TRD Special Report:Sporting a Nehru jacket and addressing an audience that included Indian Prime Minister Narendra Modi, Adam Neumann made it clear he didn’t want his company to be thought of as a number. Even if that number was $16 billion.

“For such a spiritual country, I’m surprised from the amount of talk I heard about valuation, and raising money, and bubbles, and building big companies — that is not the goal,” Neumann, the co-founder and CEO of WeWork, said in January at the launch of the Startup India initiative in New Delhi. “The goal is finding something you truly love. Make sure it has intention behind it. Make sure it’s going to Make The World A Better Place. Put those two things together, and I swear to you, success will follow, the money will follow and you will change the world.”

WeWork provides flexible office and communal living space. But that’s not what you hear from Neumann. His fundamental business, he told the New York Times in 2014, is creating “a community that empowers people everywhere to do what they love.”

It’s easy to dismiss all this lofty talk as Adam Neumann being Adam Neumann – a dreamer with a penchant for the grandiose. But WeWork’s claim of enabling a “We Generation” (the wording changes) isn’t just a shtick. It’s a key reason why investors pumped $1.4 billion into the company.[vision_pullquote style=”3″ align=”right”] “The goal is finding something you truly love. Make sure it has intention behind it. Make sure it’s going to Make The World A Better Place.” – Adam Neumann [/vision_pullquote]

WeWork’s investors believe the company isn’t simply in the leasing business, but rather creating a global community of innovators. They believe this community gives WeWork moat (or long-term competitive advantage) and will keep it enormously profitable. That, in their minds, justifies a valuation that makes WeWork one of the world’s 10 richest startups, worth more on paper than shared office giant Regus, ride-sharing company Lyft, and major hotel firms like Starwood Hotels & Resorts.

But are they right? Fears over a bursting tech bubble are adding scrutiny to WeWork’s valuation. In the first half of the year, several billion-dollar startups announced mass layoffs, and some saw their valuations slashed considerably. The valuations of Dropbox and Zenefits, for example, fell by 42 and 62 percent respectively over the past year, as per mutual funds that invested in them. Some worry WeWork may be next in line.

“No schmucks and no assholes”

Few questions are as hotly debated in the worlds of real estate and venture investing as how on earth WeWork – founded in 2010 and valued at $1.5 billion a mere two years ago – is now worth $16 billion.

“Candidly, this question baffles me,” said one unaffiliated venture investor who spoke on condition of anonymity. “I’ve talked about it with a bunch of people in the tech and real estate industry and they’re all asking the same question.”

Even its biggest skeptics will admit the company has a lot going for it. Co-working is a booming field, and WeWork’s spaces are all the rage among freelancers and startups. Big companies, too, are embracing co-working to expand into new cities without making costly long-term commitments. And unlike many other real estate startups — the words “pre-revenue” are uttered so often they’re now printed on t-shirts — WeWork has been profitable for years. In New York, it leases space on 15- or 20-year terms, in some cases for as little as $30 per square foot, according to office leasing database CompStak, and sublets desks and enclosed offices for anywhere between $450 and $1,700 per month and person.

“Adam always says, ‘No schmucks and no assholes,’” Vornado Realty Trust’s Steve Roth said while toasting Neumann in 2014, according to Fast Company. “But the definition of a schmuck is someone who rents a property at .5x and then that guy turns around and rents it at 1.5x.”

According to a leaked internal document from late 2014, WeWork’s EBITDA that year was $14 million – or 19 percent of revenues. At the time, it forecasted nearly $1 billion in profit on revenues of $3 billion by 2018. Newer numbers aren’t public, but it’s likely that the company’s profits have grown as it adds more locations and builds up economies of scale.

WeWork also has high hopes for its new WeLive division, which offers customers rooms or beds in co-living spaces. In the 2014 document, the company projected WeLive membership will account for 21 percent of its revenues by 2018.[vision_pullquote style=”3″ align=”right”] “But the definition of a schmuck is someone who rents a property at .5x and then that guy turns around and rents it at 1.5x.” – Steve Roth [/vision_pullquote]

The company now has 109 locations in 30 cities – compared to the 32 locations it had last May. It recently expanded to China and has designs on India. Even if its growth slows somewhat, it could become a global behemoth with hundreds of co-working and co-living locations by the end of the decade.

In the 2014 document, WeWork projected it would reach 260,000 members by 2018 — more than four times its current figure of 60,000. But even if it hits that mark, the question remains whether it’s enough to justify its valuation.

Tech investors who chip in at a $16 billion valuation will generally value the firm at more than twice that, another unaffiliated venture investor said, because they’re normally looking for a 100 percent return when making such a risky investment.

