined. Simply put, for every small firm that folds, a large firm downsizes enough to keep the total number of small firms more or less constant. The takeaway: Demand from small firms for shared office space is unlikely to fade in an economic crisis.

[vision_pullquote style=”1″ align=””] “Everyone said our business wouldn’t succeed then because it’s a downturn. And now they’re saying it won’t succeed because it’s a bubble. I think that whole idea is bullshit. Because as we all know sitting in this room, the world has changed completely.” – Miguel McKelvey, WeWork [/vision_pullquote]

This is exactly what Regus experienced in 2009. “They did extremely well during the last downturn, when a lot of people were downsizing, especially in the financial sector,” said CBRE’s Mark Ravesloot, who has represented Regus in New York for nearly a decade. Firms tend to be wary of making long-term overhead commitments during a crisis, he said, meaning many prefer short-term leases despite them being pricier. Moreover, staff reductions mean the demand for the kind of shared services — such as accounting, legal and IT — provided by WeWork and Regus is likely to grow.

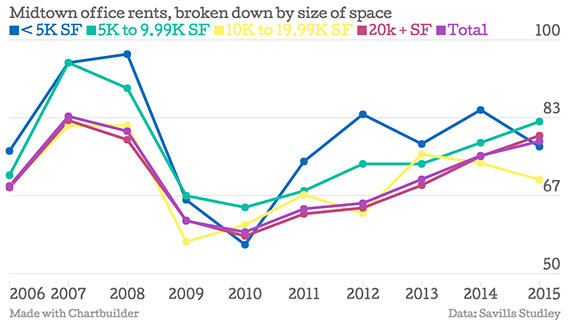

Midtown office leasing data compiled by Savills Studley corroborates Ravesloot’s observation. The chart below shows average asking rents between 2006 and 2015 broken down by office size. Offices with less than 5,000 square feet saw rents dip significantly in 2009 and 2010, but the decline was short-lived. In comparison, rents for larger office spaces recovered far slower in 2010 and 2011.

Still, no two crises are equal, and just because Regus fared well during the last downturn doesn’t mean WeWork will do as well during the next one.

According to Ravesloot, Regus tends to sign leases during market troughs, when rents are cheaper, and has remained reluctant to commit to large chunks of space in Manhattan over the past year. WeWork, on the other hand, is piling on leases at peak pricing. But expanding during a boom comes with a big plus: it has arguably never been easier to raise capital.

To date, WeWork’s founders have raised nearly $570 million from investors, according to CrunchBase. And they’ve given up at least a 37 percent ownership stake, according to PitchBook, a data firm that tracks private capital markets. No other real estate startup raised even remotely as much. While WeWork looks to be investing a sizeable chunk of that money in its expansion, it will also be able to set aside cash reserves. This, observers say, boosts its ability to weather a downturn despite the high rents it pays.

Stewart Butterfield, CEO of the corporate-messaging app Slack, said in a recent New York Times interview that raising as much capital as possible now makes sense for startups because it makes them more resilient to vagaries of the market. “It’s a hedge, and a hedge that’s unbelievably good for us,” he said. “In the case where everything turns to [expletive], we will look pretty smart.” This argument applies to WeWork as well.

So, with fat cash reserves and a rapidly-growing customer base, WeWork is likely to stay hungry. Just how big can it get? Take it from McKelvey. On a recent Thursday, he sat on a panel in blue jeans, bright green sneakers and a green plaid shirt. When the moderator said in passing: “I don’t know how much more space you’re going to acquire in New York City,” McKelvey interjected, jokingly: “All of it.”