When 220 Central Park South hit the market in 2015, Vornado Realty Trust didn’t throw open the doors so much as it cracked open a window.

Aspiring buyers had to fill out questionnaires about their income and wealth if they wanted access to a nondescript sales office at the company’s headquarters. And CEO Steve Roth earned a reputation for being a one-man co-op board, who personally vetted each prospect and turned down more than a few.

The unorthodox approach paid off. By May of that year, Vornado announced it had sold $1.1 billion worth of condos in just six weeks.

After inviting a “limited audience” to the building’s sales gallery, the developer scored commitments for one-third of the building’s 118 units and raised prices three times in those six weeks. The absorption was “extraordinary and unprecedented,” Roth boasted during a May 5 earnings call.

But in the two years since, Vornado hasn’t disclosed any sales figures at 220 CPS, mimicking other developers who have kept such updates close to the vest to avoid tipping off the competition and to minimize fallout if the project doesn’t meet expectations.

Lenders, however, can’t be kept in the dark. Many require developers to hit sales milestones as a way to mitigate risk. Take Roth’s biggest rival in the city’s latest ultra-luxury condo wars, Extell Development. In January, Gary Barnett’s firm sewed up $1.1 billion in financing for its most ambitious project yet, the $4 billion Central Park Tower. The loan came with a catch — the lenders stipulated that Extell must sell $500 million worth of units in three years.

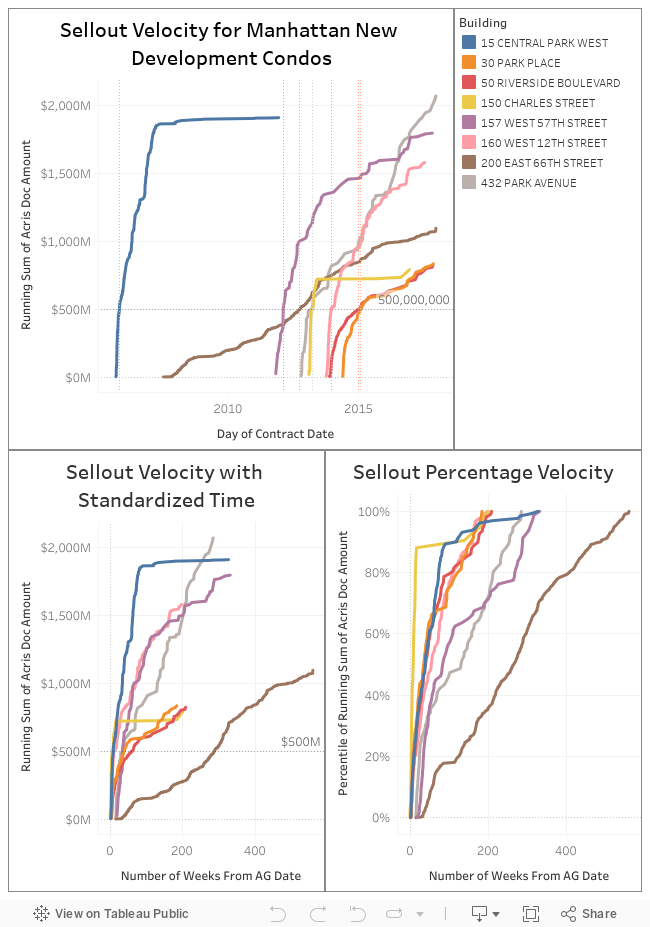

To size up Extell’s chances of reaching that target, and to understand what other luxury developers coming to market should expect, The Real Deal analyzed sales velocity at eight of the priciest condos to launch since 2005. By scrutinizing hundreds of deeds and noting when units went into contract, we tried to answer the question: How long did it take each of those projects to hit the $500 million mark?

Timing is everything

Though marketing times varied wildly, the analysis, using data pulled in January, found it took an average of 60 weeks — or roughly 14 months — to sell $500 million worth of apartments from the day the New York Attorney General’s Office approved the developer’s offering plan. Keep in mind that we only looked at buildings that have had closings; developers aren’t required to report in-contract sales activity.

15 Central Park West

One of the fastest out the gate was 15 Central Park West, Zeckendorf Development’s “limestone Jesus,” which hit the $500 million mark after eight weeks. The developers did so by selling 65 condos, with an average price of $7.8 million, the analysis shows. The building soon established itself as one of the most successful condo developments in history, with early buyers flipping their units for double what they paid.

“It had the ingredients of Robert A.M. Stern and a Central Park West address,” said Susan de Franca, CEO of Douglas Elliman Development Marketing. “There was really not that much in the pipeline.”

On the other end of the spectrum was O’Connor Capital Partners’ troubled Manhattan House conversion, which took 288 weeks — that’s 66 long months — to clear that same mark. Among the buildings with sellouts of $1 billion or more, it was the only one that didn’t hit the $500 million mark within three years — the same target Extell is shooting for.

