TRD Special Report:In March, Gary Barnett [TRDataCustom] went to Israel on a firefighting mission. On the Tel Aviv Stock Exchange, yields on Extell’s bonds had soared to 16 percent, effectively turning them into junk bonds, and Barnett’s Israeli investors were spooked by Manhattan’s struggling high-end condo market.

Of particular concern to Extell’s backers were two of the company’s most ambitious new developments, One Manhattan Square (1MS) on the Lower East Side and Central Park Tower (CPT) on Billionaires’ Row. Barnett was seeking over $2 billion in debt and equity for the two projects, a lofty goal with condo prices slipping and banks wary of financing new luxury developments. And even if he could find the money to build his glitzy towers, where would the buyers come from?

Barnett flew to Tel Aviv in an attempt to calm his investors’ nerves. But according to multiple sources, he did a lousy job of it.

“He just put more fuel to the fire,” said Shahar Keinan of Brosh Capital, an Israeli hedge fund that deals in distressed corporate bonds and jumped in to buy some of Extell’s. “He didn’t say, ‘Everything is going to be okay, don’t worry.’ He said, ‘There are risks, I can’t guarantee anything.’”

“Sometimes, it’s not the message, it’s how you wrap it and say it to the bondholders,” said one source familiar with the Israeli bond market. What Barnett said “was the last thing that investors wanted to hear.”

In an interview with The Real Deal this September, Barnett took issue with that characterization: “I was not pessimistic, I was cautionary,” he said. “I wanted to let people know what the risks were.”

Six months after that trip, however, Barnett seems far more optimistic — and it’s easy to see why. Since August, he’s locked down more than $1 billion in financing for the two projects. For 1MS, he scored a $300 million mezzanine loan from Scott Rechler’s RXR Realty and a $500 million construction loan from a consortium led by Deutsche Bank and Natixis. For CPT, commonly referred to as the Nordstrom Tower for the department store that will anchor it, he scored approximately $300 million in equity from SMI USA, the U.S. subsidiary of Shanghai’s largest state-owned enterprise.

On his return to Israel in September, Barnett “talked a different tune,” Keinan said. “He thinks the situation has improved dramatically. He thinks he will gain back the trust here in Israel.”

Yields on Extell’s bonds have improved to the mid-10 percent range since March.

Pulling rabbits out of hats is nothing new for Barnett. He had the chutzpah to build the ultra-luxury One57 in the thick of the downturn, and wrested control of a valuable Midtown South office portfolio that rivals had given up for dead.

“He was building One57 right in the teeth of the 2008 Lehman collapse,” said Donna Olshan of Olshan Realty. “If there’s money in the world, he knows how to find it.”

This time around though, his task is even tougher: There’s a nearly $200 million financing gap at 1MS and a $900 million construction loan to source for CPT, which would be one of the largest issued to a New York developer this cycle. And he’s got to find the funds at a time when lenders are shutting up shop.

In addition, the SMI deal has come under scrutiny by investors wary of the harsh conditions it imposes on Extell: if Barnett can’t meet SMI’s financing deadlines, the Chinese behemoth wants its money back.

Barnett’s playing a high-stakes game of real estate Tetris, and to win he’ll need not only to source capital, but to shift it into the right places at just the right times. As a poster child for savvy investments and calculated long-term assemblages, there’s a belief among industry insiders that his successes — or failures — will set the tone for the market in the months to come.

“Gary’s an entrepreneur, but like a crazy one,” Keinan said. “Everyone told us, ‘If there is someone who can pull it off, it will be Gary.’ But even for him, it’s a stretch.”

Smizing

A rendering of Central Park Tower (Credit: New York YIMBY)

Extell completed its first offering on the Israeli bond market in 2014, eventually raising a total of $400 million at roughly 6 percent, much cheaper than could be found at home. One headache that came with the cheap debt, however, was the level of transparency that the mandatory public disclosures have imposed on Extell — scrutiny that some developers find disconcerting.

[vision_pullquote style=”3″ align=”right”] “Gary’s an entrepreneur, but like a crazy one.”