The caveat: Late-round venture investments often come in the form of preferred equity or carry guaranteed returns. If that was the case in WeWork’s latest round – neither WeWork nor its investors commented on the matter – the valuation could be lower.

But if the latest funding round was straightforward equity, its newest investors may well believe that WeWork is a $40 billion or even $50 billion company.

Sharing is hard

Co-working and co-living are capital-intensive fields. WeWork has to spend months and millions building out its spaces. In comparison, Airbnb or Uber, which require very little physical infrastructure investment to launch in a new city, can grow much faster.

WeWork is also prone to cyclical risk. If the number of small businesses tumbles during an economic downturn and fewer young professionals can afford $1,500 per month for a glorified dorm bed, its revenues could take a serious hit.

And barriers to entry are low. Any entrepreneur or landlord with a little money can open a co-working space – and just that is currently happening all over the world. In New York, the Flatiron and NoMad districts alone are home to more than 20 different co-working companies, while startup Common is competing with WeWork in the co-living market. Co-working providers have sprouted up in every major U.S. metropolitan city, and in emerging economies such as India and China. As an early entrant of impressive size, WeWork has brand recognition and economies of scale going for it. But it would be naïve to assume all that competition couldn’t put a dent in its profitability down the line. Case in point: the company recently began offering discounts in an attempt to lure members to certain locations in Lower Manhattan, according to leaked offering materials (WeWork claims it has long had a policy of offering promotional discounts, and that the latest discounts are not a sign of weakening demand).

Capital-intensive industries with high cyclical risk and low barriers to entry generally aren’t wildly profitable in the long run. That’s why public companies most similar to a co-working provider aren’t valued too highly relative to their size. Regus, a shared-office company that, like WeWork, rents office space and sublets it on a short-term basis, is valued at just $3.49 billion. That’s despite having 2,768 global locations, 2.3 million customers and £1.93 billion ($2.55 billion) in revenue last year.

Or take large hotel companies – which, like WeWork, make long-term commitments to buildings and rent out rooms on a short-term basis, while also offering plenty of amenities. Marriott International operates 4,400 hotels globally and had revenues of $14.5 billion last year. But with a market capitalization of $17 billion it is valued just a shade higher than WeWork.

There are two likely reasons why investors value WeWork so much higher than Regus or Marriott (after controlling for sheer size). One is that they expect it to become even bigger. A source close to the firm reckons it can hit 100,000 members in New York alone. That’s over 1 percent of the city’s population. Extrapolate that market share to other cities, and you can see how WeWork and its investors think its membership could one day hit millions.

Investors also think the company will get a lot more profitable. In 2015, Regus and Marriott had operating margins of 8.3 and 9.3 percent, respectively. In 2014, WeWork projected margins of 38 percent by 2018. (In the leaked document, it estimated that its spaces break even at 55 percent occupancy, compared to 80 percent for Regus.)

So what makes WeWork different, and how does it expect to become both so big and so outrageously profitable? Here’s where Neumann’s We Generation mantra comes into play. The company, it claims, is in the community-building business. And that’s where the money is.

Better together

“People often ask: who are we competing against? Are we competing against other co-working spaces? I don’t think that at all,” Artie Minson, president of WeWork and former CFO of Time Warner Cable, said at a TRD event in May. The global community of customers WeWork is building, he argued, makes it “fundamentally different” from companies that run individual co-working spaces.

“In certain [WeWork] buildings about half the people are doing business with each other in any given month,” he said. “And so as we are able to expand the community globally, there’s a network effect among the businesses and a network effect on the community.” The bigger the community grows, the argument goes, the more valuable it becomes for its members, the harder it will be for startup rivals to imitate it, the more WeWork can charge for it, driving up its profits.

Any competitor can toss in ping-pong tables and beer kegs and open a co-working or co-living space where its tenants can work, live and mingle. But it’s a lot harder to copy WeWork’s app – a sort-of Facebook-meets-Linkedin for its members across the world.

WeWork argues that the access the app provides to a global network of potential customers, employees and business partners creates enormous value for its members. And it believes people are so keen to be a part of that network that they will pay a premium for WeWork membership, something they call the “WeWork effect.”

In a June interview with TRD at WeWork’s Chelsea headquarters, Minson said the network effect is only part of the game. Scale is also crucial.

“Similar to the media and cable industry that I came out of, WeWork is a business where scale matters,” he said. “As we continue to scale WeWork, things that will continue to differentiate WeWork are having the most robust community, the best employees and the most innovative technology, design and service. Coupling these with our strong balance sheet make us a great partner for landlords.”

And its name and cash reserves also allow WeWork to negotiate better terms with landlords.