The Witkoff Group’s 150 Charles was the fastest condo project with closed sales to hit $500 million in sales, at less than 7 weeks. The slowest was O’Connor Capital Partners’ Manhattan House, which took 66 months to meet the figure. TRD‘s analysis is based on contract signings; our starting point is the date the AG declared the offering plans effective. (Illustration by Wally Konefal/The Real Deal)

Like 15 CPW, Extell capitalized on a relatively barren condo market when it launched One57 in 2011, at a time when many developers were still underwater or staying on the sidelines following the financial crisis. One57 hit $500 million in sales after 33 weeks, according to the analysis. All it took was selling 20 units — half below $10 million and the rest over $17 million. One of them was Michael Dell’s penthouse, which still holds the city’s closed sales record at $100.5 million.

“Gary hit it,” said Andrew Gerringer, managing director of new development for the Marketing Directors. “The timing was just right.”

Macklowe Properties and CIM Group’s 432 Park Avenue was a step behind One57 when it launched in 2012, but it only took the developers a little longer to sell $500 million in condos — 38 weeks, or nearly nine months, the analysis shows.

“Macklowe made it by the skin of his teeth,” said Gerringer, who noted that the luxury sales started to slow in 2015. But in 2012 and early 2013, Macklowe and CIM had to sell just 36 condos to hit $500 million; 21 of them were above $10 million.

For the luxury condo projects where closings haven’t happened yet, it’s impossible to know how they’re actually faring since developers aren’t required to disclose contracts. Some are known to inflate their success with murky and sometimes misleading numbers. Others may not offer any at all.

Vornado, for example, hasn’t offered a sales update on 220 CPS since February 2016. Hedge funder Ken Griffin is said to be in contract for a $200 million penthouse there, and there had also been talk of a Qatari buyer eyeing a $250 million spread. And even though a pair of buyers are said to have bought units asking north of $70 million, the Zeckendorfs have also said little about sales at 520 Park Avenue, its 34-unit tower. Asking prices there start at $18 million and go up to $130 million for a triplex penthouse.

Other current billion-dollar-plus projects where closings are yet to occur include 111 Murray Street ($1.05 billion; a source recently said that 80 percent of units had been sold), 53 West 53rd Street ($2.12 billion), One Manhattan Square ($1.88 billion) and the Belnord conversion ($1.35 billion).

Meeting deadline

When Extell invited select agents to Central Park Tower’s sales gallery in November, the 179-unit condo wasn’t officially for sale, even though the AG had approved the offering plan in May. The clock started ticking once the developer locked down the construction loan in January.

Central Park Tower

Per the terms of the loan, Barnett must sell $500 million worth of apartments and pay down $300 million of the loan principal by 2021, according to documents filed on the Tel Aviv Stock Exchange.

If history is any indicator, 36 months is a viable target even in a lukewarm condo market where sales have been slowing since late 2015. During the fourth quarter of 2017, the absorption rate for new units was 8.2 months, up 24.2 percent year-over-year, according to appraisal firm Miller Samuel. The number of sales dropped 19 percent during the same time to 387.

In an uncertain market with lots of unsold product, Barnett plans to set new records: Twenty of the units are priced at $60 million or more, and the overall projected sellout is an unprecedented $4 billion.

The rest of the units, however, are two- and three-bedrooms priced between $6.5 million and $26 million. The blended price per square foot comes to just over $7,100, slightly cheaper than neighbors like 220 CPS, where the blended asking price is $7,357. With an entry point starting at just $1.5 million, Barnett has a rare product, and has to sell just one-eighth of it to satisfy his lenders’ demands.

“To do a two-bedroom facing the park under $10 million doesn’t exist, and they’ve done it,” Compass’ Victoria Shtainer said in January. The building is priced to sell today, she added — not three years out.

“Some developers price a $10 million apartment at $15 million,” she said, “because that’s where they think the market will be.”

Barnett said he is “99.9 percent sure” he’ll hit $500 million long before January 2021. He cited what he described as CPT’s unmatched views and location, as well as the success of nearby buildings, including 432 Park and 220 CPS.

“All those sold $500 million in the first six months,” he told a reporter. “Do you have any doubt?”

Pricing: An imperfect science

Sales benchmarks are common at major projects to mitigate risk for lenders, who have grown more cautious about issuing condo loans since the last cycle. Low-leverage loans typically require developers to sell a certain number of units within 12 to 18 months of the project’s completion. But high-leverage deals have tighter covenants to keep units moving.