— Shahar Keinan, Brosh Capital [/vision_pullquote]“I decided not to do it for that very reason,” Rechler said. “You’re trying to sell units. With that kind of transparency, you can’t control the messaging.”

“It’s not ideal,” Barnett agreed. “But it comes with the territory. I took the money. Now, I have to pay for it.”

The disclosures provide rare insight into how Extell is trying to put together the funds to finish CPT, which many in the market have speculated will not get built. The 1,500-foot-high condo project at 217 West 57th Street is set to Eclipse 432 Park Avenue as the tallest residential building in New York and will have a sellout of over $4 billion. But Barnett needs over $2 billion just to build it, and said the total capitalization of the project tops $3 billion.

Here’s the math: Barnett’s equity, plus an approximately $300 million capital injection from SMI and an infusion of cash from Nordstrom (which is buying its space), amounts to more than $800 million lined up for the project so far, Barnett confirmed. That leaves the developer with approximately $1.2 billion to go, $300 million or more of which may come from money raised through the EB-5 investment visa program. Barnett has tapped the program for cash several times in the past, including for 1MS.

Yaniv Saylan, an analyst at Israel Brokerage & Investments, said that as a “bondholder,” he had “uncertainty and a lack of awareness” about how CPT will be built.

“I’m worried about it,” Saylan added.

“All you have to do is go by 57th Street and you’d see it was getting built,” Barnett countered. “There’s never been a slowdown.”

Extell is in talks with several potential lenders for the $900 million construction loan — though Barnett declined to confirm any names, sources said the list includes JPMorgan Chase and the Korea Investment Corporation.

But the developer is in a serious time crunch. It has just three months to repay a $235 million land loan from Blackstone Group, which it secured in 2013. To repay the loan, Barnett is counting on securing the construction loan rather than going through a refinancing. If he’s unable to repay Blackstone by the deadline, the loan goes into a one-year standstill agreement, whereby the private equity giant can’t demand an immediate settlement until the latter part of 2017. Barnett has already blown one deadline. If he blows the next one, the interest rate on the loan will shoot up from 8 percent to 14 percent.

He isn’t bullish on racing the clock. “We have a deadline to meet and we’re going to try very hard to meet that deadline,” he said. “That’s our job. Beyond that, I’m not going to speculate.”

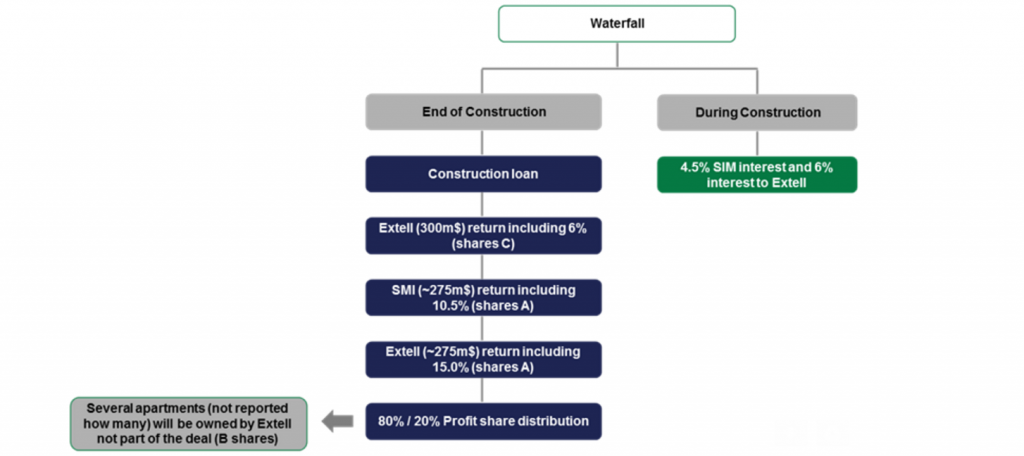

And then there’s SMI. The subsidiary of Shanghai Municipal Investment, a developer of Shanghai’s tallest skyscraper, expects to make a return of up to 20 percent if the project goes as hoped, according to Barnett.