“That gives people a better comfort in negotiating a lease,” said Bill Rudin, whose company Rudin Management leased out an entire office building on Wall Street to WeWork and is partnering with it on a ground-up project in the Brooklyn Navy Yard.

Still, investors’ faith in the power of the network effect could arguably have a bigger impact on WeWork’s sky-high valuation than economies of scale or branding. Companies who enjoy the benefits of scale have a leg up over smaller rivals – but they still tend to face competition, which keeps a lid on profits. Think of Starbucks versus smaller coffee shop chains like Peet’s or Gregory’s.

But it’s much harder to compete with a company that enjoys substantial network effects. Think of Facebook and, well, no one. That’s why networks can become more profitable, and are more prized by investors.

“The right comparables are Uber and Airbnb,” said Michael Eisenberg, an early investor in WeWork. Both Uber and Airbnb are technology-based companies that used network effects to build near-monopolies in their markets.

But there are ways to compete. Consider Uber vs. Lyft: Uber typically enters new markets such as China as Uber, taking on all the infrastructure and regulatory headaches that come with it. Lyft, however, which has also been prolific at raising venture funds, forms alliances with established players in markets it wants to break into. In China and India, it partnered with Didi Chuxing and Ola respectively, allowing its customers to use Lyft to access Didi and Ola’s network of drivers. It is conceivable that in the near future, a WeWork competitor with global ambitions might seek to do the same.

Amarit Charoenphan, who runs the co-working company HUBBA in Thailand, said entering new markets with different cultures will be a challenge for WeWork. “They will basically have to start from zero and face competition that understands the local market very well,” he said. Charoenphan acknowledged WeWork’s global network holds appeal to its users, but dismissed the suggestion that it puts it beyond competition. “There’s room for many (companies),” he said. “It’s just like you can’t have one hotel operator in one city.”[vision_pullquote style=”3″ align=”right”] “The right comparables are Uber and Airbnb.” – Michael Eisenberg [/vision_pullquote]

Ritesh Malik, who runs the co-working company Innov8 in India, says he offers a cheaper alternative to WeWork membership. Ultimately, he argued, there will be enough space for both WeWork and plenty of competitors in India.

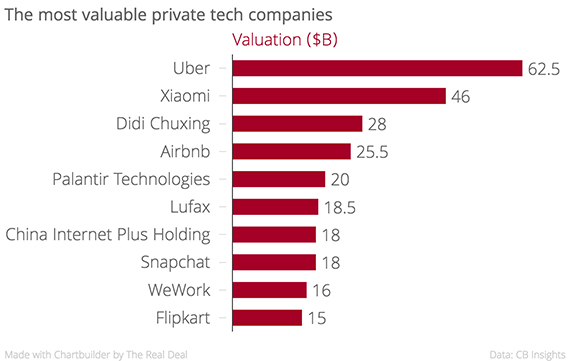

Investors love companies that enjoy network effects because they tend to create moat, or the ability to eventually jack up prices and profits. As of July 5, Facebook is valued at $326.4 billion, Amazon at $348.4 billion, Uber at $62.5 billion and Airbnb at $25.5 billion.

“When people invested in Facebook at a $10 billion valuation people thought they were totally nuts,” Eisenberg said. “I don’t think [investors] have a lot of regrets about that.” He believes WeWork will build plenty of moat in part through its global community, and in part by offering frequent international business travelers a uniform experience across countries.

Minson, too, evoked the world’s richest startup to put WeWork into perspective.

“It’s similar to people saying how could Uber’s valuation make sense relative to General Motors valuation. Well, Uber is not a car company,” he said. “It’s a product company that happens to use automobiles to deliver its product. Real estate is one of the ways we basically deliver a community lifestyle.”

The “WeWork effect”: myth and reality

Illustration by Bennett Klein

WeWork’s rosy profit projections, for one, bear further scrutiny.

In the 2014 document, the company projected it would be able to increase the average monthly membership fee from $578 in 2014 to $767 by 2018, presumably bolstered by the “WeWork effect.” But what if the opposite will happen?

Rising competition or a downturn in the real estate market or broader economy could put a dent into profits. Saddled with expensive long-term leases, a drop in demand from its short-term users could create serious financial problems.

WeWork’s executives like to counter that the company was founded during a downturn and that demand for flexible office space may even grow in hard times as companies downsize. They do have a point: as TRD reported last year, census data shows that the number of small businesses didn’t drop as dramatically as the number of large businesses during the Great Recession, and bounced back quicker in the aftermath. Moreover, a source who has reviewed some of WeWork’s lease deals signed in 2014 or earlier said they contain more lenient exit provisions than typical lease agreements.[vision_pullquote style=”3″ align=”right”] “It’s similar to people saying how could Uber’s valuation make sense relative to General Motors valuation. Well, Uber is not a car company.” – Artie Minson [/vision_pullquote]

But every downturn is different, and WeWork’s estimate that its occupancy will only fall to 85 percent during a downturn is certainly optimistic.