All those sold $500 million in the first six months. Do you have any doubt? — Gary Barnett, speaking to a reporter

“Lenders might be fine selling at a 20 percent discount to the Schedule A to get themselves out,” said Square Mile Capital’s Michael Lavipour, who added that sponsors are generally inclined to hold out for higher prices to maximize their profits. “You don’t want a failed marketing process where the inventory sits online without selling, and then you have a busted project.”

Factors influencing the sales benchmarks include the amount of leverage, size of the project and location.

150 Charles Street

“There are typically graduated levels throughout the term of the loan,” said Matt Petrula of M&T Bank, an active condo lender in the city. “It’s commonplace and necessary to ensure your project is tracking to the anticipated business plan that you underwrote.”

Time Equities’ Francis Greenburger said sales at his condo at 50 West Street “blew the benchmarks away” largely because the development hit a sweet spot in the market when it launched in 2014. (When TRD pulled the data in January, 50 West had sold $447 million worth of apartments.)

“Every developer is different, but I’m risk averse, so I only agree to benchmarks that I feel we could safely meet,” Greenburger said. “In another situation, that would be very stressful.”

Strategically releasing units for sale — a practice known as “inventory control” — is how most developers and marketers keep momentum going.

“The whole idea is you don’t want to let people come in and cherry pick apartments,” said Gerringer. “If you let people cherry pick and then you raise prices, you’re left with the most expensive units and the hardest stuff to sell.”

Typically, developers start with a sampling of units based on size, line, layout and price.

One high-end developer said it’s important to stagger a few different price points.

“You want to introduce representative units to the market one at a time, otherwise you are negotiating against yourself,” he said. “Some buyers of expensive units want to be the first, so if there are upward price amendments they bought, more or less, a bargain.”

Some developers push the cheaper units first to generate momentum.

We’re all making rough judgements of what the value of a higher apartment is versus a lower apartment. The ultimate decider is the marketplace. — Francis Greenburger

“You generally put your lowest units on first, so when people search for apartments for up to $5 million, they see your $4.5 million unit even if most of your inventory is asking $7 million,” another luxury condo developer said.

No sponsor really knows in advance how the market will react to prices, according to Greenburger. “We’re all making rough judgements of what the value of a higher apartment is versus a lower apartment,” he said. “The ultimate decider is the marketplace.”

A data-driven approach can eliminate some of the guesstimating. Gerringer’s team assigns grades to units they’re marketing so they know how each stacks up. It allows the sales team to see which price points are selling, so they can adjust prices and have units play off each other.

Manhattan House

“If something is not selling well, you don’t raise the price,” Gerringer said. “You raise something else to make the other look better.”

Over the last 18 months, buyers have been drawn to buildings that are move-in ready, or projects where they can at least see a finished model unit, Elliman’s De Franca said. That looks to have helped Macklowe and CIM at 432 Park Avenue, where a series of large closings have taken the project over $2 billion in sales.

“It creates a sense of urgency knowing that there are fewer units left,” she said. “It also mitigates risk.”

And that could prove challenging to developers who have just launched or are about to launch sales. They’re not just competing with other recent entrants, but in some cases with their other projects. Barnett, for example, even as he tries to convince the market to fall in love with CPT, still has unsold units at One57, where some resales have traded at a loss.

These days, developers aren’t necessarily launching sales immediately after the offering plan is declared effective. Instead, they might time the launch based on what else is on or coming to the market. Most have a soft marketing period for friends and family. Vickey Barron of the Corcoran Group cited two reasons: They want to take care of their people, and they want to give momentum to the sales effort.

If you let people cherry pick and then you raise prices, you’re left with the most expensive units and the hardest stuff to sell. — Andrew Gerringer

“It’s not that it’s a game being played,” Barron said. “You’re just dealing with a lot of money when it’s a whole building. The key in this market is velocity and momentum. No one wants to get stagnant. They don’t want to stall.”

Profits in the aerie

Most developers save the penthouses for last to maximize the price, since their own profits are largely tied to those units. Some resist listing the penthouse publicly at all, since in ultra-luxury projects the penthouse is usually sold by word of mouth anyway. But De Franca said developers can use the penthouse to generate buzz for the overall project.

“By achieving a record-breaking sale or a strong sales number, people see, ‘Wow, there’s really value if someone is paying $30 million or $40 million,’” she said. “That’s enabled developers to raise [prices on] lower-priced units.”

Some developers prefer to see how the market reacts to the rest of the building first, according to Justin D’Adamo of Compass. He pointed out that CPT’s two-bedroom units — averaging $8.5 million, or around $5,000 per foot — are “much more movable” than the $95 million penthouse.

He felt confident Barnett would cross the $500 million mark well within time.

“If only a couple of units are sold in that $60 million to $70 million range … you’re a third of the way there,” D’Adamo said. He speculated that’s why Extell hasn’t yet marketed the project widely. “They’re probably going and finding those big fish out of this market.”