SMI will be entitled to an annual interest of 4.5 percent in monthly payments, as well as 30 percent of the development fees, according to TASE filings, which also show that Extell needs to get SMI’s blessings for all critical decisions.

But if Barnett can’t close on a construction loan by July, SMI has what amounts to a real estate get out of jail free card: It can force Barnett to buy back its equity stake for roughly $300 million, plus interest. And if he can’t come up with the funds to buy SMI out by July 2018, it can push him to sell the whole project. While few expect it to go that far, it’s a scary proposition for any developer.

“It was kind of a distressed deal,” said one Israeli bond market source. “You have a lot of conditions. It’s an equity partner if everything goes smoothly, if not, it becomes sort of a mezz lender.”

A chart showing the SMI deal (Credit: IBI)

In an August report, IBI said CPT “represents the core risk to Extell’s business because of the challenges it will face in seeing this project through the completion. “These include the uncertainty over future funding sources, the relationship between the parties with an interest in the project (Blackstone, Nordstrom and SMI) and the softening of demand for residential property in New York.”

Bankers said SMI’s demands illustrate how equity investors are getting serious about contingency plans, in case the market slides further. And there are signs that lenders are following suit.

“Lenders are becoming more informed about the sponsor’s other projects and those deadlines,” Ori Eisenberg of real estate financial advisory firm One Ha’am said in September, when Extell closed on its construction loan for 1MS. “Terms are being customized.”

Brad Dubeck, the commercial real estate banking executive for Bank of America in New York, said, “these days, the domestic banks are not keen on new ultra-luxury condo loans and many foreign lenders have lost their appetite as well. But this is a terrific piece of real estate. I’m confident Gary will secure financing. It might be more expensive than in the past and will likely come from a non-traditional provider.”

Developers such as Macklowe Properties and CIM Group have turned to alternative lenders such as hedge funds to get their projects built. At 432 Park, for example, the word is that Macklowe and CIM are paying nearly 10 percent on their loan from Children’s Investment Fund. Others have gotten even more creative: Sharif El-Gamal, for example, turned to a consortium of international lenders to score $219 million in Sharia-compliant financing for 45 Park Place.

[vision_pullquote style=”3″ align=”right”] “You have a lot of conditions. It’s an equity partner if everything goes smoothly, if not, it becomes sort of a mezz lender.”

— Israeli bond market source [/vision_pullquote]Barnett believes he’s on solid footing. “It’s an extraordinarily low loan-to-value loan,” he said. “We’re going to be looking at less than $2,000 a foot [basis] for a construction loan and 220 [Vornado Realty Trust’s 220 Central Park South] is averaging [sale prices of] between $8,000 and $9,000 a foot.”

But even he concedes that, for banks, perception matters.

“Today, it’s not so much a question of loan-to-value as that condos are difficult to finance, period,” he said. “Not because they don’t make sense, but because, even if they’re guaranteed their money back, the banks just don’t want trouble. They don’t want to get a call from regulators saying they need to put more reserves forward, even if it’s not warranted. They know they can’t fight with Uncle Sam.”

First we take Manhattan

A rendering of One Manhattan Square

Extell’s recent flurry of financing deals at 1MS convinced investors the project is now a go — even if not quite on the terms they expected.

The firm was well underway with work by the time it scored the construction loan in September, thanks to Barnett’s own deep pockets.

“Those pockets,” he quipped, “were starting to feel a bit empty.”

One Ha’am’s Eisenberg said that after SMI secured a corporate guarantee on CPT, he’d heard that Deutsche Bank would also get one for the $500 million construction loan they are leading on 1MS.

“This is unusual for a New York developer,” Eisenberg added, “but I don’t think it’s by chance.” The construction loan was also downsized from an original $600 million, but the lenders have the option to bump it up to $750 million within the first nine months, according to TASE filings.

“It was a struggle,” Barnett admitted. “We thought we’d be able to get a higher loan per square foot price than we were able to achieve. We had to lower our sights by more than 10 percent and pay a little bit more.”

[vision_pullquote style=”3″ align=”right”] “Even if they’re guaranteed their money back, the banks just don’t want trouble.”

