Emily Allen was sure her seventh offer on a home in Phoenix, Arizona, where she and her husband, Ryan, planned to move from San Diego, would be the charm. The couple bid $70,000 above the listing price, waived the appraisal and agreed to a 14-day close.

It wasn’t enough.

“I was convinced we were going to get it, and we were like the fourth-best offer,” she said.

Unfortunately for the Allens, both 27, they were far from the only newcomers to Phoenix’s housing market, where prices jumped more than 32 percent last year. A wave of outside buyers — many of them young families — has drastically reduced the area’s once-excessive housing supply from more than 19,000 active listings in 2016 to a mere 4,500 in April, according to Federal Reserve data.

Phoenix is emblematic of a broader pattern across the country. Millennials, ready to move beyond rental apartments or their parents’ houses, entered a market in which home-building activity had never fully recovered from the Great Recession. Increased demand brought on by low interest rates and the freedom of remote work, coupled with supply chain issues that have frustrated development timelines, only made finding a home more difficult — and expensive.

The result is what economists and advocates are calling a bubbling affordability crisis. Housing prices nationally increased 18.8 percent last year, according to the Case-Shiller home price index — the highest jump in 34 years. Twenty U.S. cities broke all-time records for price increases.

“It remains to be seen how long buyers can weather this storm,” Zillow economist Jeff Tucker wrote in an email.

The dearth of supply has its roots in the 2008 financial crash, which prompted cautious investment in new inventory. Nationally, permitting for new privately owned housing units bottomed out in March of 2009 and did not recover to pre-recession levels until about January 2020. New housing starts still have yet to fully recover.

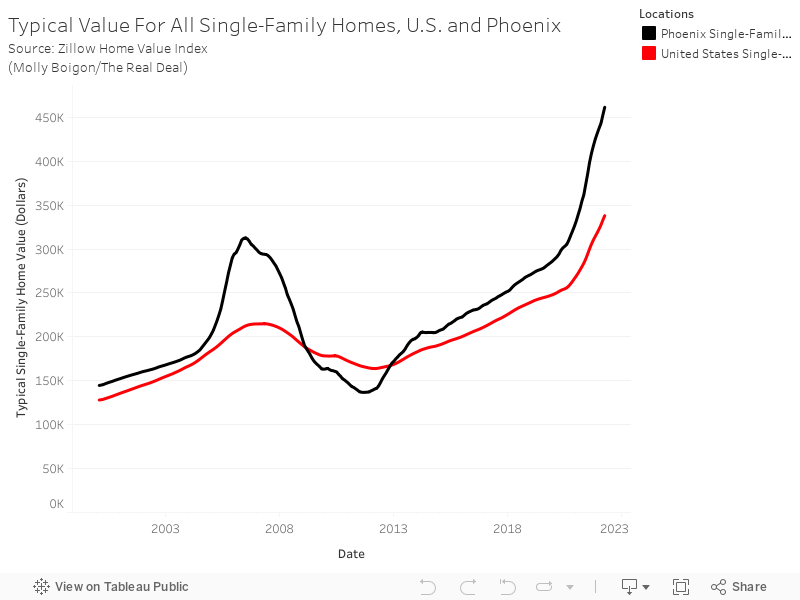

Phoenix has seen a similarly precipitous drop. In July 2004, nearly 6,000 permits were issued for single-family homes. In June 2006, the peak, a single-family home in Phoenix sold for an average of $312,171, according to Zillow.

But both sales and inventory took steep nosedives after the housing bubble burst. In February 2009, only 317 permits were issued for single-family homes. In August 2011, the average single-family home price bottomed out at $136,517.

Permitting did not return to pre-crash levels until September 2020, and by March of this year, the average price of a single-family home had soared to a record $478,000.

Permitting did not return to pre-crash levels until September 2020, and by March of this year, the average price of a single-family home had soared to a record $478,000.

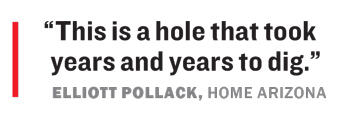

“For the last 13, 14 years, we have built fewer units than there have been household formations,” said Elliott Pollack of the housing advocacy group Home Arizona. “This is a hole that took years and years to dig.”

Now, that hole is getting deeper as both Millennials and large employers, such as a plant that will produce 20,000 semiconductor chips a month starting in 2024, settle in the Salt River Valley area, which includes Phoenix, Mesa and Scottsdale, among other cities.

Maricopa County, which contains Phoenix and more than half the state’s population, gained nearly 87,000 residents from July 2019 to July 2020, according to Census data, more than any other U.S. county.

“I love working with first-time homebuyers, because they’re so excited about the process, but right now they’re fighting with 15 other people for a house,” said Sindy Ready, a broker with a local Re/Max affiliate and treasurer of the Arizona Association of Realtors. “I kind of joke with my Millennials like, ‘Alright, you have to put your armor on and we’re going to go to battle.’”

As construction activity ramps up, supply chain issues have made it difficult for builders to bring new homes to market. Materials like lumber and even garage doors are caught up in months-long delays, driving up prices.

Prices for construction materials broadly increased more than 35 percent last year, the highest year-over-year jump on record, according to data from the Bureau of Labor Statistics.

Desperate to stockpile materials, builders are even reaching out to empty big-box retailers for increasingly scarce warehouse space, Amy Rodbell, an industrial broker for Newmark, told Construction Dive.

“We have builders who are trying to build as fast as they can, but they’re affected by supply chain issues, labor issues and a struggle to find adequate land for new development,” said Mark Stapp, who heads the real estate development master’s program at Arizona State University.

A growing cohort of investors are also squeezing the supply of existing homes. In the fourth quarter of last year, investors purchased a record-high 18.4 percent of all homes bought nationwide, according to data from Redfin. Phoenix’s share of investor purchases was even higher, at 28.4 percent, trailing only Atlanta, Charlotte, Jacksonville and Las Vegas. Many of these investors are buying single-family homes not to sell them to families, but to rent them.

Not by happenstance, rents have also risen sharply in the U.S. since last summer, and Phoenix is no exception. The average asking rent for a one-bedroom apartment in the city jumped nearly 30 percent last year, according to data from Zumper. An expected rise in interest rates will only put more homes out of reach for potential buyers, driving further competition in the rental market.

“The freefall has started, in terms of affordability,” said Home Arizona’s Pollack. The home-price surge has started to abate, largely because of rising mortgage rates, but prices are still increasing by double-digit percentages in year-over-year comparisons.

As one of numerous Millennials fighting to get into the Phoenix market, Allen feels the search has taken its toll. She said she’s thought twice about telling her friends and family when she and her husband are about to put in an offer.

“I feel like maybe I’m jinxing it,” she said.

She said she checks Redfin every 30 minutes for new listings. A $700,000 budget would be comfortable for Allen, a part-time nanny whose husband works as a sales director at a software company. Now, they’ve pushed their budget to $750,000. The rapid increase in prices has been devastating, she said.

“We look at like, this house sold for $200,000 less than what it’s selling for now literally 18 months ago,” she said. “That is like a dagger to the chest.”