“Comparing your occupancy levels now to a pre-WeWork downturn doesn’t make sense,” said Michael Mandel, CEO of CompStak. “They’ve created a completely new industry.”

“In a downturn they have huge lease obligations and it’s not like an asset they can sell,” he added. “They are going to be in a worse position than if they owned all these places.” Regus, for example, was forced to declare bankruptcy in the U.S. in 2003, after the bursting of the dot-com bubble hit its customer base hard.

Despite his skepticism, Mandel is bullish on the company overall and believes it will continue to grow at a strong pace as long as the broader market remains healthy. While he declined to say whether WeWork is over- or undervalued, he said the valuation “seems high”.

In cities where WeWork opened more locations, membership cancellations declined, Minson said. This he takes to be proof of the company’s network effect: members like it more as it gets bigger.[vision_pullquote style=”3″ align=”right”] “They are going to be in a worse position than if they owned all these places.” – Michael Mandel [/vision_pullquote]

But correlation doesn’t imply causation, and some observers are skeptical that the network and app are really a game changer. “There are some people who talk about it as a technology company,” said Nizar Tahuni, an analyst at Pitchbook, a research database that tracks venture investments. “But they are in no way, shape or form a technology company. If I get an apartment and sublease it to someone else and I make money, I’m not a technology company.”

“There’s a lot of value to [the app], obviously, but at the end of the day the person who goes to WeWork is not going to sign up to get the social aspect, but because it makes sense on per-square-foot cost basis,” he added.

One London-based WeWork member said via email: “The value of the network is not to me enough to differentiate it from a Regus.”

Chris Fischer, head of engineering at real estate data company Reonomy, said being able to work in similar spaces in different cities was the “main differentiator” that made him pick WeWork when he was an executive at imaging company Shutterstock. The app, not so much.

Neumannism

According to Pitchbook, WeWork has authorized issuing preferred shares equivalent to about 42 percent of the company – a metric that helps estimate how much of the firm is owned by investors.

If some of these investors initially had doubts, Neumann dispelled them. Several sources credit the co-founder’s charisma as a key reason for the firm’s fundraising success. Ask any WeWork champion why they believe in the company, and they will almost inevitably say: “Have you met Adam?” Last year, Boston Properties founder Mort Zuckerman told TRD that he chose to invest in WeWork in large part because of Neumann, whom he described as “enjoyable,” “inspiring” and having “a great feel” for his work.

“He’s almost like a messiah,” said Bruce Mosler, chairman of global brokerage at Cushman & Wakefield.

A lanky, scratchy-throated Israeli émigré that once sold baby clothes, Neumann has become synonymous with WeWork much the way Elon Musk is with Tesla or Mark Zuckerberg with Facebook. Like them, he has a compelling origin story — if Musk is the genius with the tortured childhood and Zuckerberg the geek boy wonder, then Neumann is the spawn of a kibbutz who can’t help but lead. And like them, he’s become the poster child for innovation in his industry — Fortune placed him at the top of its “40 under 40” ranking in 2015.

Grant McCracken, a business psychologist at the University of Toronto, said a charismatic chief can have the effect of “persuading people to put their shoulder to the wheel” — or, by extension, investors to open up their wallets. But it also has a potential downside. Once a company gets used to a leader’s charisma, it “constantly has to be applied” to keep the firm going, McCracken said. Firms that aren’t as dependent on a single figure tend to be more stable in the long run.

In a 2002 essay titled “The Curse of the Superstar CEO,” Rakesh Khurana, a professor at Harvard Business School, went a step further. “Like its close relative, romantic love, charisma can be blinding,” he wrote. “And the consequences of that blindness can be severe.” Consider Shai Agassi, another charismatic Israeli, whose electric car startup Better Place raised nearly $1 billion from investors and was the toast of the world before failing in spectacular fashion.

Does Neumann care? The entrepreneur, whose net worth Forbes pegs at $1.5 billion, is happy to prove doubters wrong. When he was a student at Baruch College, he entered an entrepreneurship company with a proposal for a co-living startup. But he didn’t even make it past the first round.

“I went to the dean of the college and I said, ‘I don’t want to contest, but why didn’t I make it?’” he recalled in a recent interview with CBS. “And the dean said, ‘Adam, no young entrepreneur could ever raise enough money to change the way people live.’ And the only lesson I think that’s there for teachers: you never know who you’re talking to.”