— Gary Barnett [/vision_pullquote]Extell was also counting on $463 million in mezzanine financing from RXR, but after Barnett didn’t score his construction loan in time — a condition of closing on the mezz loan — Rechler’s firm slashed its loan to $300 million and raised the interest from 7 to 8 percent. The loan is also collateralized by Extell’s condo project at 500 East 14th Street in the East Village and its rental tower nearing completion at 555 10th Avenue.

Dubeck said developer-lenders such as RXR, who’ve filled a gap left by traditional banks, are typically able to negotiate better terms as they face little competition.

“On one hand, it’s very positive to see an experienced and sophisticated player like RXR make investments in Gary’s projects at a more uncertain time in the market,” he said. “It shows support for the business plan for those assets. On the other hand, it might signal the lending appetite is cooling.”

Barnett joked that Rechler “conned me,” promising cheap debt.

“He’s a charming fellow, Scott,” Barnett added. “We went down the road and it turns out it wasn’t so low-cost. But, it’s probably a win-win situation. For us, it gave us that extra chunk of capital, which, given the financing environment, we needed.”

With construction and mezzanine loans in place, Barnett now has about $850 million for the project, enough to finance about 18 months of construction, according to the developer. That amount includes an additional $55 million he secured last month from a Deutsche Bank-led consortium. Completing the project will require another $190 million. RXR is likely to exercise its option to increase its loan by $163 million, Rechler said, and Barnett will look to banks and EB-5 funds for the rest.

“With doubts about whether construction would actually be completed having now been lifted, the only concern is how quickly the project will sell and the prices for properties,” the IBI report stated.

The 815-unit project’s target sellout is about $1.88 billion, down from over $2 billion last year. Extell has already sold 60 units for a total of $125 million to both domestic and Asian buyers, according to Israeli bond market filings from Sept. 5 — and the sales office is opening this month.

“Only a few deals were sold directly to China, but we have a lot of Asians buying because it is Chinatown,” Barnett said. “It’s really word of mouth though, because we [the sales office] are not open. The issue is logistics. There’s a lot of people interested but you have to be able to get deals done.”

Spring cleaning

Barnett’s continued need for cash has some of his investors wondering: What other sources of capital might he tap?

Going back to the Israeli bond market doesn’t seem like an option, at least not now.

“The market has learned to distinguish between Gary, who is a developer, and operators focused on income-producing assets,” said Yossi Levi of Infin, which advises U.S. developers on raising debt in Israel. “For condo developers, it will be very hard to raise money right now.”

A possible source of funds, Israeli investors believe, is a sale or refinancing of Extell’s 555 10th Avenue. The 52-story, 478-unit luxury rental project will begin leasing in October and IBI forecasts its annual net operating income at $30 million.

When RXR reduced its mezzanine loan for the three Extell projects, it also restructured the deal so that Extell has greater financial flexibility on 555 10th. Extell may now sell or refinance its stake, which is valued at between $300 million and $400 million, based on a total asset valuation of between $700 million and $800 million, Saylan said.

Extell has already sold off other assets, including a site at 134 West 58th Street to Stanley Wasserman’s S.W. Management for $61.5 million and another at 12 West 48th Street to DNA Development for $37.2 million. It’s also looking to sell a site at 30-32 East 29th Street.

“If the economics make sense to sell, I’ll sell,” Barnett said. “If it makes sense to keep long-term, I’ll keep it. I like owning New York real estate long-term — but not if it’s stupid.”

But Barnett said he won’t necessarily move funds from these prospective sales into CPT. He has plenty of other projects, such as CityPoint in Brooklyn And A Development Site On East 86th Street, into which the money could go.

“We have some small assemblages that we thought we’d be able to make bigger but couldn’t,” he said. “We’re doing a spring cleaning. We have a number of major projects in the pipeline and those just take up time and money that could be put to better use. It’s not huge money. We don’t see this as a source for financing.”

Proposed changes to the EB-5 program, which is up for renewal, could complicate Barnett’s capital expectations. Some proposals would curtail the number of projects eligible to accept EB-5 money and would increase the minimum investment amount for EB-5 applicants from $500,000 to $800,000 for projects in high unemployment areas. In areas with low unemployment, the minimum threshold would jump from $1 million to $1.2 million, potentially putting a dent in investor demand.

A far more damning provision would require existing investors to retroactively cough up the additional amounts. It is this change that could cause investors to pull their money out of U.S. real estate projects, leaving developers in the lurch. “If it goes through in its current form, it ends the EB-5 program,” said immigration attorney Mona Shah.

That would hit Barnett particularly hard, as he’s looking to raise at least $400 million through EB-5 funds for 1MS and CPT, some of which has already come through.

Barnett admitted the uncertainty surrounding EB-5 was a nuisance. But he believes the likelihood of the retroactive provision going through is slim.

“It will definitely be restrictive but I don’t think Congress wants to hurt people for very little benefit,” he said. “Whatever legislation gets done, I think it’s likely that it will be done in a way that doesn’t damage the investors that have already put money in in good faith.”

The price is right

A view from inside One57

Barnett’s last great triumph, One57, could actually become an unlikely stumbling block in his fundraising quest for CPT and 1MS.

The alpha dog of the last boom now has its tail firmly between its legs. Where units at the property were once devoured by wealthy investors looking for a quick upside, some of those buyers have suffered losses in recent months. For example, Escape from New York, an LLC that bought a pad at One57 for $32 million in 2014, recently went into contract to sell the unit for what’s likely to be at least a $7 million loss, given that the unit’s last asking price was $25 million.

In March, Extell reduced the projected sellout at the building to $2.56 billion, $162 million lower than in 2013. Banks keeping tabs may be loath to lend on a project likely to be even more ostentatious. Many of Barnett’s rivals have decided to wait out the slowdown. JDS Development Group and Property Markets Group delayed sales at their skinny supertall at 111 West 57th Street, and Witkoff shelved plans to Convert The Park Lane Hotel into luxury condos.

Though Extell’s investors may not share Barnett’s optimism about the condo market, they take solace in the company’s seemingly stable net asset value portfolio.

[vision_pullquote style=”3″ align=”right”] I like owning New York real estate long-term — but not if it’s stupid.”

— Gary Barnett [/vision_pullquote]“If in the past Extell’s future hinged on the securing of funding (so much so that at times it looked as if the company would have no option but to suspend construction at all sites), this is not the case anymore and it will probably remain as such for at least another year,” IBI wrote in its report.

In a bid to calculate Israeli bondholders’ level of security, Brosh Capital’s Keinan said his company tallied up all the assets in Extell’s public Israeli offering.

“We calculated what he [Barnett] would get if he sells everything tomorrow,” Keinan said. “We did that for each and every one of his assets. After we did that, and deducted the bond loans, we still got a positive equity value. Even if he needs to sell everything tomorrow, he still has positive equity, guaranteeing the bondholders get their money back in full.”

Barnett doesn’t dwell on the doom and gloom headlines. He prefers rosier stuff, like sales at Vornado’s 220 Central Park South, which he called “15 Central Park West on steroids” for its strong performance. (It’s worth noting, however, that after trumpeting sales at the tower every chance he got, Vornado’s CEO Steve Roth has stayed mum about them for about a year.)

He also points to a more recent rebound at One57. While Extell sold no units there in the first two quarters of the year, deals were signed on four apartments for a total of $80 million in the six weeks ending Sept. 5.

“There are still a lot of people who want to buy,” Barnett said of the luxury market. “It’s just a question of them thinking that the market is turning and the psychology is holding them back. But that only lasts for a while.”

He’ll succeed, he believes, because he’s doing what some of his lesser rivals failed to: pricing projects on their merits.

“A lot of it’s in tertiary locations,” he said of other new developments. “People bought and paid high prices for the land and now buyers look at it and think, ‘Hang on, why am I paying $8 million to go there?’ Then, there are people who are asking stupid prices and people who aren’t executing well. You didn’t know what you were doing, guy. You didn’t give the people what they want.”

Correction: In an earlier version of this story, TRD incorrectly stated the purchase price of 12 West 48th Street. It was $37.2 million.